Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

John Zechner

May 30, 2022

Last year the U.S. government was still in the process of trying to push through the multi-trillion dollar Build Back Better stimulus plan at the same time that Jerome Powell claimed that rising inflationary pressures were ‘transitory’ and the central bank was ‘not even thinking about’ raising interest rates and would most likely let the economy run at higher levels in order to assure a recovery and raise inflation to its 2% target range. What a difference a year can make as today we have core inflation in North America running at a four decade high rate of over 6% and central banks are scrambling to show investors how tough they can be on fighting inflation by signalling interest rate hikes of over 250 basis points this year at the same time as they move from a ‘quantitative easing’ mode to a tightening where they start selling bonds to unwind the massive stimulus needed to get through the lows of the pandemic. Throw on top of that a stock market that had seen valuations pushed to levels not seen since the ‘dot com’ bubble over twenty years ago and speculation in almost every other asset class (bonds, crypto currencies, EFTs, SPACs) and we should not be surprised that stocks dropped 20% from those peak levels and the high growth Nasdaq Index over 30% before recovering slight in the past week. The initial round of selling had been focused on most of the ‘pandemic winners’ in the high growth sectors (i.e. the social media stocks, streamers, innovation sectors) which resulted in over 50% of Nasdaq stocks falling more than 50% from their peaks. So far this year, the tech-heavy S&P500 has lost just under one-fifth of its value. Among the worst-hit high profile names have been Amazon.com (-36%), Tesla (-38%), Meta (-45%), Zoom (-44%), and Shopify (-76%). As a whole, venture-backed companies that have gone public during the pandemic are down 48%, according to PitchBook. The boom times of the last decade are unambiguously over.

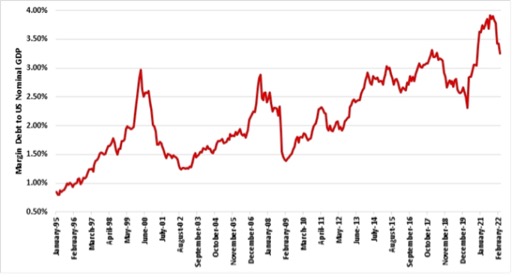

The bigger worry now surfacing for investors in that this aggressive ‘pivot’ in monetary policy by central banks will send the global economy into a recession. The war in Ukraine and the ‘near shutdown’ of the Chinese economy to control another Covid outbreak has only added to those fears. Adding to the risks was the fact that, after two years of strong gains and a decade of ‘easy money’, the stock market was not prepared for a pullback and the simple fact about the current selloff is that we are currently experiencing a deleveraging of the financial system. As shown below, NYSE Margin Debt data, which is a proxy for leverage in equity markets, surged to a record high of almost 4% earlier this year. In the 2000 and 2008 we saw similar peaks which also co-incided with stock market tops. It is one thing for investors who have never seen a downturn before to react calmly to a pullback, but it is quite a different issue when those investments are mostly in borrowed funds!

In the subsequent ‘deleveraging periods’, those figures fell until they bottomed below 1.5% of GDP. One would expect central banks to intervene before we got to that level as they did multiple times in previous episodes. But they appear more commited to getting inflation under control this time around and have less concern about the shorter-term move in stock markets. Recent comments from most US Fed governors has tended to emphasize they plan to raise rates aggessively and their commitment to get inflation under control is the primary objective. But like boxer Mike Tyson was known to have said, “everyone has a plan until they get punched in the mouth.’ The stock market action in April and the first few weeks of May certainly had that feel!

Meanwhile, investor worries catalyzed themselves most clearly in the reactions to earnings reports. Strong reports and guidance increases from the ‘formerly leading’ technology sector (i.e. AMD, Qualcomm, Zoom, Microsoft, Apple, Meta, to name a few) were generally met with some initial buying but then quickly followed by weakness. This has re-enforced the idea that this market has been transformed from a ‘buy the dip’ mode to ‘sell the blip’! On the other side, earnings disapppointment have lead to a decimation of stocks (i.e. Amazon, Snap, JPMorgan, Peleton, Teledoc) with some falling over 30% initially and then seeing more weakness after that.

The initial sell-off in stocks (which took the S&P500 down 20% from its peak and the Nasdaq almost 30%) came from re-valuations of ‘high multiple growth stocks’ due to the rising level of interest rates. If we are going to move into a full blown bear market, it will be because the ‘second shoe’ has dropped on the market and earnings start to miss expectations. The bullish case for stocks had been that consumer spending and employment remained strong and earnings were still growing despite rising inflationary pressures. That narrative has started to change as earnings reports from leading retailers such as Walmart and Target showed the negative impact on consumer spending of inflationary forces on food and gas prices and the squeeze on consumer spending in other categories in addition to ongoing cost pressure from higher wages, product shortages and supply chain problems. Investors turned to selling as both stocks had their worst single day since 1987 on those results.

These ‘earnings warnings’ are the next big risk for the stock market. The newly-found determination of central banks to drive down inflation increases the risk that they do more than simply achieve a ‘soft economic landing’ and actually drive the global economy into a recession. If that becomes the case, then we are only beginning to see the downward adjustment on earnings estimates. The drag on earnings comes from all components, that is, the decline in new orders relative to inventories, the marked increase in the US$, the plunge in retailers’ margin and the surge in labour costs. We have seen mixed results in retail as consumer spednign patterns have changed quickly and companies have not been able to react as quickly due to supply chain issues, leading to both product shortages as well as inventory buildups and subsequent markdowns. Some retailers have adjusted better and more quickly than others, which is why we saw better results from Macy’s, Nordstroms, Williams Sonoma and Costco versus the poor returns from Dick’s Sporting Goods, The Gap, Best Buy and the afore-mentioned Target and Walmart. The ‘pandemic era’ impact on consumer spending has clearly passed and not all retailers have made the right adjustments.

While some earnings estimates have started to fall, analysts in general have not cut their estimates yet, with the S&P500 net revisions still positive. If it comes, that earnings capitulation could come in mid-June, as any pre-releases come in just before the second quarter earnings season. While we have already seen some warnings from the retailers and selected tech companies, most attention will be paid to the ‘mega cap’ stocks, since those are the ones that lead this market over the last two years. In that regard, Apple is starting to look like a poster child for the problems many companies face in a high inflation, low-growth economy. In a recent statement it said it was raising compensation for workers by 10% or more as inflation rises and the labor market remains tight. The company is asking suppliers to assemble roughly 220 million iPhones this year, in line with 2021’s total but well below analyst expectations for 240 million units. A warning also came from the biggest winner in the semi-conductor group, Nvidia, in this week’s earnings conference call release that supply chains problems, China’s Covid policies and even the war in Ukraine are all weighing on its outlook. Despite those warnings, however, the company still sees double-digit growth in its data centre and gaming divisions and the stock actually finished the day up 5% after an initial sell-off of 10%. In tech, the lower expectations may already be built in to stocks!

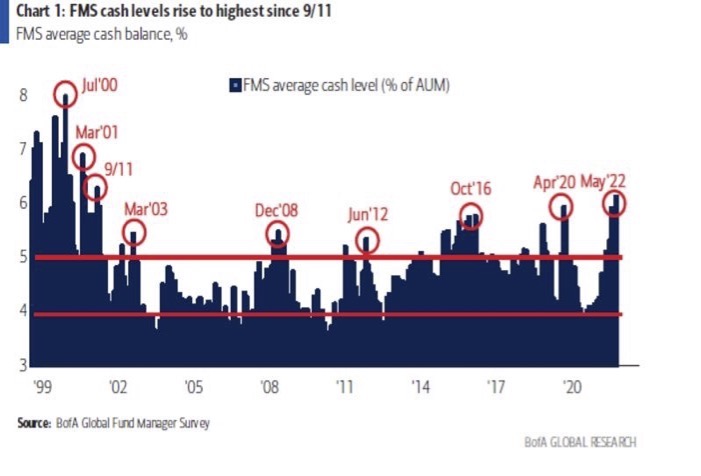

While we have described the potential pitfalls for the markets, we do see some more promising indicators that we could be closer to the lows, especially if the economic downturn is fairly shallow. Sentiment among investors is already quite bearish. According to a recent Bank of America fund manager survey, cash levels among investors hit the highest level since September 2001, with BofA describing the results as “extremely bearish.” The survey also showed that hawkish central banks are seen as the biggest risk, followed by a global recession. Stocks have historically seen their lows when sentiment hits most bearish levels. In that regard, we could be close to a low!

1 2

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.