Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

Jacqueline Ricci

July 28, 2023

The market tone is very similar to last quarter. The Canadian markets are continuing to muddle through; faced with further rate hikes, expectation for the economy to slow down, worries of corporate earning misses and fund outflows with money moving into bonds and the US stock market. Canadian and US central banks continue to focus on inflation with a particular focus on employment and payroll strength. Until they see this data substantially weaken, we anticipate they will continue tightening monetary policy which will be a headwind for equity markets.

The US markets continue to act well, drawing capital from other markets. Technology stocks have been leading the market as the “mega” large cap names break out from previous levels. The small cap tech names have been ok, but nothing close to their large cap counter parts.

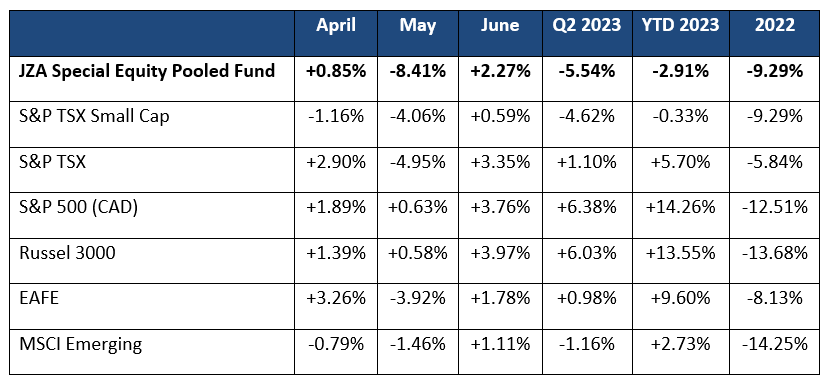

The summer doldrums are upon us. Returns for the quarter in Canada were lacklustre. The SP/TSX Small Cap Index was down -4.6% for the quarter compared to your portfolio being down -5.5%. Year to date the S&P/TSX Small Cap Index is down -0.3% with the portfolio down -2.9%.

Below please find a chart of global market returns for the quarter and year to date.

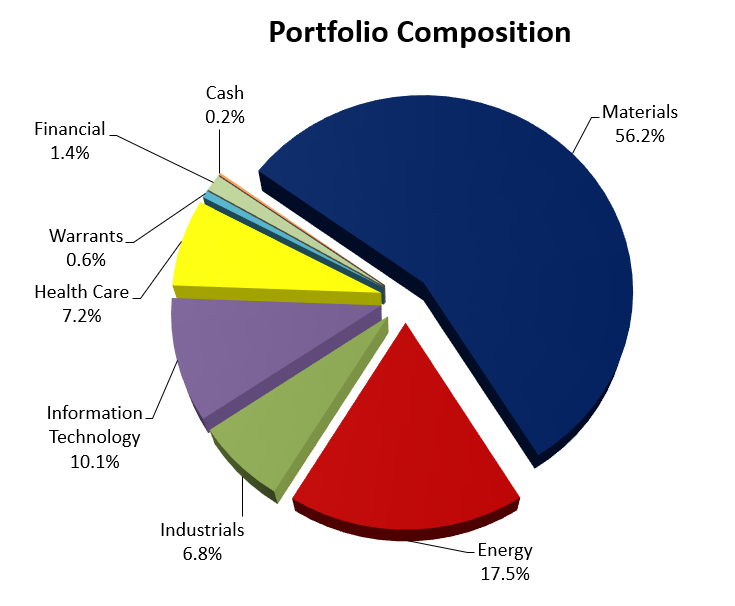

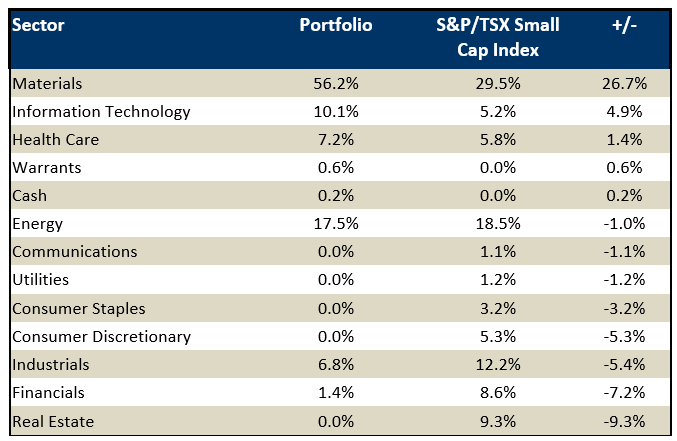

Below are the portfolio and index sector positions as of June 30, 2023:

The three names which underperformed the most in the quarter included K92 Mining, Magna Mining and Atex Resources. Collectively these names cost the portfolio -1.8%.

K92 Mining has been held in the portfolio for many years now. K92 owns the Kainantu Gold Mine in Papua New Guinea. The mine is a high-grade, low-cost underground mine with significant exploration upside. The company was mining a lower grade stope last quarter and experienced some unfavourable ground conditions thus impacting cash flow and earnings. We have added to the position on this weakness and expect this issue to be short lived.

Magna Mining is a Sudbury focused base metal exploration and development company focused on the past producing Shakespeare and Crean Hill Mines. The company has assembled a contiguous land package of over 180 kms. The Shakespeare Project has an existing resource and permits. Management is solid; the same team which developed FNX Mining and sold company in the last cycle. We bought the stock at the IPO and sold some during the initial run up. We have a full position and continue to hold the position as we look forward to more exploration results.

Atex Resources is a Chilean focused exploration company managed by a seasoned team. The flagship property is Valeriano copper gold project in northern Chile. The project is adjacent to El Encierro deposit owned by Antofagasta and Barrick Gold. Last year the company put in their first holes targeting the porphyry system. These holes intersected significant mineralization. Last quarter, Atex was one of the best performing stocks in the portfolio as it was up over +103%. In July the company announced they received further funding from its major shareholder, Pierre Lassonde and we added to the position.

The three best performing names in the portfolio this quarter were Ngex Minerals, Eupraxia Pharmaceuticals and Collective Mining. Collectively these three names added +2.0% to the portfolio returns in the quarter.

Ngex Minerals is a Lundin Group copper and gold exploration company with projects in Chile and Argentina. The Key project is its 69% interest in Los Helados with 17.6 billion lbs. of copper, 10 million oz. of gold and 92.5 million oz. of silver. The excitement in the stock comes from the high grade Potro Cliffs Exploration results which sits adjacent to Filo Mining’s discovery. The first drill hole intersected massive sulphide veins and breccias including 60m at 7.52% CuEq from 212 m. This is a new discovery between Filo del Sol and Los Helados. We maintain a healthy weight and look forward to more drilling while weather permits.

Eupraxia Pharmaceuticals is a clinical stage biotechnology company with a proprietary and innovative polymer-based drug delivery technology. In June Eupraxia reported positive topline data in its Phase 2b Osteoarthritis Trial for EP-1041AR and received fast track designation. The news is significant and propelled the stock higher in the quarter. We did take some profits but continue to hold a core position. The company will most likely do an equity raise off the back of these results. Many new investors appear interested including specialty pharma investors from the US.

Collective Mining is a gold exploration and development company with its main asset located in Columbia. The management team are from Continental Gold. The portfolio had an interest in Continental Gold from discovery through to sale to Zijin Mining. Collective management owns 35% of the company and is rapidly advancing their Guayabales Project where they have made four significant mineral discoveries. The most significant discovery is a high-grade porphyry system at the Apollo target. We like the prospectivity at Collective and the stock is not well followed. We are also bullish on gold and continue to hold a full position even though we have taken some profits to manage the weight in the portfolio.

Looking Forward

As discussed in the last quarterly letter… all eyes continue to be on the Fed to see if they will pivot from their aggressive interest rate hikes and quantitative tightening policies. While the Fed continues to be data dependent, recent data on inflation has improved giving the Fed the ability to pause hiking rates. This appears to coincide with the recent weakness in the US dollar which would be very positive for commodity centric stocks.

Earnings expectations have begun to decline, with the average analyst expecting a -7% decrease in earnings for 2023. The US market hit its low in October 2022 and has experienced a meteoric rise in the last nine months with the S&P 500 index returning over +25%. The Canadian market has underperformed the US (primarily due to foreign outflows). The S&P/TSX composite index is up +12% while the S&P TSX Small cap index is up +9% over that nine-month period.

China’s reopening was supposed to be an offset to the rest of the world slowing down. That thesis appears to have been too optimistic as Chinese data continues to disappoint investors. Policy easing by the Chinese government has also been more muted than anticipated. This is causing investors to become concerned that China’s growth trajectory in the back half of the year will disappoint.

While we do not see the stock market moving materially higher this year, we do believe global central banks are inching closer to the end of the interest rate increases which should stabilize the market and allow investors to focus on individual stock analysis versus macro concerns.

In the first quarter of 2023 we reduced the energy weight in the portfolio. Recently, we have added to the energy weight and are now slightly underweight the energy sector (0.9%). Over the last quarter, we have also shifted the subsector mix in the portfolio by purchasing more natural gas weighted stocks and reducing heavy oil exposure.

The portfolio continues to be overweight copper stocks. While we reduced copper exposure in the portfolio in the beginning of the second quarter, we added to them towards the end of the quarter on US dollar weakness. The portfolio’s gold stocks should also benefit from any US dollar weakness and should act well if the economy weakens.

We named this report “HURRY UP AND WAIT” because it feels like the Canadian small cap market is in a holding pattern. Although we are optimistic that global markets are headed in the right direction and that the portfolio is very well positioned for materially higher returns in the medium and long-term, we are waiting for the macro concerns to abate.

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.