Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

Jeff Herold

June 12, 2018

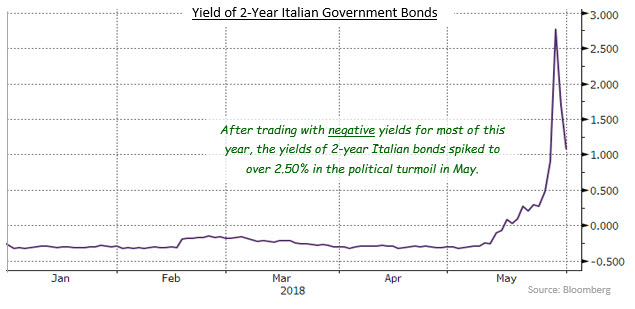

Political developments in Europe caused a sharp flight-to-quality bid in global bonds in late May. Yields of most developed economy bond markets fell as investors worried about a possible Euro Crisis, version 2.0. In Italy, three months after a national election, two Euro-sceptic populist parties’ efforts to form a government resulted in the Italian president vetoing their initial cabinet proposal, which could have resulted in another election. Many observers worried that if another election was to be held, it would give the populist parties even more support for their anti European Union policies. The yields on Italian bonds surged higher as a result. Yields subsequently fell part way back as negotiations continued, but the likely result will be ongoing uncertainty because Italy’s economy and national debt are much larger than that of Greece which caused Euro Crisis 1.0 in 2011. In Spain, stability was also at risk as a corruption scandal threatened to topple the government. The impact on Spanish bond yields was less dramatic than in Italy but did contribute to the global flight to quality.

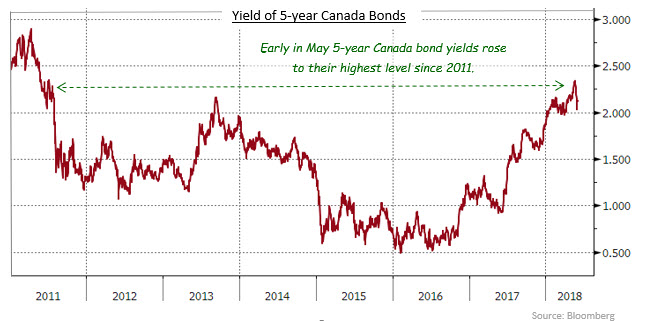

The yield curve flattened in May as shorter term Canada bond yields were little changed in the month, but 10-year yields finished 7 basis points lower and 30-year yields fell 14 basis points. The shift in yields during May was noteworthy for a couple of reasons. As noted above, yields had hit multi-year highs early in the month before falling back. In coming quarters and years, we expect bond yields will continue to move back to more normal historical levels as the various central banks’ quantitative easing programmes unwind. Also noteworthy in May was the compression in the yield spread between 10 and 30-year bonds. The difference in yields

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.