Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

John Zechner

December 2, 2021

It doesn’t seem that long ago that the rhetoric out of the U.S. Federal Reserve (and most central banks) was that they were going to be ‘patient’ in removing monetary stimulus, that the surge in inflation was ‘transitory’ and they were not even “thinking about thinking about” raising interest rates until 2023! All of that chatter went out the window with the November Fed meeting, which was preceded by a 6.2% year-over-year surge in consumer prices which stunned economists, rattled investors, and likely horrified policy makers. It marked the fifth straight month that the consumer-price index exceeded 5%, and signaled the largest jump in consumer price inflation since July 1982. Some of the pricing pressures stemmed from reopening bottlenecks, but there is more to the story as core inflation is now running well above the Federal Reserve’s longstanding 2% target. While markets had been bracing for a ‘tapering’ of the $120 billion/month buying of bonds, many had not expected such an abrupt end. The Fed announced that they plan to reduce these purchases by $15 billion per month, starting immediately. That would fully remove the stimulus by July, 2022, at which point they indicated that they would most likely start increasing interest rates.

Fed Chairman Jerome Powell indicated inflation has become the bigger concern. “The risk of higher inflation has increased,” he said during the first of two days of testimony on Capitol Hill, discussing the pandemic’s effects on supply chains, shortages, and prices. What’s more, he acknowledged that price stability is crucial to getting back to prepandemic labor-market conditions, when the unemployment rate was at a half-century low. “In a sense, the risk of persistent high inflation is also a major risk to getting back to such a labor market.” Taking all of his recent comments and the Fed meeting minutes into account, Treasury markets have now ‘priced in’ a 75% probablility of two interest rate increases before the end of 2022. Since some of this was expected, it didn’t immediately lead to a ‘taper tantrum’ for the stock market like it did in 2013, when a similar ‘adjustment’ in policy was announced. However, it did accelerate a move away from many of the high growth stocks that had the market in 2020 to the cyclical groups that can survive a rising rate environment.

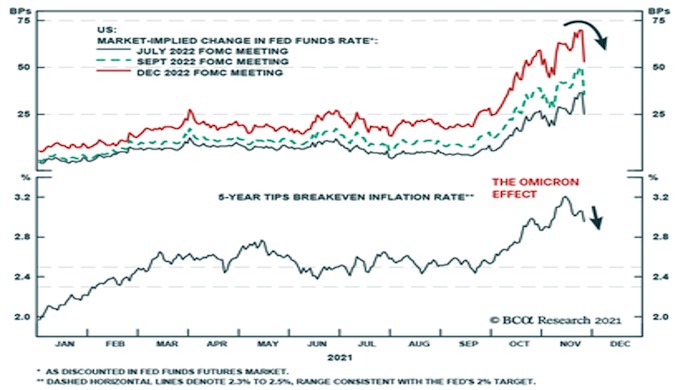

Then that whole trade got ‘turned on its head’ the day after Thanksgiving, when Black Friday shopping was in full force and most traders were away from the office, as headlines of a new COVID-19 variant, called Omicron, identified in South Africa, rocked global markets. Worst hit in that one-day selloff were the energy and travel stocks that had been particularly tied to the re-opening trade. That volatility to the downside continued into month-end, exacerbated by year-end tax loss selling and a ‘sell now and ask questions later’ attitude toward most small and mid-sized companies. The new uncertainty about the virus reduced the expected rate changes slightly, as shown in the chart below, which tracks the ‘implied probability of a move in interest rates.

Then, in the testimony by Powell and Treasury Secretary Janet Yellen to the U.S. Senate the next day, they re-emphasized their newfound commitment to containing inflationary pressures by tapering their bond purchases even more quickly and therefore pushing up the timeline for interest rate increases somewhat more. If you feel like you need a scorecard to keep track of the changes in expectations, you’re not alone!

But even before we get all the data on the effectiveness of the vaccines against this new strain of the virus, we believe the stock market reaction in the past week has been excessive. Countries and businesses are learning to adjust to the reality that the virus will be around for a long time in differing forms and are adapting their operations accordindly. With global vaccine supply increasing and vaccination levels continuing to rise, we don’t see much chance that shutdowns will return. We believe that the 12% plunge in oil prices last Friday was also overblown and driven more by the forced unwinding of short-term trading positions. Predictive models that forecast mobility across North America and Europe have suggested for months now that new case counts are influencing behavior at a level that is no longer statistically significant. Societal behavior is less reactive to new COVID cases now than at any time since the pandemic began, and we saw this throughout the summer with the Delta variant. While the economic recovery will continue to see periodic interruptions, the trend remains up. This growth will support earnings gains which, in turn, support higher stock prices, even if rising interest rates put some downward pressure on earnings multiples. All of this suggests to us that the best investment strategy in this environment is to stick with the ‘recovery trade’ and stock sectors such as energy, financials and basic materials that can withstand higher levels of inflation.

The CPI jumped to a three-decade high in October as supply chain disruptions and holiday-shopping demand fueled inflation across a range of industries. The latest surge in inflation has occurred at a time when debt has ballooned across the economy, making the prospect of higher interest rates particularly problematic. Wages are also rising at nearly a 5% clip, keeping pace with “core” but not “headline” consumer price inflation. Accordingly, labour costs may soon boost inflation and otherwise crimp corporate profit margins. Wage pressures could even accelerate, given that the average worker is experiencing an erosion of their real incomes. Alternatively, if consumers balk at “sticker shock,” demand will slow. The economy might stall. Global fund manager surveys this month identify inflation as the biggest ‘tail risk’, far more than China’s stability, COVID-19 or asset bubbles.

But as hot as October’s report was, some fixed income traders and economists say that inflation in November and December could be cooler, and that last month’s surge could be a peak. That optimistic expectation is based on a recent slide in the Baltic Dry Index, or BDI, a popular measure of global shipping rates used by economists as a leading indicator for inflation. After rising more than 130% over the past year, the BDI has dropped over 50% in the past month alone! Much of this could be attributed to some relief of the congestion at the Los Angeles Port Authority, which is now running 24/7.

1 2

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.