Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

John Zechner

August 29, 2019

There was no shortage of news and market volatility again in August as the U.S./China trade war, the G7 meeting in France, the central bank summit at Jackson Hole and the continued berating of Federal Reserve Chief Jerome Powell by President Donald Trump all had investors scrambling for some signs of economic direction around which to position their portfolios. On top of that, the barrage of ‘tweets’ on a variety of topics from the U.S. President also upended views on a daily basis as the tone shifted between saying that ‘trade talks were going well’ to positing whether China Chairman Xi or Jerome Powell was ‘the bigger enemy of the U.S.’ To say that these are unprecedented times seems a massive understatement. On top of all the headline news, investors also had to deal with economic data that continues to deteriorate, with Germany and Britain both on the verge of outright recession, China growing at its slowest rate in over three decades and the ‘infallible’ U.S. jobs machine starting to see some cracks. Those with more ‘bearish’ market views appeared to win out for now in August as stocks suffered their worst month since the May, despite a late-month rally on some major portfolio ‘rebalancing’ and more optimism that ‘cooler heads would prevail’ in the trade disputes. Meanwhile, gold prices surged to multi-year highs despite a strong U.S. dollar and bond prices also surged to new highs, with the ‘yield curve’ giving the strongest recession call since 2007 as 10-year yields dropped below 2-year yields.

But despite all the warning signs that we may see out there, investors aren’t really very worried! One yardstick of stock swings, the CBOE Volatility Index, or VIX, had fallen almost 50% this year to under 12, on pace for its biggest annual decline ever, according to Dow Jones Market Data. The gauge measures expectations for volatility over the next month and tends to rise when investors are wagering on big moves in the S&P500 through options. Extremely low volatility has consistently been a better indicator of market tops, while lows in stock prices are usually not seen until the VIX spikes up to levels above 30 and often above 50! While the VIX has moved back to the 20 level in August, it is not yet anywhere near a level that would indicate a market bottom. But a relatively healthy U.S. economy, along with global central banks’ willingness to cut interest rates, have allowed some measure of optimism, despite alarming headlines. In fact, investors’ equity holdings as a share of their financial assets hovered around 30% earlier this year; the last time it was higher was in the late 1990s.

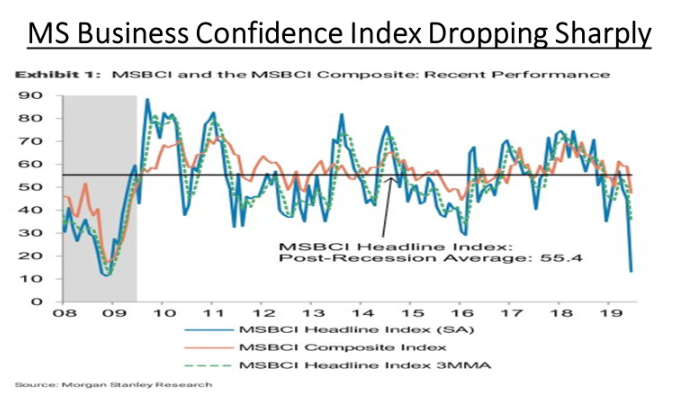

The most resilient aspect of the U.S economy has been consumer confidence, which has soared to record levels this year. However, we started to see a few cracks in these stellar numbers in August. The Conference Board’s Expectations Index declined to 107.0 from 112.4 as the outlook for business conditions and incomes eased. That report follows other confidence gauges that suggest consumer sentiment may be wavering. The University of Michigan’s gauge dropped to the lowest level since January this month, and Bloomberg’s weekly comfort measure recently saw its largest back-to-back slide since 2011. While other parts of the economy may show some weakening, consumers have remained confident and willing to spend. However, if the recent escalation in trade and tariff tensions persists, it could potentially dampen consumers’ optimism regarding the short-term economic outlook.

We continually hear claims that the consumer economy is still in good shape and that, along with lower interest rates, will support higher stock prices. But the consumer tends to be a ‘lagging indicator’ of economic growth. More importantly, we now have more than 60% of the world’s manufacturing in contraction mode. Since manufacturing generally tends to be a leading indicator of future growth, we see this slowdown as another indicator of increased recession risk. Weaker commodity prices, especially copper, lumber, oil and coal, are also signs of weakening demand. This indicator is also being confirmed by the collapse in the Baltic Dry Shipping Index.

Earnings growth has been mediocre, at best, so far in 2019. But analysts tend to resist using these weaker results to lower full year forecasts, deciding instead to push the expected growth into the fourth quarter until actual results finally force them to drop estimates. This process is already taking place, according to the Financial Times, and will eventually threaten stock values. “Analysts have pared profit expectations for U.S. companies by the most in three years as the trade war with China and a dimming economic outlook weigh on earnings and expansion plans. Profit for the S&P500 index companies are expected to increase 2.4% this year, down from 7.7% growth expected at the start of the year, according to FactSet Data. This drop marks the largest decline on a year-to-date basis since 2016.” The corporate sector is clearly displaying worrisome symptoms. With global growth slowing sharply, and domestic activity cooling, further profit weakness represents a risk for business investment and hiring, both of which are key supports to consumer spending.

Adding to market risks, President Trump has relentlessly assaulted the U.S. Federal Reserve in public for raising interest rates last year and not cutting them fast enough for his liking. To be fair, disputes between the U.S. President and the head of the Federal Reserve are nothing new. Richard Nixon, who blamed his loss in 1960 in part on a sluggish economy resulting from tight Fed policy, installed the malleable Arthur Burns as his Fed Chairman after his 1968 presidential victory. Burns dutifully pursued stimulative policies to help ensure Nixon’s reelection, which provided the inflationary tinder for the explosion in oil prices, and the subsequent steep recession of 1973-74. This time around, Fed Chairman Jerome Powell and his colleagues have been careful not to criticize the president’s trade policy choices, and they insist that their decisions are blind to politics. But they have made clear that the uncertainty being created by the escalating dispute with China, plus Trump’s on-again-off-again threat of tariffs against Mexico, and allies in Europe and Japan, were dampening U.S. business investment and had cooled global growth. Powell, in a speech at Jackson Hole, Wyoming, signaled the Fed was open to cutting interest rates again next month to help offset the headwinds from a cooling world economy, while cautioning that that there are “no recent precedents to guide any policy response to the current situation.”

1 2

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.