Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

Jeff Herold

In May, the preferred share market, like the Canadian bond and common equity markets, declined in value. Resilient economic data and little to no progress on reducing inflationary pressures during May forced the markets to increase the likelihood of interest rates staying higher for longer. While the Bank of Canada did not adjust monetary policy in the month, several other central banks, including the U.S. Federal Reserve, continued to push interest rates higher. The month also featured concerns about a possible default by the U.S. government as it negotiated an increase to its anachronistic debt ceiling. Although the funding crisis was eventually resolved very late in the month, the uncertainty contributed to the market weakness. Another factor behind the weakness in the preferred share market was selling by preferred share ETFs as they continued to experience net outflows. The S&P/TSX Preferred Share index ended the month with a return of -3.57%. During the month, the performance of each issue type (perpetual, rate reset, and floating rate) in the index was broadly in line with the overall market return.

Economic data released in May suggested the Canadian economy strengthened in April following modest weakness in March. Canadian GDP was reported to have had little growth in March, but that was better than expectations of a decline. More importantly, growth for the first quarter was robust at an annual rate of 3.1%, with final domestic demand, and in particular consumer spending, looking much stronger than in the second half of 2022. Additionally, StatsCan’s flash estimate for April showed growth resuming at 0.2%. The GDP data indicated surprising resilience in the face of the Bank of Canada’s series of rate increases over the past year. Unemployment held at the low rate of 5.0% with job creation again beating forecasts, and the housing sector, which had slowed last year in reaction to higher interest rates, showed signs of stabilizing. The number of homes started exceeded expectations and sales of existing homes jumped 11.3% with prices rising for the second consecutive month. Inflation was well above forecasts at 0.7% in April and accelerated to 4.4% on a year-over-year basis. The Bank of Canada did not have a rate setting meeting in May, but the stronger than expected data on GDP, employment, housing, and inflation put pressure on the Bank to consider resuming rate increases.

Every few years, the U.S. government struggles to have the limit on its permitted amount of debt increased. (Unlike almost all other countries, including Canada, the U.S. separates its budgetary approval of spending from a plan to finance that spending.) This year, the debt ceiling debate attracted more attention than usual because the especially polarized political climate in the U.S. made bipartisan agreement appear less likely. Without agreement to raise the debt ceiling, the U.S. government would potentially default on its Treasury bills and bonds, creating financial chaos. While an agreement to suspend the debt ceiling until January 1, 2025 was eventually reached late in the month, the uncertainty for much of May likely contributed to the selloff of bonds as international investors exercised caution about holding U.S. debt.

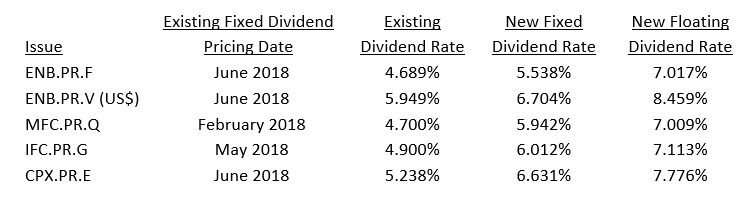

In May, there were no new issues of either traditional $25.00 par orinstitutional preferred shares. During the month, five series of preferred shares, including a U.S. dollar denominated issue, reset their dividends. Dividend rates continue to reset significantly higher because the 5-year Canada bond yield continues to be substantially higher than five years ago. Details of the resetting issues were as follows:

During the month, Enbridge announced that 1,827,695 of its outstanding ENB.PR.F fixed rate series were tendered for conversion into the ENB.PR.G floating rate series. Therefore, on June 1st, it will have 18,172,305 ENB.PR.F and 1,827,695 ENB.PR.G shares outstanding. The creation of the floating rate ENB.PR.G shares was unusual, because investors in the last few years have rarely expressed sufficient interest in switching to floating rate shares even though their dividend rates have risen well above the fixed rate alternatives. To that point, Enbridge also announced that an insufficient number of holders of ENB.PR.V wanted to make the switch into the floating rate series and all shares will remain fixed rate ones for the next five years. Similarly, National Bank announced that too few holders of NA.PR.E (which was reset in April) wanted to make the switch into the floating rate series and all shares will remain fixed rate ones. Investors in MFC.PR.Q must make their decision on converting into the floating rate series by June 5th, while investors in IFC.PR.G and CPX.PR.E have until June 15th to make their decision.

As noted above, preferred share ETFs experienced outflows in May with persistent selling by retail investors forcing ETF managers to sell the underlying preferred shares. The seven largest ETFs had net outflows of $91 million, with all but two days in the month having net daily outflows. In other ETF news, Brompton Funds announced that it plans to launch the Brompton Split Corp. Preferred Share ETF, which will be the first ETF focusing on split share corporation preferred shares in the Canadian market. There are approximately 30 Canadian split share corporations, concentrated in the financial sector, with over $5 billion in preferred shares outstanding.

J. Zechner Associates Preferred Share Pooled Fund

The fund returned -2.51 % in May, which was significantly better than the S&P/TSX Preferred Share index return. Fund outperformance was largely a function of security selection that included an approximate 13% allocation to institutional preferred shares and Limited Recourse Capital Notes that are not in the S&P/TSX Preferred Share index and which outperformed the index.

In May, portfolio activity included switching positions in CVE.PR.C into CVE.PR.E, FFH.PR.C into FFH.PR.K, and MFC.PR.I into MFC.PR.Q to pick up incremental yield.

Outlook and Strategy

As noted above, the yield of the 5-year Canada bond continues to be substantially higher than five years ago resulting in substantial increases in dividend rates on resetting issues. Despite this dynamic occurring over the past year, preferred share prices have trended lower, thereby producing the highest yields in many years. Indeed, several bank issues have yields above the previous highs of 6.25% to 6.50% seen in 2009. In addition, given the advantageous tax treatment of dividends, preferred shares look very attractive versus alternative fixed income instruments. We believe rate reset issues will continue to benefit from sharply higher dividend rates when they reset, particularly those with reset dates in the next few months and potentially further in the future if interest rates remain higher for longer.

We anticipate the annual rate of inflation will fall substantially in the next month as the outsized increase of 1.4% in May 2022 is dropped from the calculation. Indeed, the annual rate may fall below 3.5%, but the fight against inflation is not nearly over. With consumer prices up more than 2% in the first four months of 2023, inflationary pressures are clearly still too high. And with high profile wage settlements such as the recent ones for federal civil servants (12.6% over four years plus a $2,500 one-time payment) and WestJet pilots (24% over four years), the risk is that a wage-price spiral is adding to the existing demand-pull inflation. At its rate setting meeting on June 7th, the Bank recognized this by increasing its interest rate by 25 basis points to 4.75%, and expressing concern over excess aggregate demand, inflation expectations, and wage growth. Its accompanying statement was interpreted by many as leaving the door open to another 25-basis point increase in July depending on the strength of the economic data between now and then.

Paradoxically, the good economic news in May makes us more concerned about a recession beginning later this year or early in 2024. The resilience of the Canadian and U.S. economies to date following substantial interest rate increases suggest even tighter monetary policy will be required to bring inflation sustainably down to the 2% target. That raises the likelihood of the economies reaching breaking points with sudden sharp retrenchments, rather than achieving so-called “soft landings”. The experience of the 1980’s, when inflation had become entrenched as it is currently becoming, suggests that inflation can only be curbed with a significant economic contraction that results from a substantial reduction in aggregate demand.

Notwithstanding a possible recession, we continue to remain confident in the creditworthiness of the issuers in the portfolio, as these companies have successfully weathered previous economic downturns without impacting their ability to pay the dividends on their preferred shares.

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.