Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

John Zechner

August 27, 2018

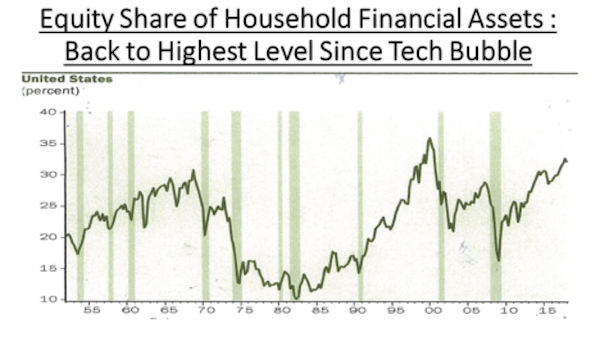

Since the dark days of the Great Recession in 2009, America has experienced one of the most powerful household wealth booms in its history. Household wealth has ballooned by approximately $46 trillion or 83% to an all-time high of $100.8 trillion. Stock market bulls claim that investor sentiment is too negative, that investors are not overly bullish and that this has been a very ‘hated’ bull market, suggesting that many investors have yet to buy into the advance. The data below would appear to contradict that belief as it shows that the share of stocks versus the total financial assets of households in the U.S. has risen to near record levels. From a low of about 15% at the end of the Financial Crisis, the share has risen to over 32% today and has been eclipsed only during the final few months of the technology bubble of the late 1990s, which ended in March, 2000. While there have been many skeptical views about the quality and durability of the bull market, it clearly has drawn investors in and there doesn’t appear to be a ‘wave of liquidity’ on the sidelines waiting to buy into stocks. Other periods when stock ownership has gotten anywhere close to these levels have always ended badly.

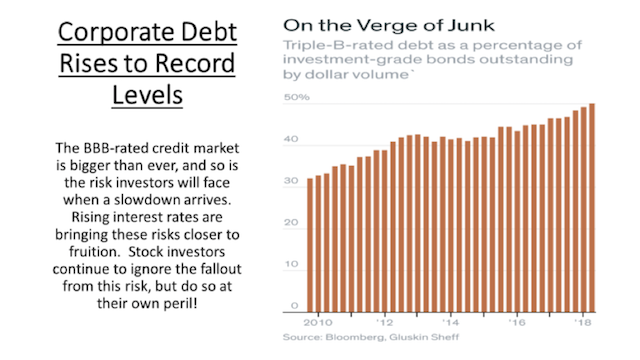

Maybe stock market investors should be taking their cues from the fixed-income markets. Equity investors failed to do that in 2007, to their detriment. At that time, as now, the economic news was generally bullish, commodities were doing well, and other indicators of economic activity were flashing green lights. Even Fed Chairman chief Ben Bernanke supported the positive outlook, suggesting that there was ‘no bubble’ in the U.S. housing market. The bond market, however, was given a totally difference signal as it was ‘flashing red’, especially the high-yield end of the bond market. Sure enough, stocks peaked less than twelve months later and fell over 45% during the ensuing financial crisis and global recession. Now we’re back to a situation where economic growth in the U.S. is exceptionally strong, profits are growing 20% per annum, consumer and business confidence are at record levels and hardly anyone is worrying about risks of a slowdown, especially if you look at the stock market as an indicator. Once again as well, the new Fed Chairman, Jerome Powell, last week suggested that U.S. economic strength will continue and that long-term inflation expectations remain muted. But U.S. short-term interest rates have gone up rapidly and the Federal Reserve remains on course to keep hiking interest rates despite jawboning by the President against the actions of the Fed. Inflation is over 2% and rising and the economy is running near full capacity, so rates will probably need to go higher. Rising rates will cause more nonperforming loans and defaults. What many investors are unaware of is how much debt has been accumulated by corporations during this period of ultra-low interest rates and how the quality of these borrowers has deteriorated. More than 450 investment-grade companies had cash-to-debt ratios more similar to those of speculative-rated (junk) issuers. The deterioration of credit quality means the corporate debt market is in a worse position to cope with a recession than it was on the eve of the 2008 financial crisis.

Stock market bulls also argue that Corporate America’s huge $2.1 trillion cash pile will soften any downward pressure on stocks. That cash horde is double what it was in 2009 for U.S. nonfinancial companies and it could grow further as $1.5 trillion in corporate cash is expected to be brought back onshore under the U.S. tax overhaul passed last year. The new law sets a one-time repatriation rate for untaxed cash held abroad at a 15.5%, with payments to be spread over eight years. Previously, such funds were hit with the 35% corporate tax. This money is concentrated in only a few hands though as over half of that $2.1 trillion is held by just 25 companies, including Apple and Microsoft (MSFT). Stock buybacks should easily reach a new record level this year and could easily exceed US$800 billion! While this does provide support for stock prices, investors at some point may have to question the wisdom of buying back stock at these inflated prices this late in the cycle. General Electric was a major buyer of their own stock and made purchases exceeding $24 billion in 2016 and 2017 at an average price of $30.30, more than double the current price of $12.80. given the company is now stretched financially, selling off assets laying off employees, there must be a realization that the money could have been better spent!

Meanwhile, on this side of the border, the major banks started reporting their third quarter earnings recently and, once again, have been exceeding expectations despite worries about a decline in housing. But the risks to our long bull market in home prices is unfolding. Existing home sales declined 2% in July and activity in the market remains modest with Canada-wide sales at a six-year low. Rising interest rates and record low affordability should bring about a long-overdue consumer deleveraging cycle in Canada, which will also become a growing headwind for the large Canadian banks’ domestic business. Goldman Sachs pointed out in a recent research report that “Canadians are living beyond their means, depending on asset sales and debt to maintain current lifestyles. The private-sector financial balance has proven more powerful in predicting crises than the current-account balance, ‘The good news is that the biggest economies — the U.S., the Euro area, and Japan — are all running healthy private sector surpluses while the ‘not-so-good news’ is that some of the smaller Developed Market economies — especially Canada and the U.K. — are running sizable deficits and appear vulnerable to higher interest rates and weaker asset markets. Canada should fear this economic indicator flashing red’, Goldman Sachs says.

The bottom line for our strategy outlook is that stock market strength has been driven by record low interest rates, strong global growth and rising profits enhanced by U.S. tax cuts. But these are all well known facts. The stock market outlook hinges on future developments. There we see storm clouds gathering! The synchronous global recovery losing steam as a higher U.S. dollar, international trade frictions, record global financial leverage and rising interest rates all put the current expansion at risk of slowdown. We have already seen breakdowns in many emerging markets reminiscent of late 1990s. Copper prices have also been falling and U.S. bond yields stalling, both of which are indicative of slowing growth and put in question the bullish economic outlook painted by the stock market. The ‘zero interest rate policy’ that fueled the shift to financial assets is being removed, which will increase attractiveness of stock alternatives and dry up the giant liquidity bubble that has driven stocks to record valuations. The U.S. remains the sole geography of global growth, but this was due to ‘adrenalin shot’ given to economy through massive tax cuts and deficit spending. But the impact of those tax cuts on earnings will start to fade by the 4th quarter, just as companies are warning that rising input costs and trade risks are putting profit growth at risk. Also, economic stimulus this late in cycle will only raise inflationary risk, meaning that U.S. Fed will need to continue tightening monetary conditions. Debt in the U.S. has risen to a record US$22 trillion and will rise further with deficits expected to exceed $1 trillion annually over next few years. Massive US borrowing needs will eventually lead to a weaker U.S. dollar and should give a lift to commodity prices, maybe even gold. Commodity stock valuations represent one of few valuation opportunities in the stock market. ETF money flows have funded the global bull market but we have seen those flows shift from bonds and global stocks to U.S. technology stocks in the past year. When this bubble ends and the buying turns to selling, valuations will overreact on the downside to the same degree that they have exceeded normal values on the upside in recent years. We are staying conservative with slight overweight positions in cash, short-term bonds and commodity stocks. Have reduced positions in US technology stocks (which remain best long-term growth stories) and maintain market weight positions in US financial stocks.

1 2

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.