Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

John Zechner

August 29, 2019

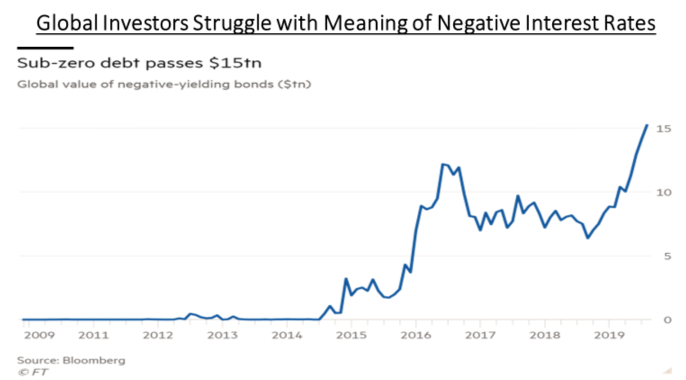

Speaking of ‘no recent precedents’, we are drawn to the implication of negative interest rates on global economic growth and financial markets, especially since we now have over US$16 trillion of global debt trading with negative rates! Sometimes we wonder whether the current cycle of economic growth and low inflation is causing many investors to ‘re-write the playbook’ on investing that has existed for many decades! Clearly the old relationship between inflation and the unemployment rate (the‘Philips Curve’) is relevant anymore as inflation has remained well below normal rates despite an unemployment rate in the U.S. at a 40-year low! But that’s exactly why some strategists, fund managers, and financial advisors are beginning to consider the investment versions of survivalists’ supplies. For the first time in seven or eight years we are starting to some meaningful ‘de-risking’ across portfolios. This has been driving bond yields to record low levels while also shifting many investors to once again look at the gold market as an alternative to paper assets. Whether the tariff war escalates, the downside is a no-growth world where risk sentiment evaporates. Central banks around the world are trying to provide a safety net, but it’s a small net with a lot of holes. Each doomsday scenario calls for its own strategy, but Treasury bonds, gold, and cash are clearly becoming the ‘bunker staples’ in this one.

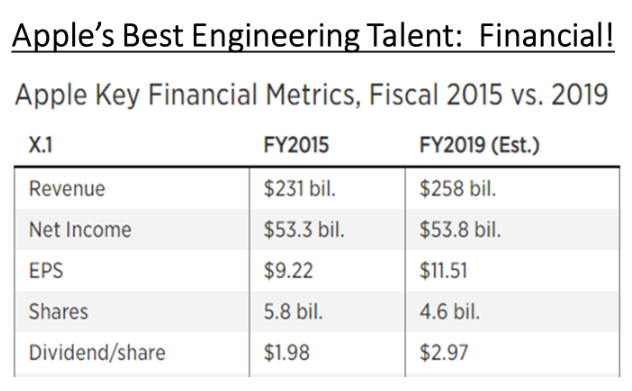

In last month’s letter we included the table below, which used Apple’s results over the last four years to show how share buybacks can distort actual financial results to the upside. While net earnings were basically unchanged over that period, the company borrowed $100 billion in the bond market at cheap rates and used the funds to buy back over $150 billion of their own stock, shrinking the share count from 5.8 billion to 4.6 billion. This lead to an earnings per share gain over the period of over 25% which, in turn, lead to investors putting a higher multiple on those earnings (18 vs 10). Bottom line, the stock ended up doubling in price despite the fact that total net earnings were basically unchanged during that time.

This strategy has been used pervasively by most large U.S. corporations over the last ten years and it always works particularly well in a rising market. But the past month also showed how these buybacks can punish a company when businesses get into more troubled times. General Electric spend over $25 billion in stock buybacks from 2015-2018 at prices in excess of $20 per share. But the stock dropped more than 20% last month, driven in large part by a 175-page report from Hedge Fund manager Harry Markopolos that called GE “a bigger fraud than Enron.” Markopolos, who uncovered Bernie Madoff’s scheme, accused GE of not having sufficient reserves for its long-term care business and not properly accounting for losses at Baker Hughes. While we have no comment on the report, we would wager that GE management wishes they hadn’t wasted that $25 billion on those stock buybacks for shares which are now 60% lower! Stock buybacks may be winning strategies, but only in rising markets!

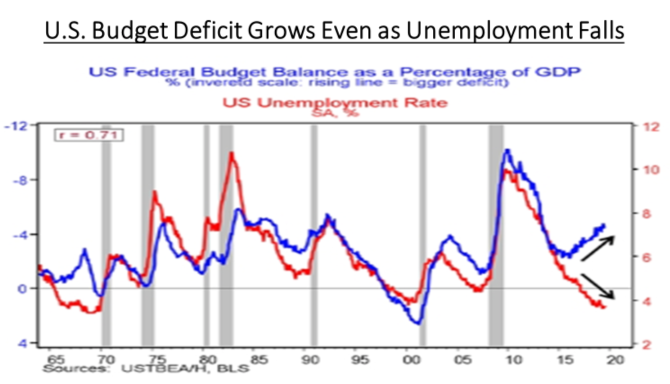

Debt, not geopolitical headlines about Iran or China, is what advisors say clients ask about most frequently. The U.S. budget deficit is on pace to exceed $1 trillion next year, global debt is at a record high and triple the size of the world’s gross domestic product, and $16 trillion of debt yields negative interest rates. The nightmarish scenario many think is most plausible: a “Japanification” of Europe and the U.S., with more economies stuck in a rut of anemic growth and perpetually low interest rates. Loaded with debt, economies can’t grow. Investors reach further for yield, feeding a credit bubble that pops and ripples through financial markets. After years of easy monetary policy, central banks are impotent and unable to stem the crisis. While central banks have done as much as they can to sustain this economic cycle, many pundits now look for fiscal policy to take the reins, much like the spending binge that China went on after the Financial Crisis. But the ‘deficit hawks’ in Germany have already turned down that idea despite the fact that German debt remains low compared to other major economies. The U.S. is also hampered by large debt and further projected deficits despite strong economic growth over the past decade. Recent CBO projections show a US$12.2 trillion cumulative budget deficit that would take U.S. debt from 79% to 95% of GDP! Usually such spending has been positive for growth and the graph below shows how budget deficits have traditionally moved with changes in employment. Deficits rise when unemployment rises and then fallen (or moved to surplus) when economic growth is strong and unemployment falls. But the two measures have deviated under the current U.S. administration, which has seen deficits grow even as unemployment shrinks to record low levels.

Back in tech world, Cisco stock plunged 9%, a day after it reported July-quarter financial results. The company, a leading maker of routers, switches, and security products, is seen as a bellwether for technology spending given its broad exposure to corporate, government, and telecommunication end-markets. While the networking-equipment maker beat earnings estimates, investors were disappointed with its weaker-than-expected sales outlook. The company expects sales in the current quarter to be flat to up 2% year-over-year. That’s a significant decrease from 7% aggregate growth over the past fiscal year. Order growth also meaningfully decelerated to flat year-over-year down from 4% in the prior quarter. In late 2000 I heard Cisco CEO John Chambers on a conference call saying that had just seen the biggest meltdown in new orders ever. That was about 2 months before the peak in the tech bubble. Clearly their client base was very representative of tech spending in general and was signaling the oncoming slowdown. Cisco’s outlook warning on their earnings call just might be the ‘canary in the coal mine’ for the bull market in technology this time around again!

More evidence of the slowdown in technology came when IC Insights released its list of the world’s top-15 semiconductor suppliers in the first half of 2019, and it identified Sony as the only company registering year-over-year growth during the six-month period. The top-15 semiconductor companies saw their combined sales drop by 18% from a year earlier in the first half of 2019. Just more evidence that bullish forecasts for double-digit earnings growth in this group will have to be revised down.

1 2

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.