Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

John Zechner

March 27, 2018

While worries about ‘trade wars’ weighed on market sentiment last month, there was very little carryover to the outlook for economic growth, which is still expected to be strong this year with an average estimate of 2.7% in the U.S. Corporate profit growth is also expected to have a sharp rebound to over 15%, due in large part to the U.S. tax cuts. The expectation of that growth is what supported stock gains in 2017 and early 2018, but now we are seeing some doubts about the duration of this recovery. The tax cuts, which were designed to bring substantial cash holdings from overseas accounts back into the U.S. to support job growth, have instead been directed by corporations mostly towards stock buybacks. Buybacks have moved back to record annual levels of over US$100 billion, giving additional support to stock prices but doing nothing for longer-term growth and job creation. Stock buybacks have helped ease the losses in the stock market as they have offset the recent large outflows from ETFs. However, we expect the headwinds for the market to increase this year as stock markets will be facing a potential peak in profit (and maybe economic) growth this year as well as rising inflation and continued interest rate increases by the U.S. Federal Reserve. The OECD Diffusion Index (index of leading indicators for the industrialized countries) turned negative recently suggesting we may have seen peak growth for this cycle in Europe, Japan and the U.S. This could all be adding up to a toxic mix for stocks with economic growth peaking and profit growth slowing just as interest rates are increasing and valuations are high.

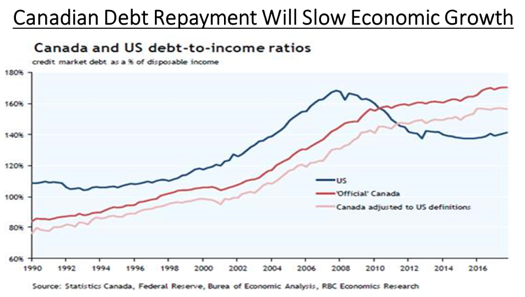

Rising prices are already having an impact on consumer spending as the average consumer is finding they have to allocate more of their income to food, energy, health care, housing and other non-discretionary items as they see those prices rising. This leaves less to pay down excess credit or put into savings. This can be seen in the retail numbers, which have failed to meet recent expectations and done nothing but go down. Last year saw the biggest increase in food and energy outlays since 2011, accounting for 30% of the increase in consumer spending. It has also had an impact on savings which rose from $440 billion to $1.4 trillion after the financial crisis. Those savings have now slipped back to $400 billion. Consumers have basically taken every penny they socked away and spent it. This clearly reduces future purchasing power and is an important lesson for Canadian economic projections since our consumer debt levels and housing market look very much like the U.S. did ten years ago. The logical conclusion is that Canada should experience a much less robust economy over the next few years as consumers retrench in order to pay down record debt levels.

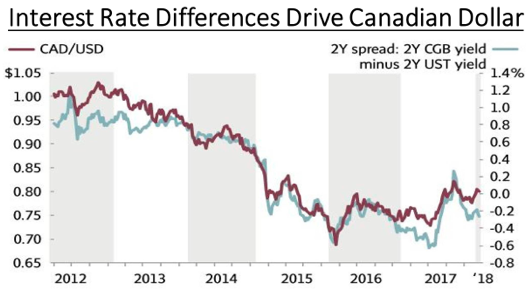

What really moves the Loonie? Canada has always been viewed internationally as a ‘hewer of wood and a drawer of water’ as basic commodities such as oil, gas, copper, lumber and uranium have been the most important drivers of growth while we have depended on trade for most finished goods. So the movement in commodity prices (oil in particular) has always been closely correlated with moves in the Canadian dollar. But, in reality, financial capital is the most liquid and transferable asset. So the tightest relationship between the currencies of Canada and our southern neighbour can be found in the difference in two-year government bond rates between the two countries. As our rates increase we draw capital in and that increases the demand for our currency and, hence, its level versus the U.S. this can be seen clearly in the chart below where the red line is the value of the Canadian dollar versus the U.S., while the light blue line is the difference in the two-year government bond yield in the U.S. versus Canada. Stronger growth in Canada in 2017 pushed our interest rates higher than the U.S. and drew capital up here which increased the value of the Canadian dollar. However, due to high debt levels and worries about the free trade agreement have lowered economic growth and lead to a lower outlook for Canadian interest rates. This has pushed the Canadian dollar back down to the 77c range versus a recent high of over 81c. Given our outlook for more economic headwinds in Canada, we expect further weakness in the Canadian dollar, even though we also see the U.S. dollar weakening against other major currencies such as the Euro.

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.