Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

John Zechner

May 30, 2022

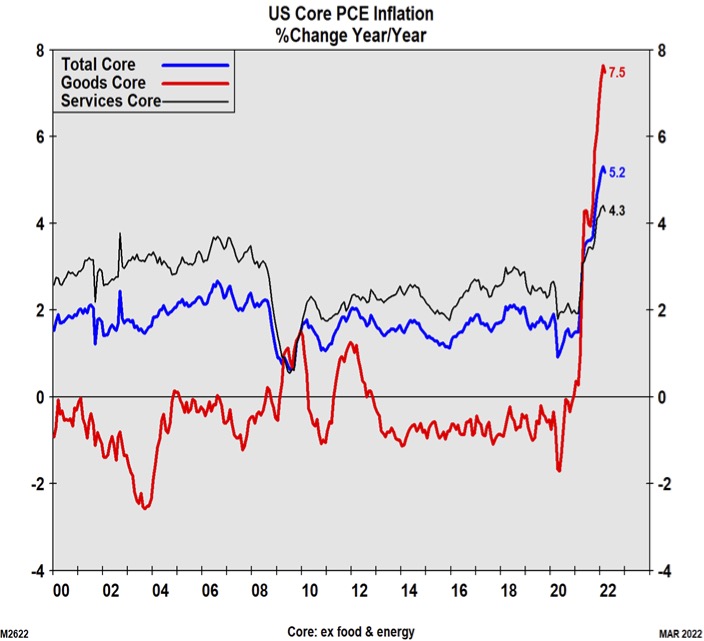

In terms of our overall investment strategy right now, we remain constructive towards stocks despite the risks noted earlier. While stocks were at elevated valuations, we have seen the multiple on the S&P500 fall from over 21 times at the peak earlier this year to around 16 at the recent low, which is close to the long-run average. We recognize that in any bear market stocks rarely stop falling at ‘fair value’ and generally bottom at much lower levels. But we also believe that central bankers may not need to be as ‘hawkish’ as they currently appear, and that the economic downturn can be contained. Most importantly, we don’t see inflation being endemic like it was in the 1970s. While the Fed was premature in calling inflation ’transitory’ last year, now running at the highest level in decades, ‘goods’ inflation has moved much higher than ‘services’ inflation due to the supply chain shortages. As shown below, core ‘goods’ inflation has soared to the highest level in over 30 years, core ‘service’ inflation has remained somewhat more contained in the 4% range, only slightly above the longer-term average. It is still a long way to get core inflation back down to the 2% target range, but stock investors tend to be very ‘forward looking’ and we would expect a very position market reaction from any downturn in those inflation rates.

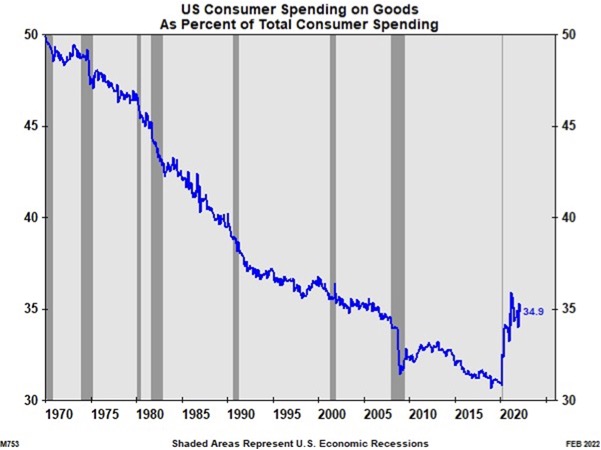

We expect some rebuilding of capacity will start to alleviate those pressures on goods inflation. We have been moving towards a ‘service-based’ economy for much of the past four decades, so the fact that services inflation is not raging is one key to whether the current inflationary spike can be brought back under control. As shown below, consumer spending on goods had been in a secular downtrend for the last 50 years, dropping from almost 50% of total spending to just above 30% before spiking up during the pandemic, when spending on services such as travel, dining out and other social services were basically non-existent. Longer term trends should now resume.

Finally, wage pressures have increased but have not become as endemic to expectations as they were in the 1970s. Moreover, as central banks continue to raise interest rates, growth in employment will slow and labour shortages should retreat, which will also take the edge off wage inflation. Most importantly though, the biggest source of disinflation for the past three decades has been the increasing use of technology, which improved productivity and put downward pressure on the production costs and prices of so many goods and services. Putting it all together, we think we have already seen ‘peak inflation’ for this cycle, which should mitigate the need for central bankers to be as aggressive as many investors fear.

The corollary of that view is that parts of ‘big tech’ are starting to look very attractive, particularly given how sharp the downturn in those names has already been. The basic tenet of stock markets is that they can rise for two reasons; either because earnings are growing or because investors are putting a higher multiple on existing earnings. This latter reason has been responsible for over 80% of the rise in stock prices over the past decade, but is now effectively finished as higher inflation forces up interest rates, thus pushing earnings multiples lower. To find the best stock opportunities now we have to focus solely on where earnings growth will be strongest. While the re-opening of the economy ‘post pandemic’ and the surge in spending generated sharp gains in economically sensitive stocks, those same companies are now expected to see a slowdown as the rising interest rates needed to reduce inflation leads to a slowdown in growth. That leads us back to technology, which as a percentage of GDP spend is expected to double over the next decade. We know that company managements all over the world are going to continue to invest in innovation just to survive and also to take market share. This is unlike the ‘tech bubble’ in 2000; valuations are much lower than they were at that time and the business models are more sound. The measurement metric today is cash flows or revenue growth as opposed to ‘measuring eyeballs’ in 2000. On those more standard valuation measures, stocks such as Alphabet and Meta are trading well below market multiples despite ongoing double-digit growth. Semi-conductor stocks such as AMD and Qualcomm also reported great quarters recently, yet the stocks dropped sharply following those results. AMD has become the dominant player in the high growth data-centre business while Qualcomm has added IOT (internet of things) to its already established high growth business in 5G communications, yet the stock trades at a ‘low teens’ earnings multiple. On a larger scale, in our view, semis are the best growth story in the industrial sector as they continue to be used in almost all devices from phones to laptops to autos to appliances, and are only increasing in importance. The stocks in the sector are also starting to generate higher profit margins as economies of scale increase.

In many ways, the volatility in financial markets so far in 2022 actually makes sense given the uncertainties and heightened risks. What we know is that interest rates are going higher in the short term to bring elevated inflation levels down. What we don’t know is what the economic results will be. Strong medicine for inflation could set off a recession. But the economic and earnings data has yet to reflect that outcome. For now, jobs are abundant, wages are rising, and household and corporate balance sheets look strong. Bullishness during downturns can seem naive. There is a tempting intellectualism to the bearish view as there always tends to be. While we can share those worries until the economic situation starts to sort itself out more clearly, history has shown that the better strategy is to stick with quality stocks and use periods of extreme weakness and heightened fear to add to those positions. Sounds like a good plan to us and we have been acting on it in client portfolios by adding selectively to stocks, particularly in the hard hit tech sector, in the past few weeks.

1 2

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.