Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

Jeff Herold

November 6, 2019

Bond yields have fallen over the last year primarily due to two risk factors. The first is the ongoing trade dispute between the United States and China, and the resultant negative impact on global trade. A second, and somewhat less impactful, factor has been the uncertainty surrounding Brexit and the possibility that Britain would leave the European Union without a negotiated agreement and thereby trigger economic chaos. Both factors were diminished in October, increasing the likelihood that bond yields will rise in coming months. The trade talks between the U.S. and China appear to be making progress toward an initial, partial agreement to be finalized later this month. If that occurs, we would expect bond yields to rise. With regard to Brexit, the risk of a no-deal departure has been substantially reduced with the extension of the departure date to January 31st. The election in the intervening period may result in greater certainty regarding Britain’s decision to leave or to stay, given that it will likely be a referendum on the agreement negotiated by Boris Johnson with the EU. Whichever the result, the lower risk of a chaotic departure lessens the safe haven bid for bonds, allowing yields to rise. With both risk factors looking to shrink in importance, we are keeping portfolio durations shorter than benchmarks.

The yield curve is currently saucer-shaped with mid term yields below those of both short and long term bonds. We do not expect this to last very long. Unless the Bank of Canada begins lowering interest rates soon, which we do not expect, mid term and long term bond yields will face increasing upward pressure. Accordingly, we are structuring the portfolio to benefit from a steepening of the yield curve.

We do not anticipate a recession in the next year or so, so we are comfortable with the current overweight allocation to corporate bonds. However, we recognize the potential for a slowdown has increased, so we are carefully reviewing the creditworthiness of every holding and looking for opportunities to lower overall risk. With benchmark Canada bond yields at historically low levels, many investors have chosen to look for higher yields by buying lower quality, investment

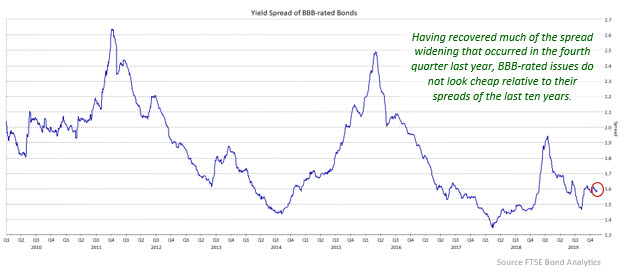

grade corporate bonds. BBB-rated issues, which comprise close to 42% of the corporate sector, experienced sharply higher spreads in the risk-off environment a year ago. Since then the spreads of BBB bonds have retraced most of that widening. Current yield spreads, however, are relatively narrow compared with the experience of the last decade. In other words, the risk/reward trade-off is not particularly favourable. Accordingly, we are monitoring the market for opportunities to reduce the BBB exposure in the portfolio.

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.