Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

John Zechner

August 1, 2018

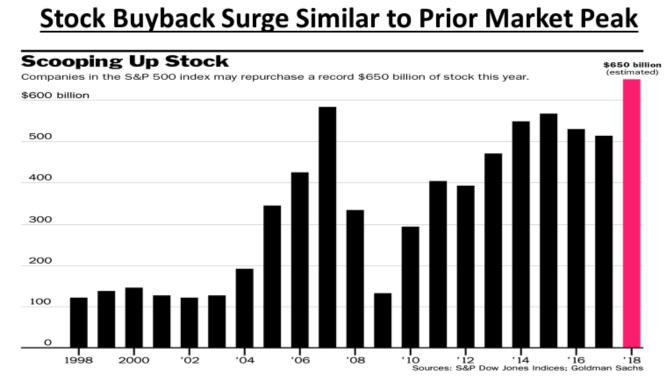

S&P 500 companies are on track to repurchase as much as $800 billion in stock this year, a record that would eclipse 2007’s buyback bonanza. Among the biggest buyers are Oracle, Bank of America and JPMorgan. But 57% of the more than 350 companies in the S&P 500 that bought back shares so far this year are trailing the index’s increase. That is the highest percentage of companies to fall short of the benchmark’s gain since the onset of the financial crisis in 2008. The historic spending spree on share buybacks has some analysts worried companies have gone out and borrowed funds (at low rates of interest) and are now buying their shares at excessive valuations during the peak of the economic cycle and at a time when the market rally is nine years old. Others warn the billions of dollars spent to buy back shares could have gone toward capital improvements like new factories or technology that could lead to stronger long-term growth. Buyback activity reached a frenzy in the early 2000s, just before the stock market peaked. The previous record for share repurchases was $589.1 billion in 2007. Not coincidentally, that was just a year before the stock market tumbled into the worst financial crisis since the Great Depression.

Facebook’s shares wiped out a record $119 billion of market value in just one day on July 25th, which was the largest single day loss of market value for any single stock in stock market history. This large decline was only possible, though, due to the substantial rise in Facebook stock from a market value of about $80 billion at its IPO in 2012 to over US$600 billion at its high last week. But is this sharp sell-off an ominous sign that a shakeout is coming for this group of stocks that connote overvaluation to many investors? The company bought back a record amount of stock in the second quarter—$3.3 billion—usually a signal of long-term confidence in the business. Analysts wondered why the company would do so ahead of a cut in financial guidance.

Its shares fell almost 20% after the earnings release as the company cut its forward guidance on revenue growth and operating profit margins. The stock now trades for 21 times projected 2019 per share earning. The bearish argument is that Facebook is peaking, as user growth slows and expense growth outpaces revenue gains. This was the reason we had sold the stock earlier this year, after owning it for most of its public stock life. We believed that the privacy issues highlighted by the Cambridge Analytica scandal and the necessity of much more spending and hiring required to deal with those issues would lead to lower profit growth. Moreover, we had anecdotally heard about many individuals/groups that were closing their Facebook accounts. Higher costs and lower user growth/engagement would have a negative impact on profit margins, in our view. This indeed became the background for the biggest shocker in Facebook’s new guidance as it sees its operating margins, now at 44%, trending down to the “mid-30s” in the coming years. Most analysts had expected little erosion in those margins.

There are many analysts still putting forward the bullish case for Facebook despite its recent sharp price drop. It remains a powerful platform, with 1.5 billion daily users, strong engagement, and no major competitor. They still point to Facebook as basically the only megacap company with a reasonable valuation whose revenues could grow 25% next year, among the highest organic growth rates for companies with market values of $100 billion. Facebook also has a strong balance sheet with $42 billion of net cash, or $14 a share. In our view, this is a bigger issue than just the move in Facebook stock. What is most important about the fall Facebook is we believe that similar dramatic drops in some high-flying technology stocks this month is further evidence the stock market will go lower. Economic growth with slow down in the 2nd half of 2018, profits have peaked for the cycle yet the Federal Reserve cannot slow down its interest rate increase agenda since the economy is running nearer to full capacity and inflation has worked its way back into the mix. The combination of slower growth and higher interest rates will have negative implications for both stock valuations and profit growth. Those variables had been separately or together supporting higher stock prices for most of the past ten years. We believe we are at the end of that cycle and don’t see how stocks can rise significantly given that background.

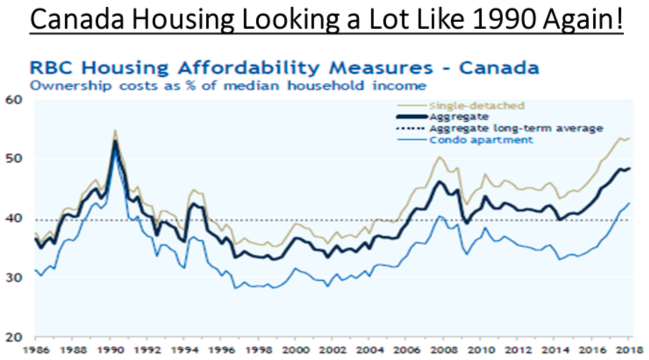

Investors need to remember how important interest rates have been in lifting financial asset and real estate prices and the risk we could see as that support wanes, particularly since consumer, business and government debt levels have risen to record levels. As an example of this, a recent survey done in Canada shows that 28% of respondents said another interest rate increase will hurdle them toward bankruptcy and another 42% say if rates rise much more they’d fear for their financial well-being. While both readings were down modestly from the previous quarterly survey, that’s not lessening the alarm. When you look at the staggering number of people who are teetering on the edge, it’s clear that we are going to start seeing a rise in delinquencies as rates rise. The Bank of Canada has raised interest rates three times since last summer and has indicated more rate action may lie ahead. This can be seen clearly in the chart below, which shows Housing Affordability in Canada, which in the past two years has risen back to the peak seen in 1990.

1 2

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.