Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

Jacqueline Ricci

February 7, 2024

Good-Bye 2023!!

The past year proved to be challenging with the Fed embarking on a rate-tightening cycle to curb inflation and restore it to their targeted level. Consequently, markets experienced numerous fluctuations throughout the year, leaving investors grappling with pivotal questions: recession or a soft landing, persistent rate hikes or a pivot, ongoing global conflicts, and weak corporate profitability amid the tightening cycle.

The fourth quarter mirrored the rest of the year, with investors closely monitoring every utterance from the Fed. At the quarter’s onset, markets witnessed a sell-off fueled by concerns that the tightening cycle would persist “higher for longer,” and Powell would persist until inflation was subdued. However, in December, the traditional “Santa Claus Rally” materialized despite the hurdles. The gains were more widespread than in most of the year. The catalyst for the rally emerged in November when the market sensed that Fed was ready to pivot. In early December, Powell reaffirmed that the Fed wasn’t projecting any imminent reversals in interest rate policy. Instead of interpreting this as a retreat from the perceived policy pivot, investors seemed to overlook the message’s content, considering it another “green light” for easing in 2024.

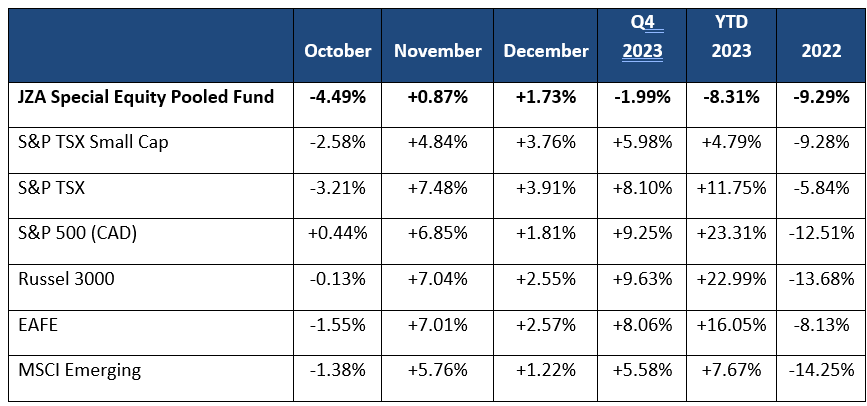

Below is a table of the global market returns including the portfolio. Of note was the incredibly strong performance of the US markets (with the Nasdaq and technology leadership). The Magnificent Seven returned an incredible 111% within the Nasdaq highlighting the importance of large cap this year.

Regrettably, the portfolio did not outperform its benchmark last year. The final quarter witnessed significant tax loss selling in energy and small-cap stocks which offset strong equity markets. In the fourth quarter the portfolio was down -2.0% while the S&P TSX small cap index was up almost +6.0%. For 2023, the portfolio was down -8.3% compared to the benchmark return of +4.8%.

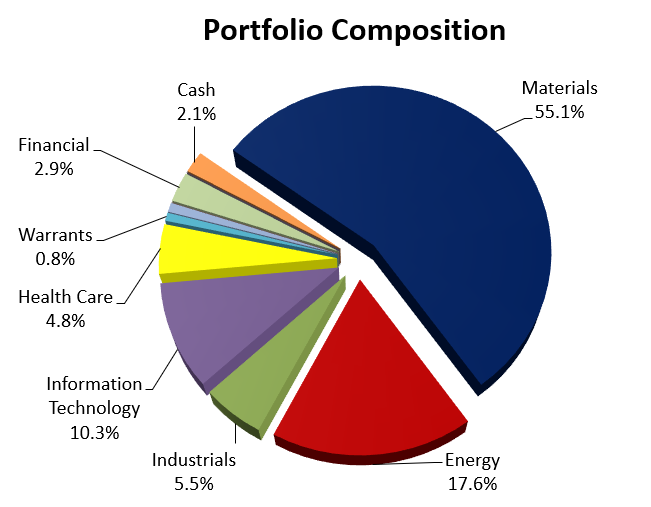

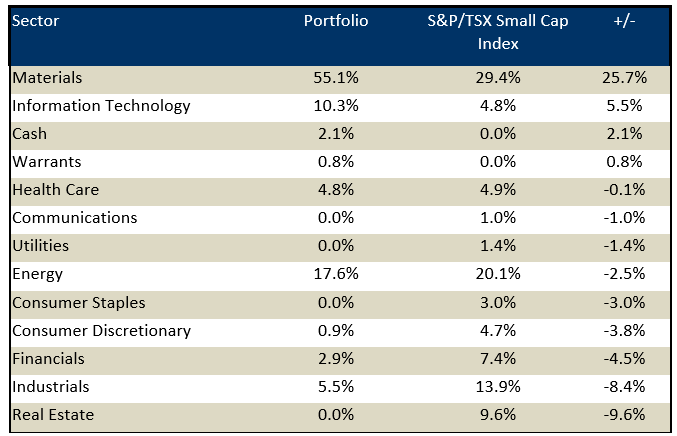

The following charts shows the composition of the portfolio. Through the quarter we decreased the energy sector exposure and added to the golds. We also added to special situation names after two stocks, OpSense and H2O Innovations, were taken out in the quarter.

The three names that most weighed down the portfolio included Horizonte Minerals, Critical Elements and C3 Metals Corp. Collectively, these three names cost the portfolio -2.9%.

Horizonte Minerals, a leading nickel company in Brazil that is currently developing two tier one projects, the Araguaia ferronickel project and the Vermelho nickel-cobalt project, both of which are high grade, low quartile cost and long-life projects. In the 4th quarter, the company announced catastrophic cost overruns which severely impacted their stock price and balance sheet. In late December the company announced a $20 million dollar funding package comprising of equity and debt from their three largest shareholders: La Mancha, Glencore and Orion Resource Partners. Although the funding is dilutive, it is a positive development as the company can continue to move the project forward. While the portfolio weight is very small due to the price depreciation, we continue to hold the position and anticipate seeing some equity appreciation as Horizonte progresses toward production.

Critical Elements Lithium Corporation is a mining exploration company owning several mining operations in Quebec. The Rose lithium-tantalum project is at an advanced stage with a fully permitted project, close to significant infrastructure with a development plan that is low-risk using a single open pit and conventional lithium processing technology which produces technical grade spodumene concentrate used in batteries for e-mobility. The company told investors that they would be revealing a strategic partner by the second half of 2023, which has yet to be announced. The company continues to tell investors they have multiple interested parties performing their due diligence. The stock sold off aggressively in the fourth quarter, as investors lost patience/confidence. It did not help that lithium carbonate prices continued their slide into year end (finishing down -78% last year). We continue to hold the stock as we believe Critical Elements has viable projects and represents excellent value at these levels.

C3 Metals is a junior mineral exploration company creating value through the discovery and development of large copper/gold deposits. The company holds a property in Peru called Jasperoide which sits in a similar geological setting as Las Bambas (MMG), Constancia (Hudbay) and Antapaccay (Glencor). This property provides great optionality. The company also owns 20,700 hectares In Jamaica focused on copper-gold drilling on 16 porphyry targets and 40 epithermal targets. In the fourth quarter the company underwent a share consolidation which saw the stock react negatively. The company is fully funded for their 2024 drill program, and we anticipate more positive news releases over the course of the year.

On the positive side the three names contributing most to performance this quarter included H2O Innovation, OpSens Inc. and GoEasy Ltd. These three names added +1.8% to the portfolio returns.

H2O Innovation is a complete water solutions company focused on providing best-in-class technologies and services. The company applies membrane technologies and engineering expertise to deliver equipment and services to municipal and industrial waster, wastewater and water reuse. H2O also supplies specialty chemicals, consumables and engineered products to the same group of customers. In early October H2O entered into an agreement to be acquired by Ember Infrastructure Management (a US private equity firm) at a +69% premium.

OpSens is a fibre optic sensor manufacturer offering innovative solutions for interventional medical, energy and laboratory industries. At inception this company used fibre optics to test pressure and temperature in the Oil and Gas industry but soon pivoted to develop a significant expertise in the medical field. Their FFR guidewire received FDA approval after many years of testing resulted in a tool that is easy-to-use, saves time and cost but more importantly enhances the success rate in challenging peripheral and coronary interventions by utilizing OpSens’ proprietary miniature optical pressure sensing technology. In early October OpSense announced that it was being acquired by Haemonetics Corporation (US listed public company). The offer was an all-cash offer for $2.90/share, representing a 50% premium to the prior days close. We have since tendered our shares.

GoEasy is one of Canada’s leading non-prime consumer lenders, offering a full suite of products including unsecured and secured loans as well as point-of-sale financing. These loans are made to individuals who have been denied credit by the banks and other traditional financial institutions. GoEasy’s stock was heavily discounted with the onset of rate increases and credit concerns. However, the company has proven over years to be great assessors of credit risk and have lowered their own borrowing cost over the previous years. We added the position in July with the anticipation that interest rate hikes were coming to an end. We continue to hold a position in GoEasy.

Outlook – What’s next for 2024

With Fed Powell adopting a more dovish stance in December, interest rates should drop further in 2024. The current Federal Reserve’s “dot plots” are forecasting three rate cutes over the year while the market (Fed funds futures) is currently pricing in six cuts. The initial cut is most likely in the second or third quarter of 2024, which would be very constructive for Canadian small cap stocks. Interest rate projections are based on inflation falling towards inflation targets amid slower economic growth (but still positive). While a deeper economic slow down and significant recession are possible, currently it is not the consensus forecast. With so much optimism in the market for a “soft landing” we are cautious on equity markets to start the year (especially in US growth stocks after their rally into year end).

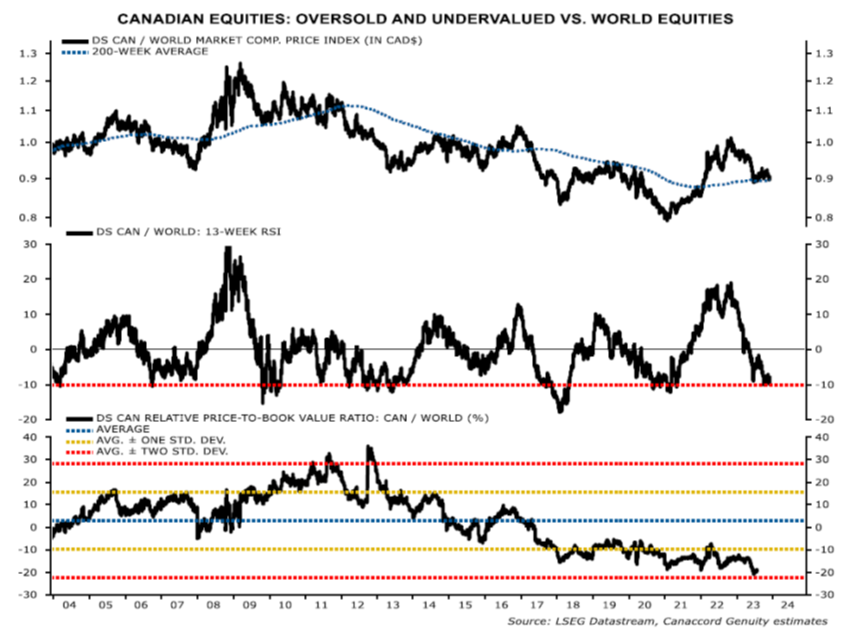

Looking at Canada and small caps we feel much of the negatives have been priced and valuations are more favourable. Below’s chart highlights Canada’s undervaluation relative to world equity markets.

As we look forward to rates dropping in the US, we expect the US dollar to weaken. This should underpin commodity strength and be extremely positive for the portfolio and Canadian small cap tocks. Below are some charts showing the US dollar weakness, the US 10-year yield reversing and the long-term price of gold.

US Dollar – DXY down-trend

US Bonds – 10 Year yield rolling over

Spot Gold – Hitting new highs

Commodity equities are currently at very low levels and provide excellent opportunities for 2024 and beyond. Last year’s weakness was caused by slower growth from China, lack lustre EV sales, high interest rates and fear of a global slow-down. What remains constant is the lack of investment in the base metal/battery metal sectors creating a stagnant supply situation. When demand does begin to pick up, low inventory levels should squeeze prices higher earlier than in prior cycles. Moreover, with new mines being more difficult to find, permit, build combined with geopolitical issues (ex. Panama/First Quantum) our preferred metal continues to be copper with our favorite names being Capstone, Hudbay, NGex and ATEX.

The standout commodity last year was uranium, which rose from $48 to $91 per pound because of low utility inventories and tight supply. Uranium prices should continue to be well supported in 2024 as supply continues to tighten, with the announcement in early January that Kazatomprom’s (the world’s largest uranium miner) would have a production shortfall for the upcoming year. The uranium names in the portfolio include F3 Uranium, Encore, NexGen and Dennison.

Golds in particular look ready for a positive move in 2024. There has been more corporate activity recently with larger producers taking interest in small companies with good assets. The backdrop of lower inflation, a weaker US dollar, government buying and tightening real rates will provide a good backdrop for gold and gold equities. Our investments in precious metals run the gamut with exposure from exploration right through to production. Some of our favorite names include Snowline, ReUnion Gold, GMining, K92 and Oceana Gold.

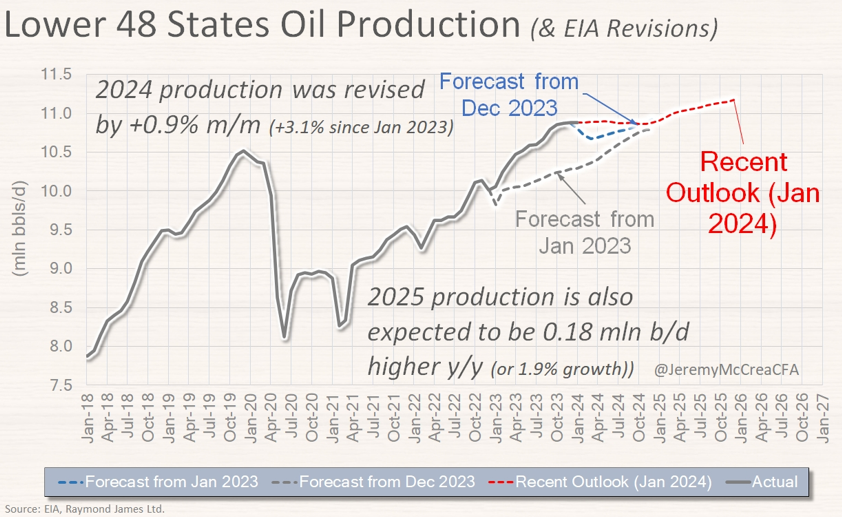

Energy was the last commodity sector to fail last year despite underlying strong demand. Price headwinds were caused by added supply from the releasing of large amounts of US SPR, increasing production from Russia/Iran/Venezuela (2 million bpd collectively) and continued US production growth (see below).

The Saudi’s/OPEC alliance appear determined to keep prices in the $80 plus range for WTI. It is our view that demand will continue to grow at a modest 1-1.5% with much of the “rogue” spare capacity being utilised. We anticipate oil should trade around current levels ($70-$80 range) for the first half of the year, before rising above $90. The Canadian E&P companies are in substantially better financial shape than in the past. These companies have found religion and are spending within their cashflow. Their corporate decline rates have been managed down below 30% and they are putting in policies of returning capital to shareholders in various forms while keeping very strong balance sheets (with very low debt). Our favorite names include Athabasca (with their heavy differential exposure), Headwater, Tamarack Valley, Lycos and Logan.

With winter starting late this year, it appears that gas markets could be challenged through much of 2024. On the other hand, Canada’s first LNG facility will be up and running by early 2025 and should begin loading in late 2024. The first facility, after fully loaded, will export close to 10% of Canada’s gas production. Exporting these gas molecules should be tremendously beneficial to the price of gas within Canada. We will be monitoring the market closely the next few months for an opportunity to add to the portfolio’s gas exposure to see if investors will look through the summer dip in prices. Currently the portfolio is weighted towards oil with some gas exposure from Advantage and Montney players like Kelt and Crew.

The portfolio continues to hold an overweight in technology. With interest rates forecast to fall in 2024, technology growth stocks should continue to do well. This sector was a significant outperformer last year with the Canadian small cap tech sector up +40%. While technology stocks are not cheap, their strong growth should continue to attract investment. Our favorite names include Docebo, Celestica, Nuvei and Kneat.

After being taken out of a few special situation stocks, the portfolio has added: Blackline, a worker safety technology company, Kraken a marine technology company and Source Energy solutions which is a frac sand producer/supplier/distributor.

Last year was a difficult year for Canada and for small cap stocks globally. As we get more clarification that the tightening cycle has ended and global economic growth improving, Canadian small cap stocks should garner significant more attention and bounce back with significant returns for investors.

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.