Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

Jeff Herold

November 6, 2019

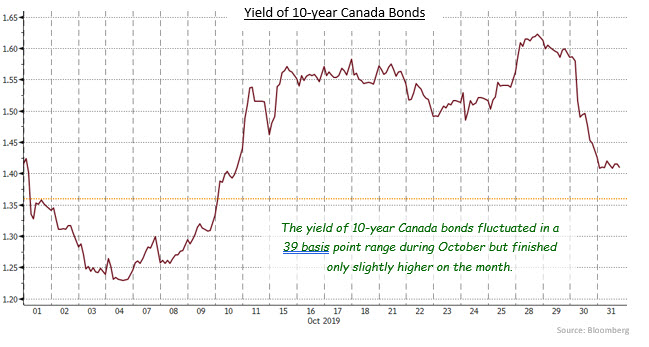

Global bonds moved in wide ranges during October as investor sentiment about economic growth swung from pessimism to optimism and back. On the first day of the month, surprisingly weak U.S. manufacturing data caused global bond yields to drop as investors feared slowing growth. Yields continued to fall until, later in that week, robust labour market data suggested the U.S. economy in fact remained in very good shape. Bond yields moved sharply higher the following week due to optimism that the United States and China were close to agreeing to a partial settlement of their trade dispute. In addition, as the month progressed the likelihood of a no-deal Brexit declined and the safe haven demand for bonds diminished as a result. Bond yields hit their highest levels of the month two days before the Bank of Canada and the U.S. Federal Reserve made their respective interest rate announcements on October 30th. The two central banks each did as expected, but surprisingly the market reaction was a sharp rally in bond prices and a plunge in yields over the next two days. As a result, yields were only slightly different from month earlier levels despite the wide fluctuations that occurred during the month. The FTSE Canada Universe Bond index returned -0.17% in October.

Canadian economic news during October was mixed. Unemployment fell to 5.5% from 5.7% as job creation was very strong for a second consecutive month. Other good news saw the trade deficit shrink as exports grew more rapidly than imports. As well, housing starts remained strong and building permits increased more than expected. Less positively, the Canadian economy as measured by GDP grew somewhat less than expected in both July and August, leaving the year-over-year increase at only 1.3%. In addition, both retail sales and wholesale trade disappointed. Overall inflation held steady at 1.9%, but the Bank of Canada’s three measures of core inflation edged higher to 2.1%. The federal election had little discernable impact on the bond market.

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.