Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

John Zechner

November 1, 2022

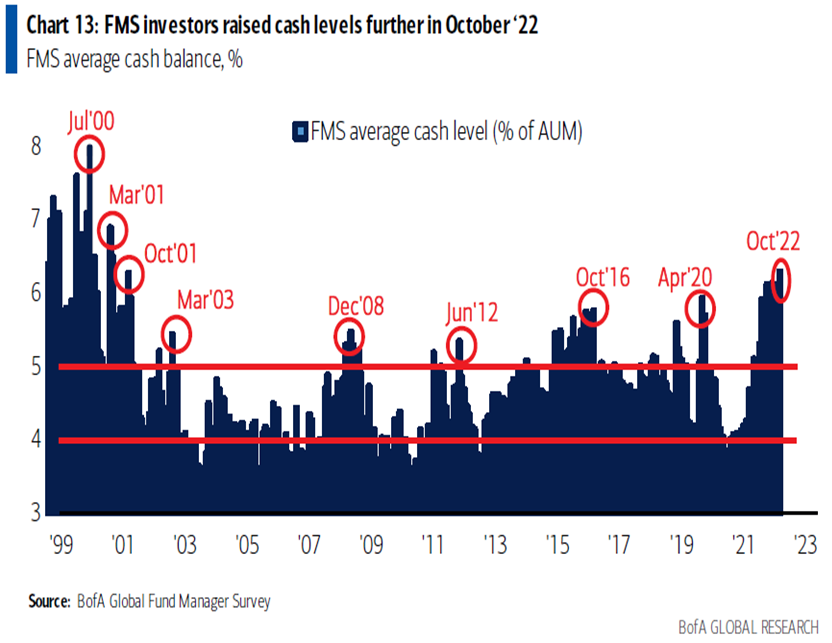

Right on cue, when investors seemed to be at their most bearish and the outlook dismal, the stock market suddenly runs out of sellers and stocks rally. That has been the story so far in October, which got the traditionally strong fourth quarter off to a good start despite a mixed picture from the reported earnings results, with ‘big tech’ faltering. The backdrop of bearishness was in plain view after a miserable September and overall year so far in 2022. Sentiment on stocks and global growth among fund managers surveyed by Bank of America showed full capitulation, opening the way to an equities rally. The bank’s monthly global fund manager survey “screamed investor capitulation.” Market liquidity deteriorated significantly,” the surveys said, noting that investors have 6.3% of their portfolios in cash, the highest since April 2001, and 49% of participants were underweight equities. Nearly a record number of those surveyed said they expect a weaker economy in the next 12 months, while 79% forecast inflation will drop in the same period, according to the survey of 326 fund managers with $971 billion under management. While the stock market has reflected investors’ pessimism about the outlook for all of 2022, it seems prudent to point out that such periods of high cash in the past have often coincided with major market bottoms.

Meanwhile, in the stock market, there seemed to be a ‘sea change’ of the sort not unlike what we saw in the aftermath of the bursting of the ‘tech bubble’ in 2000. The quintet of the biggest tech names have been viewed and owned as safety stocks, a growth trade, and a play on fortress profit margins that have been vacuuming up cash from the rest of the market for over a decade, with four of the five achieving ‘previously unheard of’ market capitalizations of over a trillion dollars each! Now these ‘megacap technology’ names have morphed into ‘market dogs’. Big tech’s fall from grace has eroded its influence over the market-capitalization weighted S&P500 Index this year to the lowest since April 2020. Mega-cap technology names that have reported earnings this past week have lost more than $500 billion in aggregate value with Alphabet, Amazon, Meta and Microsoft all offering concerning commentary for the third quarter and the remainder of the year. Between slowing revenue growth — or declines in Meta’s case — and efforts to control costs, the tech giants have found themselves in an unfamiliar position after unbridled growth in the past decade. Third-quarter results this week came against the backdrop of soaring inflation, rising interest rates and a looming recession. Only Apple bucked the trend after beating expectations for revenue and profit.

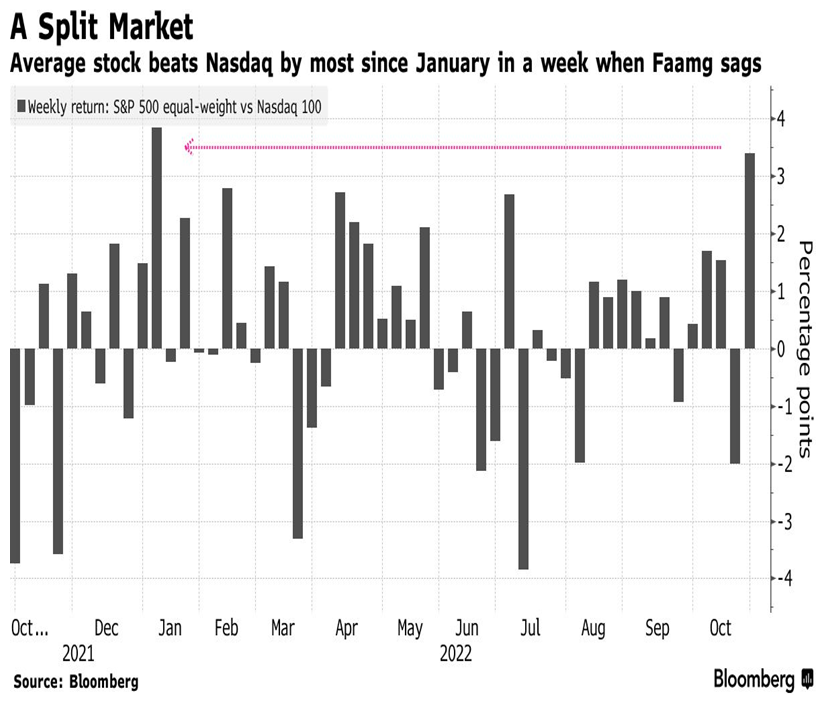

Still, at 19% of the benchmark, Apple, Microsoft, Alphabet, Amazon and Meta Platforms hold bigger sway than the utilities, energy and consumer sectors combined. Together, the five companies have lost a combined $3 trillion in market capitalization this year alone. All things considered, this is not the worst news for stock market bulls. While these ‘market favourite’ stocks are getting crushed, investors continue to rotate away from tech, finding money-making opportunities in other parts of the market that had previously lagged behind software and internet names. The Dow Jones Industrial Average rose 3% in the past week, the fourth weekly gain in a row for the index. Prior to 2021, the Dow had underperformed the Nasdaq for five straight years. The earnings reports were also supporting this move. While the big tech stocks disappointed the street with earnings and/or outlook, old ‘rust belt’ companies such as Caterpillar and General Motors reported robust numbers and strong end markets. Ditto for the big energy players such as Exxon and Chevron and money centre banks such as Bank of America, Citi and JP Morgan. The chart below shows that the most recent weekly move in the S&P500 versus the Nasdaq Index had its best week since January.

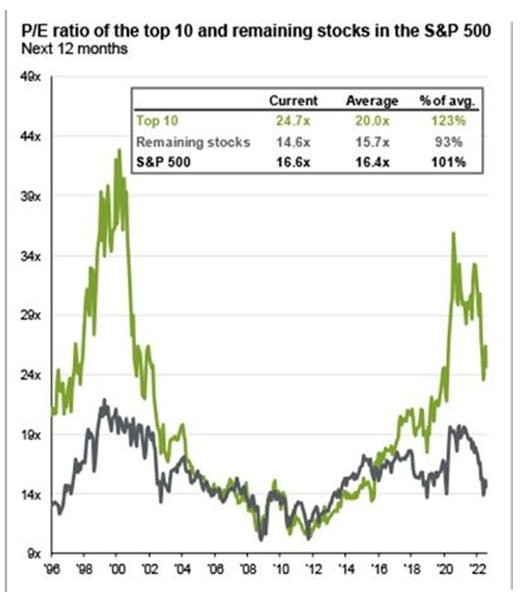

The other reality about big tech is that those stocks have become ‘over-owned’ due to the fact that they were over 25% of many widely-owned index funds such as the S&P500 and the Nasdaq100. As those positions continue to unwind we might see more short-term selling pressure in that group compared to the rest of the market. This again is similar to what happened in the 2001-2003 period in the aftermath of the deflated tech bubble. A final factor supporting a shift away ‘big tech’ to the rest of the market is the relative valuation. As shown below, while valuations have come down across the board in the 2022 sell-off, the largest ten stocks in the S&P500 still sell at over 24 times earnings while the other 490 sell at an average earnings multiple of only 14.6 times, well below the long-term average. With growth in the larger stocks slowing, the opportunities in the rest of the index are becoming more apparent.

In terms of our investment strategy for the balance of this year, we added to both stocks and bonds during the September sell-off, believing that investors were positioned too bearishly heading into what is traditionally the best period of annual seasonal strength. The stock market hit some interim lows in mid-June and then re-tested those levels twice in October and held both times. That improves the chances that the June lows might end up holding. With all of that in mind, we added back to energy stocks (Whitecap Resources, Crescent Point Energy and Suncor Inc), banks (Scotiabank, Citi, Bank of America), consumer discretionary (GM, Magna, BRP, Air Canada) and some tech (semi-conductors Qualcomm and AMD as well as Paypal and Lightspeed). We also added some 10-year bonds to the portfolio and reduced cash balances to minimal levels. Clearly there are still many risks facing investors, not the least of which are rising interest rates and slowing economic growth, but we feel that most of those risks have been accounted for in current stock valuations. While there might be more weakness and volatility in the short-term, we don’t see substantial potential downside for stocks in this scenario.

Meanwhile, the Federal Reserve in the US meets again in the first week of November and is widely expected to hike interest rates by another 75 basis points, pushing them into the 3.75-4.00% range, the most aggressive series of rate hikes that investors have seen in modern history. Much of the rally in stocks we have seen so far in October, beyond the fact that stocks were supremely ‘oversold’ and overdue for a bounce, was premised on the view that we might also see some moderation in the tone of hawkishness from Fed Chairman Jerome Powell in the press conference following the Fed meeting. While investors don’t see any reversal of rate increases in the near term, they are hoping that the Chairman might indicate that the rate hiking cycle is coming to an end soon with economic growth slowing and inflation moderating. The Bank of Canada laid some of the groundwork for such a call in the past week when they raised interest rates ‘only’ 50 basis points at their meeting, rather than the consensus estimate of another 75-point rate increase.

1 2

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.