Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

John Zechner

October 13, 2017

Looking at some other asset classes, bonds had an extremely difficult month and quarter as stronger economic conditions pushed central banks to a more ‘hawkish tone’ on interest rates, with the Bank of Canada joining the U.S. Federal Reserve in raising short-term interest rates. The FTSE Canadian Bond Index fell 1.3% in September and 1.8% in the third quarter and is up only 0.5% so far in 2017. Preferred shares, on the other hand, have continued to do well with the S&P/TSX Preferred Share Index gaining 1.7% in the third quarter for a year-to-date gain of 10.8%, following on the 7.0% return in 2016. The 5% yields as well as a growing institutional investor following have lead to stronger money flows, even from non-taxable accounts, to this sector.

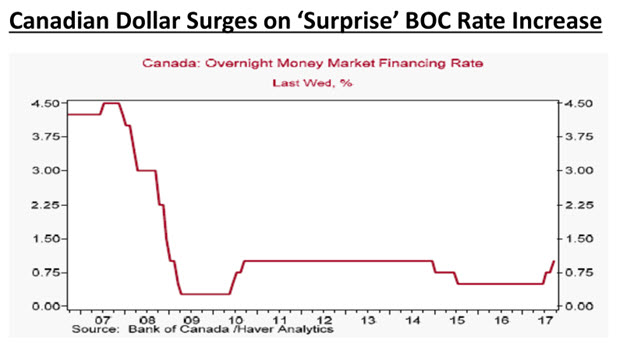

While the recent moves by the Bank of Canada to raise short-term interest rates have lead to a sell-off in bonds and a further rise in the Canadian dollar, we have to recognize that this ½ point increase in rates only reverses the ½ point cut in interest rates that took place in early 2015. Those interest rate cuts were in response to the collapse in oil prices from over US$100 barrel in late 2014 to a low of under US$30 per barrel in early 2016. That fall in energy took a sharp toll on the Canadian economy, especially in Alberta. The strong recovery in the past year has allowed the Bank of Canada to take back those cuts, as shown in the chart below.

The bigger question now is where these markets go for the balance of 2017 and beyond. The key to the outlook for stocks depends, in our view, on continued momentum in global economic growth which, in turn, remains dependent on a 2nd half pick-up in U.S. growth. Optimism about tax cuts and deregulation has pushed economic confidence to new highs while employment continues to grow. While global growth has been an upside surprise this year, we remain skeptical about further gains in stock prices. More than 80% of the rise in U.S. stocks since the 2016 election has been due to higher valuations for stocks, rather than earnings growth. Meanwhile, profit margins have most likely peaked for this cycle as input costs are starting to rise again. While earnings growth was strong in the first half of 2017, those were being compared to a very weak first half of 2016. The year-over-year comparisons will become more difficult in the back half of this year and we expect only about 5% growth in the U.S. and slightly better results in Canada due to a recovery in oil prices. Another problem is that Investors have also been taking on a higher level of risk in their portfolios to offset the fact that interest rates are too low to provide a viable alternative. In the process they have become totally complacent about stock market risk, as measured by the fact that stock market volatility remains near record lows. We also now have the U.S. Federal Reserve beginning to ‘drain the large pool of liquidity’ that was driving stocks higher as they start to sell their existing bond holdings to reduce their US$4.5 trillion balance sheet. Higher interest rates and the reduction of the U.S. Fed’s balance sheet will turn a ‘tailwind’ for stocks into a ‘headwind.’ We haven’t had a stock market correction in over 18 months, a bear market in over six years and we are more than eight years into a recovery; all of which are far longer than normal.

Historically there has been a correction in stocks at least once a year and a full bear market every four to five years, and those declines tend to be anywhere from 20-40%. The reason we haven’t seen such a pullback since the financial crisis is, in the view of ourselves and many other investment commentators, due to a ‘liquidity bubble’ created by the Federal Reserve’s zero interest rate policy, which has also attracted global interest as other central bankers go down the same path. But now these programs are starting to unwind and we are heading for higher yields. This would lead to a huge reset of pricing in the risk markets, which would mean lower stock prices. The U.S. stock market, trading at 21 times operating earnings, 100 months into a business expansion and all the potential geo-political risks coming out of Washington suggests there’s very little reward but of a lot of risk. We continue to invest accordingly.).

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.