Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

John Zechner

December 5, 2018

While we have been raising ‘red flags’ about the risks in the stock market for much of the advance in the past two years, our caution is not a lone voice. The U.S. Federal Reserve issued a cautionary note about risks to financial stability, saying trade tensions, geopolitical uncertainty and a build-up in corporate debt among firms with weak balance sheets pose strong threats. In what is often a boiler plate report on conditions in the banking system and corporate and business debt, the Fed instead warned of “generally elevated” asset prices that “appear high relative to their historical ranges.” In addition, the central bank said ongoing trade tensions, which are running high between the U.S. and China, coupled with an uncertain geopolitical environment could combine with the high asset prices to provide a notable shock. “An escalation in trade tensions, geopolitical uncertainty, or other adverse shocks could lead to a decline in investor appetite for risks in general,” the report said. “The resulting drop in asset prices might be particularly large, given that valuations appear elevated relative to historical levels.” The drop in asset prices would make it more difficult for companies to get funding, “putting pressure on a sector where leverage is already high,” the report said. The report further noted that the Fed’s own rate hikes could pose a threat. A market and economy used to low rates could face issues as the Fed continues to normalize policy through rate hikes and a reduction in its balance sheet, or portfolio of bonds it purchased to stimulate the economy. “Even if central bank policies are fully anticipated by the public, some adjustments could occur abruptly, contributing to volatility in domestic and international financial markets and strains in institutions.”

The afore-mentioned Fed report notwithstanding, we continue to believe that we are transitioning from the longest bull market in decades to a bear market! These transitions take time and can see multiple peaks and slow breakdowns, but the key supports for stocks over the past few years are being methodically knocked down. While slowing earnings growth and rising interest rates are creating enough of a ‘headwind’ for stocks on their own, a slowdown in global economic growth is the bigger worry for investor over the next year, in our view.

Last year at this time, most observers were marvelling at the strength of the ‘synchronized global upswing’ and predicting more of the same this year. How things have changed! More recently, it seems like almost every major economy in the world is dealing with some sort of meaningful adversity or sour economic news. Trade wars initiated by the U.S. administration have only added fuel to the economic risks as the intricate supply chains that have supported decades of global expansion are being distorted. Early this year we saw breakdowns in many of the emerging economies from Brazil to Turkey to Indonesia. By the third quarter, this weakness had spread to developed economies as well. German GDP fell at a 0.8% annual rate in the third quarter, pulling the year-on-year pace down to a mere 1.2% clip. The Euro Area overall has cooled to a 1.7% year-over-year growth rate from 2.7% as recently as the end of 2017. In Italy, the budget standoff with the EU continues, with Italy giving only a pledge to increase asset sales to contain debt. Meanwhile, Italian GDP eked out a 0.1% annualized rise in the 3rd quarter, but is up just 0.8% year-over-year. Asia is under pressure as well, evidenced by the fact that Japanese GDP fell at a 1.2% annual rate in the last quarter, pulling down the year-on-year pace to a mere 0.4% clip. Japan is now on track to grow by less than 1% both this year and next. Finally, in the world’s 2nd largest economy, China is grappling with the ongoing trade tiff with the U.S., a full-on bear market in domestic stocks, and a currency that is off nearly 10% since the spring.

Back in the U.S., the National Association of Realtors reported that its pending home sales index, which tracks contract signings for purchases of previously owned homes, dropped 2.6% from the prior month in October. The index was down 6.7% from a year earlier, marking the 10th straight month of annual decreases and another sign that growth in the U.S. may have already seen its best days for this cycle. On the capital investment front, the U.S. 2017 tax cuts were supposed to give a massive lift to business spending, which had been non-existent for much of the recovery that started back in 2009. While business spending accounts for only 10% of U.S. gross domestic product versus 70% for consumer spending, business investment is required to provide economic growth as well as employment gains. But we’ve seen almost no growth for business investment in the third quarter and the monthly data are showing another flat performance for the fourth quarter, which a problem for those who believed that tax cuts would spur on a business spending boom.

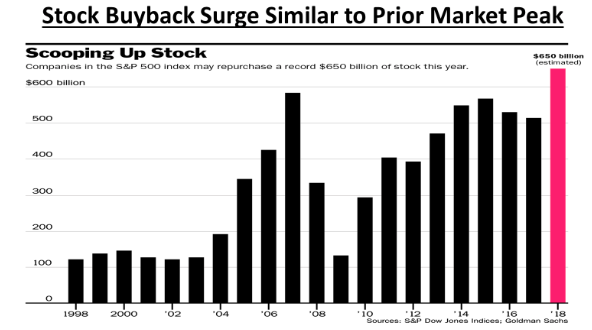

The vast majority of the proceeds from the tax cuts went to extending the share buyback boom. We will need to update the chart below as it now looks like stock buybacks will end up being well in excess of US$800 billion this year!

But that buyback boom seems set to fade in 2019 as some blue-chip firms are announcing a slowdown or stoppage in these programs, and some are doing the same for dividend polices too. Why is that the case? Because triple-B-rated companies, which have a massive US$3-trillion in debt outstanding, do not want to face a downgrade to junk and lose their institutional investor base. Corporate deleveraging will be a key market theme next year. The debt-heavy businesses face a three-year tsunami of refinancings (US$2.5-trillion) and will need to shore up their balance sheets by diverting cash flows toward debt-service repayment and debt retirement. That should slow the flow of money to stock buybacks and will also weigh against the prospect of any business spending boom, will depress economic growth and likely stay the Fed’s hands once it gets to the estimated 3-per-cent neutral funds rate. The theme for 2019 could be one where the end of the share-buyback boom coincides with the end of the earnings boom. That sets us up for a tough year for stocks!

The fallacy of stock buybacks. Shareholders normally love buybacks because they make shares scarcer and inflate a key measure of corporate profitability. But they can also end up being a very poor use of capital if the company runs into trouble or stocks just generally head lower. General Electric (GE) is a key case in point. Their buyback binge was another unfortunate example of buying high. Using a combination of debt and cash, GE spent $2.6 billion last year on stock buybacks in 2017 at an average price of $19.65. GE’s buybacks were much worse in 2016, when it spent $21.4 billion at an average price of $30.30. With the stock now trading below $8, that looks like over $18 billion worth of losses on stock buyback, all for a company that is now selling assets to reduce debt and dealing with credit downgrades, all while still trying to resurrect growth on a much smaller asset base. Clearly those funds spent on buybacks would’ve proved vital today to helping save this historic company.

Share-repurchase shenanigans are not however confined to the dinosaurs of yesteryear. A recent Financial Times article outlined how the five tech companies with the most cash (Apple, Alphabet, Cisco, Microsoft and Oracle) have repurchased an astounding $115 billion of stock in the first three quarters of 2018. By contrast, the total capital spending of those five companies was only $42.6 billion during the same period. President Trump’s tax reform, which lowered the corporate tax rate, was supposed to encourage physical investment in U.S. facilities which would expand employment and extend the economic cycle. With share repurchases in these companies being almost three times their actual investment, one has to question the wisdom of this tax cut in the first place! If you ignore the current stock price, a company repurchasing its shares creates no value. Share repurchases are highly pro-cyclical, pushing up share prices in a bull market and raising the possibility that the company will be short of cash in the next recession. Ask any GE shareholder if they think the share purchases were the best use of its capital.

1 2

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.