Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

John Zechner

January 28, 2021

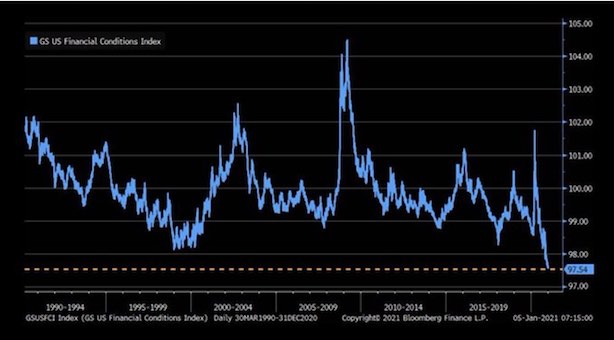

While investing in stocks or any other asset class in never easy, even at the best of times, we see the environment of the past year as being even more complicated and potentially volatile than any we have seen in at least the past decade. The worst global health pandemic in over 100 years, the fastest 35% decline in stocks on record (mid-February to mid-March 2020) and the sharpest economic downturn since the Great Depression hardly seem like the kind of stuff to send stocks soaring to record highs, but the reality is that is what has happened. Now investors have to decide whether the sharp moves higher, the extended valuations and the excessive levels of speculation are setting the stage for another ‘stock market bubble’ or whether stocks are just reflecting the reality that monetary conditions (interest rates) are going to stay extremely supportive of financial markets for a very long time. The ‘easy money’ conditions that were absolutely necessary in the early stages of the pandemic when economies were in a liquidity crisis have been continued by global central banks, which has fueled increased speculation in financial markets since the mass of new liquidity has nowhere else to go. The chart below shows the Goldman Sachs U.S. Financial Conditions Index, which has fallen to levels not seen in 30 years.

On the other hand, the bullish action could simply be reflective of the firm belief that the pandemic will be brought under control by mass vaccinations, such that the global economy will have a quick economic rebound driven by ‘pent-up demand’ which will fuel an equally sharp recovery in corporate profits. While, like most investors, we find ourselves wanting to focus on the longer-term and remain fully invested, it’s very difficult not to be swayed by the extreme volatility and short-term risks and want to become more defensive in order to protect the gains of the past year. We are seeing far too much of the behaviour we saw in financial markets in the late 1990s. The stock bulls point out that technology sector valuations are better supported by real cash generation by the largest players in the industry, with the five FANG stocks generating combined free cash flow of over $200 billion last year. But there are other parts of the market where speculation in running rampant. We can easily point to Bitcoin, the non-profitable growth stocks such as Tesla, ‘work from home’ beneficiaries such as Zoom and Peleton and inflated first day trading gains for new issues such as Doordash and AirBNB as areas where speculative activity seems to be excessive. But nothing points to speculative fever, in our view, like the explosion in issuance and pricing of SPACs (Special Purpose Acquisition Companies). These are investment vehicles that take in new funds with the promise of investing those funds in mostly private companies in the highest growth sectors such as biotechnology, cloud computing, space technology, electric vehicles or cannabis. If no suitable investments are found within a designated period of time, then the money is returned to investors. They are effectively a “blank cheque” shell corporation designed to take companies public without going through the traditional IPO process and allow retail investors to invest in private equity type transactions, particularly leveraged buyouts. The shocking part of this is that these SPACs have taken off from day one of trading, despite none of the funds having even been spent! This is all so reminiscent of the funding of ‘fibre’ in the late 1990s, when companies would plan to spend ‘X’ dollars of funds raised on laying internet fibre networks, and the stocks would immediately trade at ‘4 times X’ or higher. That lead to an explosion in valuations for the sellers of fibre such as JDS Uniphase, Nortel and Lucent or the major buyers such as communication companies Worldcom, NorthPoint Communications and Global Crossing. Suffice it to say none of those companies are around in that form today because most of them went bankrupt!

Social media takes on Wall Street and the hedge funds. One corner of the market that reeks of excessive speculation is the volatility in the most heavily shorted names, where large institutional investors and hedge funds have lined up substantial negative bets against those companies due to what they see as inflated valuations or unsustainable growth. Now an army of smaller-pocketed, optimistic investors is throwing dollars and buy orders at companies like BlackBerry, AMC Entertainment and GameStop, the last of which had a short interest of over 130% of its total stock float. These stocks have seen their shares skyrocket over the past week as retail investors, spurred by social media and message boards like Reddit plow heavily into those firms. The crush of investors has led to a ‘short squeeze’ as institutional investors and hedge funds scramble to cover their mounting losses. Shares of GameStop were soaring again as we write this, up more than 100% on the day, even as some high-profile short sellers indicated they had retreated from their positions. The video game retailer’s stock is being hyped by investors in online forums on sites like Reddit, causing it to jump from roughly $6 just four months ago to as high as $330, a gain of some 5,400%! That lead to large losses at hedge funds that bet against it, prompting an emergency $2.75 billion deal to rescue one such firm, Melvyn Capital Management. On the January 27th Federal Reserve press conference following its two-day meeting, chair Powell was asked specifically if the ultra-easy money policies of the central banks are helping to fuel much of this speculative activity. He countered that the Fed’s goal is to maintain maximum employment levels and price stability. Reading between the lines, they seem to understand that speculative activity is some corners might be an unintended consequence but that the ultimate goal of maximum employment is still a long way from being realized, with more than nine million Americans still out of work in the past year!

In terms of overall stock market, we are clearly not alone in pointing out some of the risks associated with the current stock market euphoria. U.S. stocks are now “a fully fledged epic bubble,” according to Jeremy Grantham, the money manager who has earned a reputation for his timely forecasts of impending market plunges. “It is highly probable that we are in a major bubble event in the U.S. market, of the type we typically have every several decades and last had in the late 1990s.” His warning highlights the potential risk that goes along with the extreme monetary policies put into place to deal with the pandemic and the resultant bullishness in financial markets. Stock valuations in the U.S. measured against most fundamentals, from underlying revenues to long-term earnings to the replacement value of assets, are mostly beyond the high points of exuberance they reached during the dot-com bubble of the late 1990s.

According to a recent Bank of America poll, global institutional investors are upbeat about 2021 macro and equity prospects. The study has rarely seen such unanimous agreement between investors. If something unexpected were to happen, markets face the risk that a lot of investors will head for the exit at the same time. In another survey, over 90% of millionaires surveyed by E-Trade Financial believe that the stock market is near a bubble. Yet these affluent investors are not running from the market, or parking money in cash. In fact, amid rising bubble fears these same investors say their risk tolerance has increased significantly in the first quarter of 2021, with the majority expecting stocks to end 2021 with even more gains. If an investor with $1 million or more in the market thinks that a stock bubble is already here, or soon coming, you would assume that their strategy would be to raise some cash. But, according to this survey, the answer is to keep investing in stocks, with more emphasis on undervalued sectors of the market. While all this bullishness might seem to be a paradox given the dismal economic data of the past year, the reality is that central banks have created so much liquidity that there is nowhere else to go outside of financial markets. The chart below shows clearly how much the money supply has exploded during the past year.

1 2

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.