Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

John Zechner

June 8, 2023

Resilient economic data and little to no progress on reducing inflationary pressures during May forced the bond market to recognize the likelihood of interest rates staying higher for longer. As expectations of interest rate cuts later this year faded, short term bond yields rose sharply, and longer term yields followed in a more muted fashion. While the Bank of Canada did not adjust monetary policy in the month, several other central banks, including the U.S. Federal Reserve, continued to push interest rates higher, which contributed to weaker bond prices. The month also featured concerns about a possible default by the U.S. government as it negotiated an increase in its anachronistic debt ceiling. Although the funding crisis was eventually resolved very late in the month, it contributed to the weakness in bond prices in the period. The Bloomberg Canada Aggregate index declined 1.76% in May, while the FTSE Canada Universe fell 1.69%.

Economic data suggested the Canadian economy strengthened in April following modest weakness in March. Canadian GDP was reported to have had little growth in March, but that was better than expectations of a decline. Additionally, StatsCan’s flash estimate for April showed growth resuming at 0.2%. More importantly, growth for the first quarter as a whole was robust at an annual rate of 3.1%, with final domestic demand, and in particular consumer spending, looking much stronger than in the second half of 2022. The GDP data indicated surprising resilience in the face of the Bank of Canada’s series of rate increases over the past year. Unemployment held at the low rate of 5.0% with job creation again beating forecasts. As well, the housing sector, which had slowed last year in reaction to higher interest rates, showed signs of stabilizing. The number of starts beat expectations and sales of existing homes jumped 11.3% with prices rising for the second consecutive month. Inflation was well above forecasts at 0.7% in April and accelerated to 4.4% on a year-over-year basis. The Bank of Canada did not have a rate setting meeting in May, but the stronger than expected data on GDP, employment, housing and inflation put pressure on the Bank to consider resuming rate increases at its June 7th meeting.

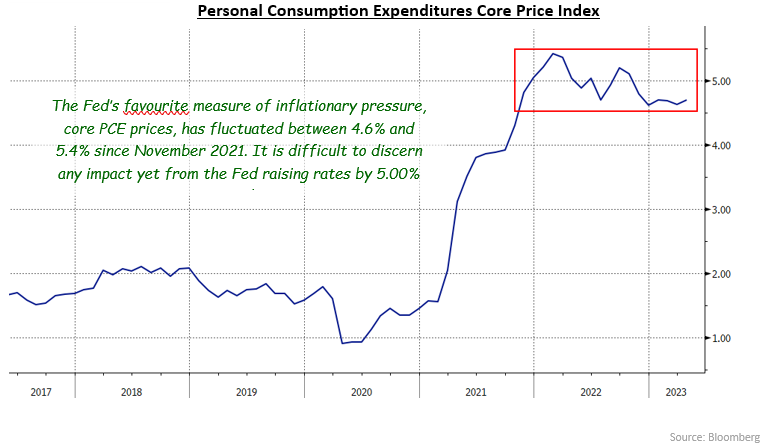

U.S. economic data showed a similar pattern to Canada, with activity improving in April after some weakness in March. The labour market remained very tight as unemployment declined to 3.4% (the lowest since 1969), job creation remained robust, and the number of unfilled job openings jumped back above 10 million. The important manufacturing sector rebounded as factory production was stronger than expected and orders for capital goods accelerated. Inflation remained problematic with the annual increase in CPI declining only marginally to 4.9% from 5.0%, and the core rate moving to 5.5% from 5.6% the previous month. Early in May, the Fed increased its interest rates by 25 basis points, and subsequent comments from Its Chair, Jerome Powell, suggested that it would consider pausing rate increases at its June 13-14 meeting. However, subsequent resilient economic data pointed to the need for further increases. Of particular note, the Fed’s preferred measure of inflation, the Personal Consumption Expenditures Core Prices, actually increased slightly. As can be observed in the following chart, there has been little improvement in inflation since the Fed raised rates by a cumulative 5.00%.

Every few years, the U.S. government struggles to have the limit on its permitted amount of debt increased. (Unlike almost all other countries, including Canada, the U.S. separates its budgetary approval of spending from a plan to finance that spending.) This year, the debt ceiling debate attracted more attention than usual because the especially polarized political climate in the U.S. made bipartisan agreement appear less likely. Without agreement to raise the debt ceiling, the U.S. government would potentially default on its Treasury bills and bonds, creating financial chaos. While an agreement to suspend the debt ceiling until January 1, 2025 was eventually reached late in the month, the uncertainty for much of May likely contributed to the selloff of bonds as international investors exercised caution about holding U.S. debt.

International developments in the month were mixed. Inflation was higher than expected in the U.K. and Italy, but lower than forecasts in Germany, France, and Spain. Remarkably, each release of inflation data provoked brief responses in North American bond markets as if they were domestic, not foreign, news. During May, the central banks of Europe, England, Australia, New Zealand, and Norway each tightened 25 basis points, continuing the global trend to higher rates. In China, the economic rebound from the pandemic appeared to be losing steam, which caused global commodity prices to fall and bond prices to strengthen because of the potential depressing effect on inflation.

The realization that interest rates would likely stay higher for longer resulted in sharp increases in yields, especially for shorter terms. In Canada, the yield curve became significantly more inverted as 2-year Canada bond yields jumped 56 basis points, while 30-year yields climbed a smaller 21 basis points. Mid term issues also saw higher yields, with 5-year and 10-year yields rising 46 and 34 basis points, respectively. In the United States, 2-year Treasury yields jumped a similar 55 basis points, but longer term yields gained only 10 to 18 basis points.

The sharp rise in yields resulted in the federal sector returning -1.77% in the month. The smaller declines in longer term yields meant the provincial sector fared only slightly worse than Canada bonds, returning -1.84%. Investment grade corporate bonds earned -1.34%, benefitting from their higher yields and a small narrowing of their yield spreads. Non-investment grade issues returned -0.21% as high yield investors shrugged off concerns about rates staying higher for longer. The higher than expected inflation data increased interest in Real Return Bonds, helping them substantially outperform nominal bonds of equivalent duration as they earned -1.06%. Preferred shares declined 3.57% in the month, as higher bond yields and continued retail selling of preferreds weighed on the asset class.

Bond indices are expected to experience significant changes in duration during June as a result of coupon payments and numerous outstanding bond issues being dropped from various indices because their remaining terms to maturity have become too short. The duration of the FTSE Canada Universe, for example, is expected to increase by roughly 0.15 years, while the duration of the long term bond index will jump by over a half year. Most of the changes will occur on June 1st and 2nd, with more happening on June 15th. Index funds typically respond to the duration changes such as these by buying bonds to add duration around 4 pm of the day the change takes place. Investment dealers and active managers are able to take advantage of the mechanistic approach of index funds by positioning in advance of the indexers’ purchases. That positioning was responsible for a small rebound in the market in the final week of May.

We anticipate the annual rate of inflation will fall substantially in the next month as the outsized increase of 1.4% in May 2022 is dropped from the calculation. Indeed, the annual rate may fall below 3.5%, but the fight against inflation is not nearly over. With consumer prices up more than 2% in the first four months of 2023, inflationary pressures are clearly still too high. And with high profile wage settlements such as the recent ones for federal civil servants (12.6% over four years plus a $2,500 one time payment) and WestJet pilots (24% over four years), the risk is that a wage-price spiral is adding to the existing demand-pull inflation. The Bank of Canada appears to recognize this as its officials have started musing about whether they have made monetary policy restrictive enough. The Bank’s next rate setting meeting is June 7th, and some observers are now forecasting a rate increase at that time. While we acknowledge the possibility of a rate increase on June 7th, we think more likely that the Bank will wait until July 12th to decide if further rate increases are warranted.

Paradoxically, the good economic news in May makes us more concerned about a recession beginning later this year or early in 2024. The resilience of the Canadian and U.S. economies to date following substantial interest rate increases suggest even tighter monetary policy will be required to bring inflation sustainably down to the 2% target. That raises the likelihood of the economies reaching breaking points with sudden sharp retrenchments, rather than achieving so-called “soft landings”. The experience of the 1980’s, when inflation had become entrenched as it is currently becoming, suggests that inflation can only be curbed with a significant economic contraction that results from a substantial reduction in aggregate demand. Should a recession occur, we would expect federal bond yields to fall in anticipation of eventual rate cuts by the Bank of Canada and corporate yield spreads to widen sharply in reaction to the heightened risk.

Strategically, the portfolio durations were increased in anticipation of the index duration extensions causing a brief rally as index funds make their required purchases. We plan in the near term to reduce portfolio durations again, because of the potential for further rate increases by the Bank of Canada. Only when a recession appears imminent do we expect to extend durations. At that time, we will probably also shift more of the portfolios to mid term issues to take advantage of the yield curve inversion disappearing and the curve steepening. We began reducing the exposure to the corporate sector some time ago, and we plan to continue that process in the coming months.

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.