Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

Jacqueline Ricci

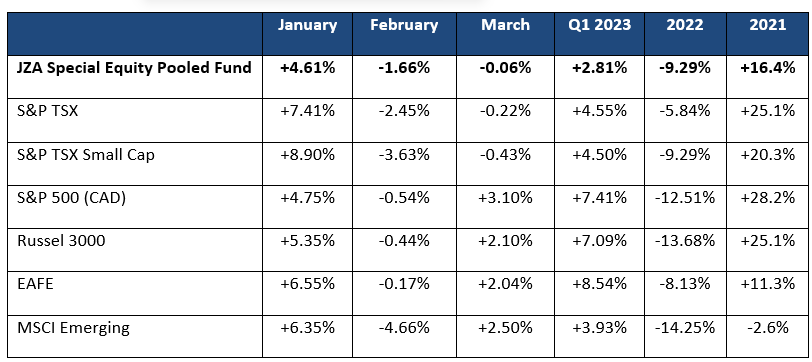

Given the volatility at the back half of 2022, the expectation for the new year was understandably apprehensive. Much to investors surprise, January started on a high note with markets showing strength to start the year. By late January the TSX Small Cap Index had advanced by +8.9%. Perhaps it was the hope/expectation that the Fed would soon pivot and begin the easing cycle that drew investors back into the market driving up prices. That expectation however did not last, as it became clear that the Fed was not about to pivot, and that fighting inflation was still their prime focus.

As tighter for longer set in, the energy sector became the latest market victim. After holding up relatively well through last year’s turbulent market, energy became the worst performing sector in the TSX for the quarter ended March 31, 2023, with a negative return of -3.6%.

With more pressure on interest rates, and the Fed’s musings that the ultimate level of interest rates is likely to be higher than previously anticipated, and that he was looking to realign supply with demand with the monetary policy transmission mechanism which likely will hurt employment and wages. Post the Fed’s statement, Silicon Valley Bank (SVIB) reported an asset/liability mismatch, igniting fears of a Global Financial Crisis like contagion. This event rippled through financial markets putting downward pressure on risk assets and upward pressure on safe-haven assets. Gold showed its strength as a safe-haven asset with the gold price advancing by +8.0% in the first quarter to trade through the US$2,000/oz level.

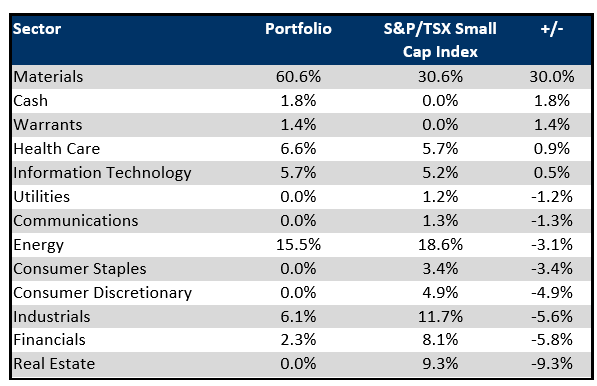

If the quarter wasn’t eventful enough, OPEC decided to make an unexpected cut to oil supply. With oil trading below $65/barrel, this cut had the immediate impact of moving the oil price through the $80/barrel level. This did provide relief for the sector, but the stocks continue to be priced lower than when oil was previously at the $80/barrel level. OPEC decisively showed the market that they wanted the oil price to trade above the $70 level and that OPEC was less than interested in seeing US strategic reserves to be replenished at bargain basement prices. Below please find a chart showing the TSX Small Cap Index returns for the first quarter and showing a comparison to other global markets. Note that the portfolio underperformed the S&P TSX Small Cap Index by -0.95% in the quarter.

For the quarter, there was a resurgence in the large cap technology stocks, but this did not filter down to the small cap names. The outperformance came from those companies with positive earnings profiles and companies with room to improve their margins through cost cutting. Small cap tech names are largely earnings negative and therefore did not participate in the run up. Technology and financial stocks were amongst the worst performers in the TSX Small Cap Index.

On the positive surprise for the quarter, despite concerns for ever increasing interest rates, base metals prices remained firm. Copper largely held the $4.00/lb level for much of the quarter, mainly because of the positive expectation of Chinese demand after China opened its economy post the COVID lockdown and the overall tightness of supply. The base metal stocks were reasonable performers in the quarter.

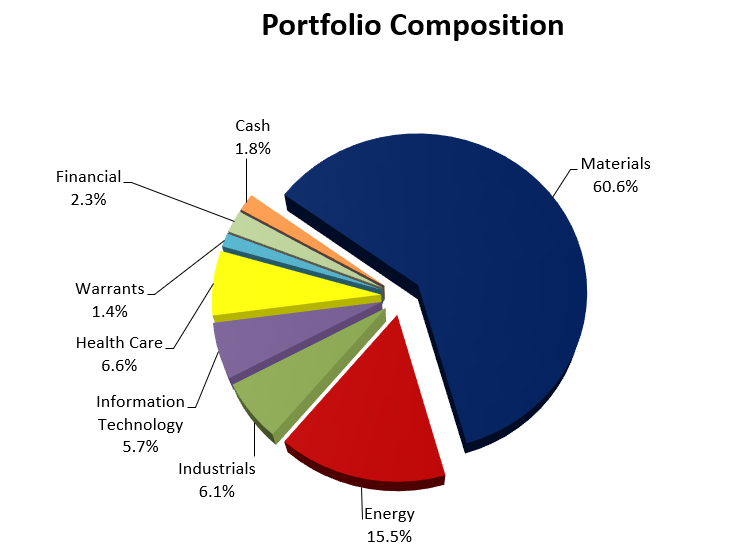

Below are the portfolio and index sector positions as of March 31, 2023:

The three names which underperformed the most in the quarter included Clean Air Metals, STEP Energy Services and Calfrac Well Services. Collectively these three names cost the portfolio -1.2%.

Clean Air Metals is a Canadian based platinum and palladium exploration company focused on advancing its flagship Thunder Bay North Critical Minerals project located in the Thunder Bay region of Ontario. In February, the company withdrew their previous mineral resource estimate and PEA pending a restatement. The expectation is for a material reduction in the metal content in the current deposit. The discrepancy is due to the different estimation methods used by two independent engineering companies. Given the companies need for further financing and the material negative news that was announced we have decided to exit the position.

Step Energy Services and Calfrac Well Services are energy service companies. At the beginning of the year our expectation was for energy to hold its $75/barrel level. With the sector outperforming and abundant cash flow we added to the service sector expecting continued tight market conditions for the services these companies provide. As the energy market faltered and the WTI price looked to be heading towards the $60 level, the service sector stocks began underperforming given the expectation of a reduction in cash flows of the energy sector which would translate into lower drilling activity thereby directly impacting service stocks. We have exited both positions. With the decline in energy stock prices, when OPEC announced their supply cut, we added to the exploration and production companies.

The three names that contributed the most to the portfolios returns include Atex Resources, Capstone Copper, and G Mining Venture. Collectively these three names added 2.1% to performance in the quarter.

Atex is a copper exploration company with its flagship property, Valeriano copper project located within the Link Belt in north-central Chile. The company is focused on delineating and growing the copper-gold porphyry resources underlying a surface oxide gold deposit. Drill results to date confirm the presence of a major copper-gold porphyry system that is open in all directions. The property sits adjacent to the El Encierro deposit of Antofagasta and Barrick Gold. We have history with this management group and are very excited about the opportunity. We continue to hold the position.

Capstone Copper has consistently been one of our larger positions in the portfolio. It follows our thesis of a very tight copper market in the next few years, largely from underinvestment on the supply side and strong demand growth as we move towards electrification and diminish our reliance on hydrocarbons. Capstone has a portfolio of long-life copper operations in the Americas and a fully permitted development project in one of the world’s most prolific copper-producing districts (Chile). As they develop their permitted projects Capstone will continue to lower their cost of productions given these lower cost projects. We like Capstone’s portfolio of assets and their ability to grow with internal generated cash flows. We continue to hold our Capstone position.

G Mining Ventures was formed in 2021 to pursue direct ownership of precious metal projects and capitalize on the value that successful mine development leads to. This management team over the previous 15 years were leaders in mining project execution. With a combined cost of $2 billion dollars of construction spending, this team has delivered 100% of their projects at or below budget and on schedule. Since forming G Mining Ventures, the company has acquired a 2-million-ounce resource project called Tocantinzinho in Brazil. They are currently in project and have hit all milestones. We have confidence that this management team will deliver on this project and anticipate that they will be acquisitive to further their production pipeline. Building a mine on time on budget is extremely challenging but this teams history has us extremely positive on the prospects of this company going forward. We continue to hold the position.

Outlook for the remainder of 2023

To pivot or not to pivot…that is the question. The first quarter of 2023 has proven to be quite eventful, but one thing is clear, despite SVIB and other weakness in the banking sector, the Fed is sticking firmly to their tightening bias and fight against inflation. The traditional path of an economic slowdown is taking place with rising rates. Interest sectors such as housing have rolled over, businesses have started to see a slowdown as evidenced by the layoffs in both technology and financial sectors. The consumer has remained resilient, but this is largely because employment has remained strong. As mentioned earlier, many believe the Fed will not pivot until Chairman Powell sees weakness in employment data.

Are we heading into a recession? Much of the data would indicate, yes. The question is the severity of the recession. The market hit a significant low last October and has been climbing a “wall of worry” ever since. When the recession finally does arrive, it will have been the most widely anticipated downturn in history. Despite slowing demand in many sectors, underinvestment in many commodities over many cycles have helped keep supply/demand very tight and is keeping commodity prices somewhat elevated. China’s reopening after being shutdown during COVID has also added to demand.

Although we do not see a runaway bull market, we are optimistic that we are closer to the end of rate increases. We expect markets to muddle through as investors continue to look out over the horizon for the recession to begin. Our positioning has changed somewhat with us being underweight energy early in the first quarter, expecting demand for energy to decline. Our gas weight has been substantially reduced as we expect weakness throughout the summer as no additional takeaway capacity in the form of LNG has been added, thereby making it more sensitive to economic activity in North America. Post the OPEC supply decrease we reduced the oil underweight as it seemed that OPEC wanted to manage prices above the $70/barrel level, a decent level for most producers.

Gold remains a defensive position for the portfolio. Providing a haven during economic instability (as seen through the SVIB crisis) but also being well position for when the turn in interest rates occurs. The portfolio has a higher percentage of producers as these companies are trading at strong free cash flow yields.

Copper is also a significant weight within the portfolio. The mid to long term outlook keeps us extremely bullish. Under-investment and runaway demand for the energy transition should sustain higher copper prices for longer. Short-term however, copper is very sensitive to any global slowdown, despite the long-term fundamentals and tight inventories. This current tightness and China’s importance with respect to copper demand is the reason we remain overweight despite economic headwinds. Not to mention the improved balance sheets of the base metal producers and their willingness to be active in M&A.

Post the technology selloff, we have added to the sector and continue to look for interesting small cap names that are able to weather the recession fears. We have also added exposure in the small cap industrial sector with names like Savaria, H2O Innovations and AG Growth International.

While we are optimistic that we are through the worst of the market selloff, we anticipate continued volatility and expect several more stock corrections over the next few quarters until inflation falls to the central bank targets (between 1%-3%).

As always, would love to hear from you if there are any questions or thoughts you may want to share.

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.