Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

John Zechner

August 3, 2023

Stocks have rallied this summer as more and more investors are becoming convinced that the U.S. Fed can successfully achieve the mystical ‘soft economic landing’ that has occurred so infrequently. The nearly 10% ramp in the S&P500 since June 1 is the result of more investors embracing this view, thanks to improving inflation. An economy that has shown resilience despite the significant increases in interest rates in the past eighteen months and second quarter earnings which, despite being down year-over-year, surpassed these lowered expectations have all empowered the bullish narrative that the economy will glide down to a slower growth rate for a few quarters without actually going into a recession and then start to grow again in 2024. Add to this the idea that central banks are basically finished or almost done raising interest rates and that falling inflation will allow them to start lowering interest rates again next year and we can see why investors have been flocking back to the stock market despite extremely ‘rich’ valuations. Much of this buying seems to be driven by a ‘FOMO’ (fear of missing out) mentality as stocks have rallied over 25% from the October 2022 lows.

We are not buying into this bullish narrative and have been lightening up on stock holdings on the strength. While we have been surprised by the resilience of the economy, we attribute more of this to all the accumulated stimulus from both the pandemic and massive infrastructure spending. We have had the easiest money policy on record for most of the past decade at the same time as we seen massive fiscal stimulus from each of the past two administrations in the U.S. This money as well as the return of consumer spending on services that were shut down during the pandemic have all contributed to an extended business cycle despite the sharp increase in interest rates. But this highly aggressive increase in interest rates is still expected to dampen economic activity and borrowing costs for businesses and consumers. Additionally, the expiration of pandemic spending programs, along with the rundown of the excess savings that consumers had accumulated during the height of the pandemic, will likely result in reduced consumer spending and a drag on overall economic growth. Just because this hasn’t happened yet, does not mean it won’t happen at all! Monetary policy traditionally works with ‘long and variable lags.’ For the afore-mentioned reasons these lags have been somewhat longer in this cycle.

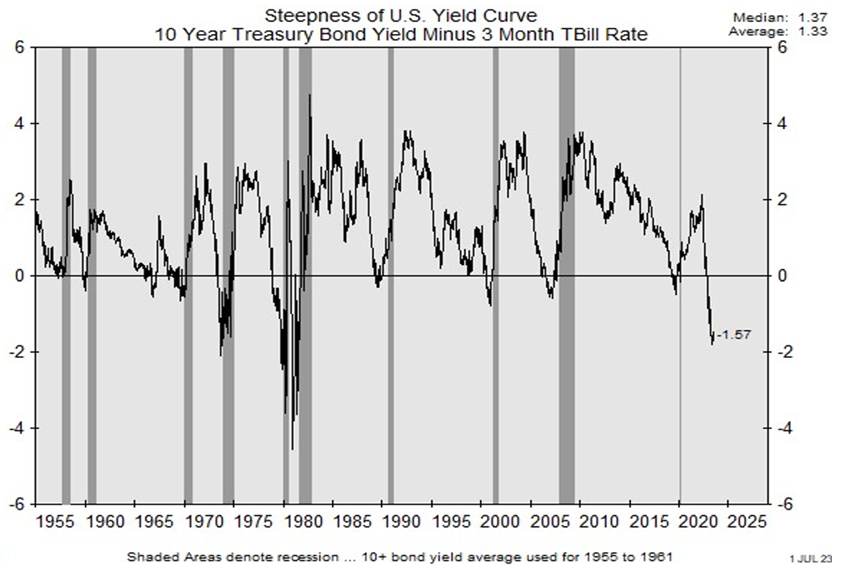

A lot of the commentary we read lately is reminiscent of what we read in 2007 when rising interest rates were not having an impact on economic growth. In the end it was just a matter of time before growth rolled over. The economy has become so levered and investors addicted to low or zero interest rates in the past decade that we don’t see any way that this aggressive move in rates since the beginning of 2022 won’t have a serious impact. The period of very low rates allowed many companies and consumers to lock in debt for longer periods, so those debts have been slower to roll over and face higher rate renewals. Also helping sustain economic growth has been continued strength in employment. While there are some longer-term demographic and other factors that are keeping employment strong, there has also been a reticence for companies to lay off workers at the first sign of a slowdown since they had such a hard time filling those positions during and after the pandemic. In the short term they prefer to reduce hours but, in the end, they will have to move to layoffs as economic growth slows. We saw some of that in the tech sector last year and more recently have seen similar announcements from banks and retailers. In terms of the outlook, we just go back to the simple economic principles that have worked for a very long time. At the top of the list is the yield curve. In the past, whenever the curve gone negative or ‘inverted’ (short-term interest rates higher than longer-term rates) a recession was the ultimate result. The chart below shows yield curve data over the past 70 years, with the gray areas indicating periods of recession. While the time from inversion (line dropping below zero below) to actual recession varied, we see only one period (1967) when the economy did not end up in recession afterwards. No reason to think the current period will be any different and we won’t be in recession sometime in the next few quarters. It is far too early to say that we are ready to begin a new bull market in stocks!

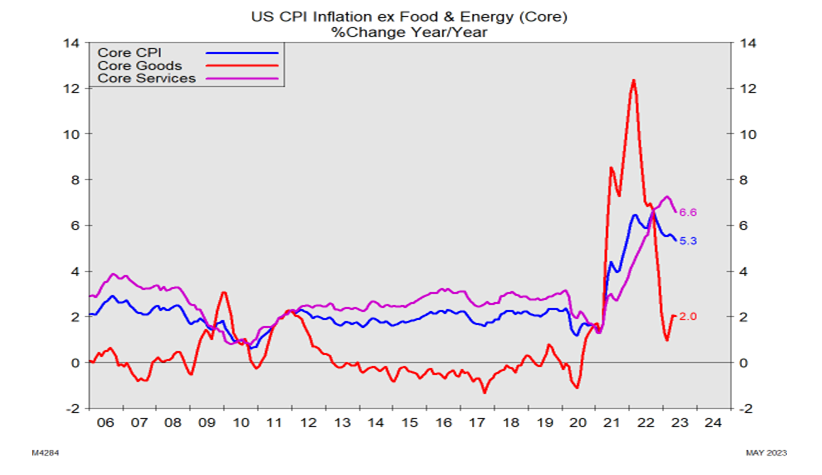

Another risk we see in the stock market is the fact that so many investors believe that inflation has been brought back under control and is moving towards the 2% target range set by central banks such as the U.S. Federal Reserve and the Bank of Canada. But, as shown in the below, it is really only ‘goods inflation’ (red line) that has come down significantly in the past year, and this was mostly due to just a normal retracement of oil and other commodity prices which had surged at the outset of the Ukraine war. The ‘core’ inflation measure (blue line) has come down less and is nowhere near the 2% target range. This is mostly due to continued inflationary pressures from the service sector (purple line) as consumers get back to travel, eating out and other services that had been shut down during the pandemic.

If the central bankers who do not remember the period go back to the history books they will see that the biggest mistake made back in the 1970s was easing interest rates before inflation was totally tamed. That necessitated such draconian measures to bring inflation back under control which included a surge in interest rates to double-digit levels that ultimately resulted in two ‘back-to-back’ sharp recessions in the early 1980s. We expect that central bankers will not want to risk a re-occurrence of those times and will therefore keep interest rates higher for longer than the bullish investment community seems to expect. The only way that we will see reductions in interest rates in early 2024 and a fall in inflation to the 2% target is if the economy is in a full-blown recession. How investors could expect that to be a good environment for stocks escapes us. While we don’t necessarily see stocks retracing back to their October 2022 lows, we think it is far too early to confidently say we are into a new bull market!

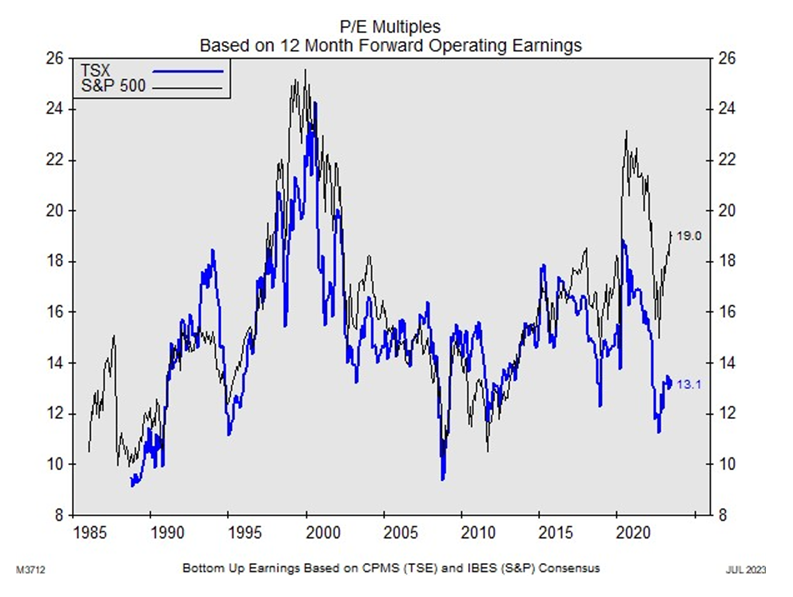

The good news for Canadian investors is that the stock market here is not nearly as over-valued as the major US indices. Looking at the chart below showing the valuation of Canadian (blue line) versus U.S. (black line) stocks, we can see that they have traded in line with one another for most of the past five decades. However there has been a sharp divergence in the past year. That should be no surprise since technology stocks (which are the largest component of most U.S. indices) have been far and away the leaders over the past year while energy and financials stocks (which make up over half of the Canadian index) have lagged. Even during the ‘dot com’ bull market in the late 1990s we saw Canadian stocks trade in line with the U.S. but that was almost solely due to one technology stock, Nortel, which soared to represent an unprecedented 35% of the Canadian TSX Index. But foreign investment flows into Canada are very sensitive to oil prices, so the 20% rebound in oil prices so far in the second half of 2023 suggests that foreign selling of Canadian stocks is likely abating. While we wouldn’t expect Canadian stocks to rally during any sell-off in the U.S., there does appear to be much less valuation risk in our market.

In terms of our overall strategy, it should come as no surprise after reading our comments above that we have been selling into this recent stock strength. Specifically, we have been reducing positions in the cyclical sectors (autos/metals/semi-conductors), U.S. financials and technology. We have maintained overweight positions in energy (on valuation) and telecom (valuation, earnings stability and dividend yield). On top of all the economic, earnings and valuation risks we see, our caution is also heightened by almost all the key investor sentiment measures we look at, which are all far too bullish and very reminiscent of late 2021.

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.