Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

John Zechner

June 29, 2023

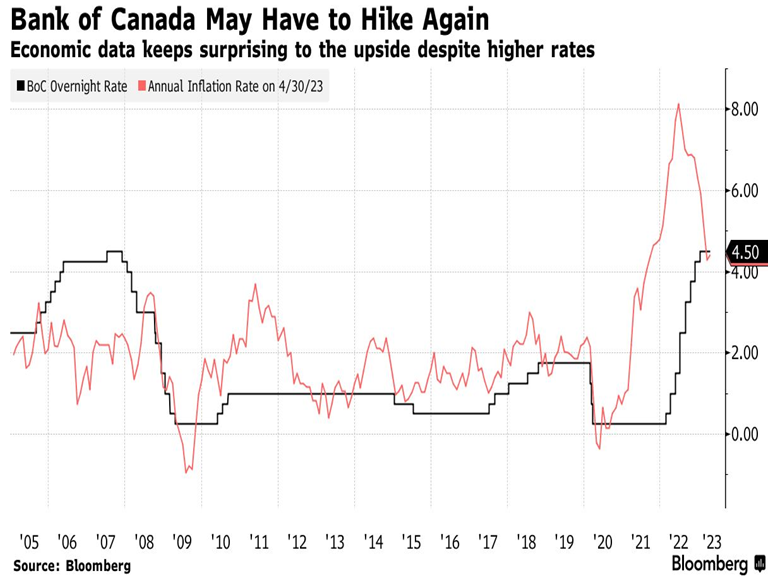

Not only do we expect economic weakness from the rate increases already enacted, we don’t think that central banks are finished yet. In the past month we saw the Bank of England surprise markets by raising rates by 50 basis points rather than the expected 25 basis point increase while we also saw the ECB raise rates by another quarter point and indictate that they have yet to bring inflation down to desired levels. While the Bank of Canada surprised the market in March by taking a ‘pause’ in their rate rising schedule, they did come back in June with another quarter point rise. Going into this year, the consensus view was that Canada’s deeply indebted households would quickly cut back spending as they absorbed higher rates, causing the economy to slow down earlier than other nations that aren’t so exposed to bloated home prices and mortgage debt. Canada’s economy grew at a 3.1% annualized pace in the first quarter, stronger than projected, while employers added 344,000 jobs in six months. Consumer spending has been steady. It’s prompted some to change their minds about how tight monetary policy needs to get to bring inflation to heel. The June rate hike took the short-term interest rate to 4.75%, the stronger employment report has the consensus now seeing rates moving to at least 5.0% and perhaps higher depending on the inflation readings over the summer.

The continued hawkish vigiliance of central bankers has more to do with the ongoing economic strength than any disappointment on inflation, which has been falling as expected. While it’s difficult to pinpoint the primary cause for the surprising economic resilience, the unusual nature of the pandemic-induced 2020 recession and the ensuing recovery seems to be at the core of the reaction as this has blunted the normal impacts of rate hikes. In 2020 and 2021, the U.S. and other governments provided trillions of dollars in financial assistance to households that were also saving money as the pandemic interrupted normal spending patterns. Meanwhile, central banks’ rock-bottom interest rates allowed companies and consumers to lock in low borrowing costs for longer time frames, thus limiting the initial impact of rising interest rates. This economic momentum has been sustained. Households and businesses continued to spend heavily and families tapped their savings, which were replenished by solid income growth and pandemic payouts. Businesses kept hiring thanks to pandemic-related labor shortages and large corporate profits. Normally, the Federal Reserve’s rate increases force heavily indebted consumers and businesses to rein in spending because they have to pay more to service their loans. But consumers haven’t overextended themselves with debt and household debt service payments now account for only 9.6% of disposable personal income, below the lowest levels recorded between 1980 and the onset of the pandemic in March 2020.

In terms of how this economic backdrop and forecast impacts our current investment strategy, we remain slightly underweight stocks because valuations are at the high end of the historical range, interest rates have risen sharply and therefore are less supportive of those valuations and the probability that we are in a recession before the year is over is quite high. Cash is providing an attractive return option right now but we don’t expect to see interest rates remaining at this high level a year from now, paritcularly if our forecast for pronounced economic weakness in the back half of the year is accurate. Bonds, on the other hand, look like a great ‘hedge’ for stock exposure at this time. They provide income levels that are higher than they have been in over a decade. Meanwhile, bonds could rally if economic weakness and inflation reduction occur as we expect. Stock market moves and economic information come in every day and we will continue to incorporate that information into our strategy on finanical markets overall as well as individual companies. In terms of industry sector positioning, we currently find the best ‘risk adjusted’ return probabilities in the cyclical sectors that are already reflecting recessionary economic conditions. Energy and consumer cyclicals lead that list but we also added some base metal (copper) and fertilizer positions in the past month as those stocks have lagged the overall market so such a large degree. We are not yet adding banks to the mix since they face headwinds from increased loan loss provisions, slower capital markets activities and tigher capital requirements. But valuations are also starting to get to very attractive levels and the dividend yields are quite high. U.S. banks will lead the earnings parade in mid-July so we will monitor those results and outlook closely before adding.

Technology once again shows why it is a growth industry that has earned the premium valuations that stocks in the sector have been awarded. Tech stocks have lead the charge upward in 2023, with the biggest names dominating the gains in the major indices. Most investors, ourselves included, have not been fully invested in the ‘magnificent seven’ that have lead the charge so far this year since the valuations seems pretty extended, but we have to acknowledge that tech stocks have once again proven that they deserve the premium earnings multiples that have defined this industry since its major growth started in the mid-1990s with the public rollout of the internet and early search engines. The short history of the technology industry has given us a bit of a ‘roadmap’ to how it has successfully ‘re-invented itself’ on numerous occasions when it looked like it had reached a plateau and would become cyclical in its growth, like the consumer, industrial, resource and financial sectors.

After 2000 most businesses had upgraded their hardware and penetration had reached most segments of the economy, suggesting that some slower growth was expected, but then came the age of social media and smartphones, with Facebook, Apple and Google all driving much more consumer traffic to the internet and pushing to a new era of growth for those companies. Then, after the financial crisis, tech spending seemed to be slowing down again as companies cut back on IT budgets and consumer penetration of devices seemed to reach capacity. Once again new applications came to the rescue as that was when the new ‘cloud’ companies, lead by Microsoft and Amazon, pushed businesses to move their data and applications to third party services and away from their own desktop and laptop computers. That same expansion of networks and service providers later gave way to ‘streaming’ companies (Netflix, Amazon Prime) that drew consumers back to their devices in massive numbers and sustained growth right up to and through the pandemic. Then, in 2022, the most recent test of the industry came as central banks moved away from a decade of zero interest rates to the most aggressive tightening of policy ever seen, bringing down the valuations of growth sectors such as technology as well as raising fears about an economic recession. Tech had grown to be such a large part of the economy by then that it seemed unrealistic to believe that their growth would not be impacted by any slowdown in the economy, especially since businesses like advertising had high economic sensitivity and online advertising had basically grown from zero to the largest single source of advertising in the past decade. We did initially see a wave of layoffs from Amazon, Microsoft, Facebook (Meta), Shopify, Alphabet, etc. to get their cost structures in line with reduced revenue outlook. But then the industry once again showed how it can re-invent itself with a new source of growth as artificial intelligence (AI) saw a surge in spending with new applications such as ChatGPT bringing in new business and consumer users. While it seemed we were going to a bit of a repeat of the 2000 tech bubble with regards to the hype around AI, the most recent earnings report from NVIDIA (the poster child for the growth of AI in its GPU chips) absolutely blew through expectations and provided guidance that made analysts upgrade their growth for this industry dramatically. Other chip makers, AMD and Marvell, came out with similar comments that really showed the tech industry had once again re-invented itself and earned the premium valuations that these stocks get, even in a period of higher/rising interest rates. Whether these valuations and growth projections actually come to fruition is still now known but, for now, the onus is on the bears and skeptics to prove that these stocks are really not worth those nosebleed valuations!

1 2

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.