Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

John Zechner

January 28, 2021

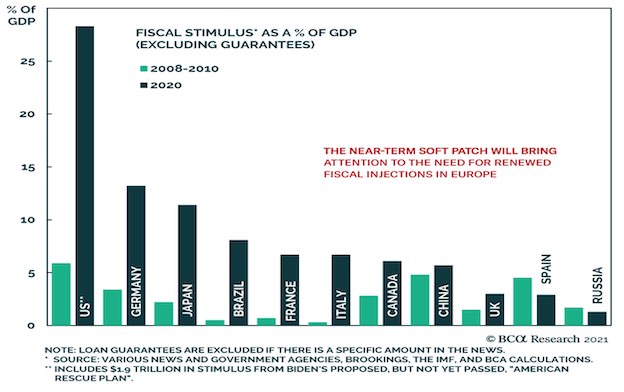

While most of the chatter has been about the massive liquidity created by central banks, the conversation has begun to shift to fiscal policy, which has already eclipsed its contribution in past crises and is now assumes the primary role in providing a reflationary bridge until the pandemic subsides. However, as shown below, the outlook for global stimulus is varied between regions. The U.S. has been the leader by far in fiscal stimulus in the current pandemic and is only going to increase further with democrats having control of basically all three branches of the government. Meanwhile, European states’ stimulus has lagged even as they impose more stringent lockdowns and is being reflected in recent economic data releases. Chinese fiscal response has been much more muted relative to what they applied in the aftermath of the Financial Crisis in 2008. Maybe this is due to worries about excessive debt or a better response and results in dealing with Covid19, such that less stimulus has been needed. Thus, although the effect of China’s massive 2020 policy response will continue to support the global recovery, it will not be the main driver like it was a decade ago.

Ultimately, the combination of supportive fiscal policy amid ultra-easy monetary policy has created an optimal environment for risk assets such as stocks. This is especially true over a two-year time frame, during which the risk of overheating is low. The bigger question now is how to adjustment your equity strategy going forward. We don’t believe that the playbook that has worked over the past year will be the right one for the recovery phase. Valuations in the ‘stay at home’ stocks and high growth sectors of the market have reached excessive levels and, while earnings have not been the story at all for this group, we still believe that the growth comparisons are going to become more difficult going forward. The use of Zoom, the backlog of Peloton bikes, the explosion of cloud-based services and the growth of home delivery apps are just not going to rise at the same rate as they did in the early stages of the pandemic. Meanwhile, the rollout of vaccines and the eventual full re-opening of the economy will lead to a recovery that will start to shift more spending into sectors that have lagged for the past year, such as travel, dining out, retail shopping, concerts and sporting events with spectators! We also expect that banks will start to divert more resources into lending activities for real business expansion and consumer spending versus putting the bulk of their deposits into government and corporate bonds.

Despite the continued easy money policies from central banks, we believe that there will be some upward pressure on longer term interest rates and the cyclical/resource sectors of the stock market should start to play some ‘catch up’ to the growth sectors of the market, which had seen elevated due simply to the low level of interest rates. While excessive bullishness and some concerning technical market trends has induced us to reduce our exposure to stocks slightly in the short term, we remain close to fully invested in stocks. Our sector weights have shifted significantly, though, taking money out of growth sectors such as health care, technology, consumer staples and utilities and shifting more funds into financials, energy, industrial products and consumer discretionary groups such as travel, autos and restaurants. The telecom sector remains one of our highest conviction bets over the long term. In a market where investors are looking for ‘long duration assets’, the fact that the companies in this sector have built out massive networks to host the growing need for data, the increase in streaming activity and shift to 5G makes them a great ‘infrastructure play.’ While these stocks have lagged many other growth stocks in the past year due to reduced Roaming activity tied to travel and the elimination of ‘overage fees’, stocks such as BCE, Telus, Shaw and Rogers all pay attractive dividends, generate substantial free cash flows and should see a pickup in operating cash flows again in 2021.

In terms of some stock specific actions we’ve taken lately, we continued to add to General Motors last month despite sharp recent gains. Our simple thesis is that, if Tesla can command a market cap of over US$800 billion, then GM should be worth more than $70 billion, especially considering that it produces over six times as many autos annually, generates strong free cash flow and is going to take its brand names into electric vehicles with spending plans of over $25 billion over the next decade. Also, believing in the re-opening of the economy, we re-initiated a position in Air Canada near the $20 level. The company is still generating losses on a daily basis due to travel restrictions and the stock is down over 60% in the past year, but they have reduced costs and fortified their balance sheet and capital structure such that they are able to survive this downturn and position for growth in the recovery. The pending acquisition of Air Transat could turn out to be very timely as we believe that, although business travel may never return to its pre-pandemic levels, personal and vacation travel will return in a very robust way as people will want to visit relatives and take holidays after a very long hiatus. The strong, well-financed players such as Air Canada will emerge in a stronger industry position to capitalize on this growth.

Bottom line for investors, there is clearly a lot of short-term risk due to excessive speculation, extended valuations and pandemic-related economic risks. But we also believe we are at the beginning of a new economic cycle and that the lockdown measures and rollout of vaccines will bring the pandemic under control. With continued support from both fiscal and monetary policies, there should be some good economic tailwinds later this year and onward. Record debt levels will have to be dealt with at some point as well, but the over-arching news stories this year we expect will turn to better economic numbers and a strong profit recovery. Within our managed portfolios, cash has increased but this has been due more to a move out of bonds, where we see negative real returns over the next few years and are using only as a ballast to most portfolios for stability and a source of cash for any potential stock market volatility. Investors may want to ask whether the potential reward for staying in the market is enough to offset the possible damage from a downturn. We believe the trajectory for stocks over the next few years will be higher, in line with a rebounding global economy, and we hesitate trying time the corrections and risk missing gains due to shorter-term risk concerns. A better strategy, in our view, is to position in names where valuations are reasonable, growth is tied to an economic recovery and dividend yields can supply some income during more volatile periods.

1 2

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.