Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

Jeff Herold

April 5, 2024

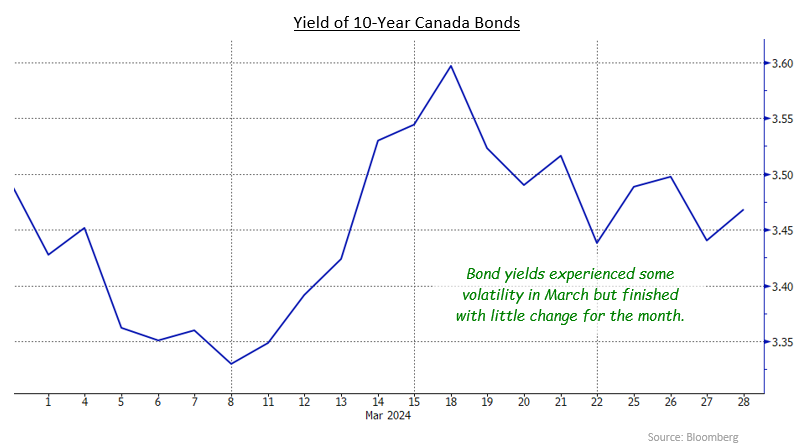

The Canadian bond market moved in a seesaw pattern in March, with yields initially falling, then rising before falling again. In the end, yields were only marginally lower on the month, with interest income generating most of the returns. Canadian inflation again surprised to the downside, but better than expected economic growth suggested the Bank of Canada would not need to rush interest rate cuts. The Bloomberg Canada Aggregate and FTSE Canada Universe indices returned 0.55% and 0.49%, respectively, in March.

For the second consecutive month, inflation in Canada was lower than expected. Prices rose only 0.3% in February compared with forecasts of 0.6% increases. As a result, the annual rate of inflation declined to 2.8% from 2.9%. The news caused bond yields to drop that day but had limited impact over the balance of the month. The lack of lasting impact may have been due to better than expected performance in the Canadian economy, which reduced the need for monetary easing by the Bank of Canada. Growth in Canadian GDP during January was reported at 0.6% and the initial estimate for February was an additional 0.4% improvement. Those increases implied growth in the first quarter at annual rate of 3.5%, much better than the Bank of Canada’s 0.5% forecast. Housing starts were stronger than expected at 253,000 units, although still inadequate for the rise in Canada’s population. The rapid increase in population accounted for the unemployment rate edging up to 5.8% despite job creation that was twice as strong as forecasts. The Bank of Canada met early in the month and left its interest rates unchanged, as expected. It indicated that it wanted to see further progress on inflation before considering rate cuts and also stated that it would continue to reduce its holdings of Canada bonds until at least early 2025.

Economic data in the United States was mixed during March but generally indicated that the U.S. economy remained resilient. On the positive side, the pace of GDP growth in the fourth quarter of last year was revised higher, and the index of Leading Economic Indicators rose for the first time in two years. The housing sector news was favourable, with both starts of new homes and sales of existing ones exceeding expectations. And, as this is being written, the manufacturing sector appears to be rebounding. On the negative side, the unemployment rate rose to 3.9% from 3.7% last month and retail sales were weaker than expected. Inflation edged up to 3.2% from 3.1% the previous month, although core inflation declined to 3.8% from 3.9%. The Federal Reserve left its interest rates unchanged and kept its forecast of three rate cuts this year. The market, though, pushed back the expected start date of the first reduction to July from this Spring.

Internationally, the most consequential development was the Bank of Japan’s first rate increase in 17 years as it decided to end its negative interest rate and Yield Curve Control (YCC) policies. The Bank had kept its overnight interest rate at -0.10% for the last eight years but going forward will allow the rate to move slightly above zero, as Japanese inflation has accelerated. YCC had most recently capped 10-year Japanese Government Bond yields at 1.00%, which encouraged Japanese investors to look at higher yielding global bonds including U.S. Treasuries and Canada bonds. Its removal will likely mean less Japanese interest in global bonds, which should result in upward pressure on their yields. In other international news, the Swiss National Bank became the first major central bank to cut rates in this cycle, as it surprised markets with a 25 basis point reduction in its target rate to 1.50%. All other major central banks left their rates unchanged in March.

The Canadian yield curve moved marginally lower in March as the yields of 2-year and 30-year Canada bonds finished one basis point lower. Mid term issues fared slightly better with 5-year and 10-year yields declining 6 and 4 basis points, respectively. The U.S. yield curve underwent similar changes in the month, with yields of mid term issues experiencing the largest declines.

The federal sector earned 0.51% in March, reflecting slightly lower yields as well as interest income. The provincial sector returned 0.43%, as slightly wider yield spreads negatively impacted its results. The widening of provincial yield spreads reflected investor disappointment as most provinces disclosed wider than expected budget deficit targets. The investment grade corporate sector gained 0.54%, with its yield spreads edging marginally wider. Non-investment grade corporates returned 1.22% in the month. Real Return Bonds ignored the lower than expected inflation data and earned 1.47% in March. Preferred shares gained 3.47% as announced redemptions by banks prompted investors to buy in anticipation of further redemptions.

As the third anniversary of inflation breaking out of Canada’s 1% to 3% target band approaches, we note that investors are having to again revise their expectations for the timing of the first rate cut by the Bank of Canada and the Fed. Inflation remains sticky and we think more and more Canadians are adapting to both the current levels of interest rates and inflation. We believe Canada’s inflation rate may accelerate above 3.0% in the coming months as the recent 10% rise in oil prices, ongoing housing rent increases, and various tax increases, including the April 1st federal carbon tax increase and the 9.5% increase in Toronto property taxes, are accounted for. If this happens, the Bank may not cut interest rates before autumn, which will put upward pressure on bond yields until then. We also believe the Bank will be cautious about lowering interest rates because it will want to avoid creating another housing frenzy. In the United States, we think the strength of the U.S. economy and the need to further slow inflation there will also mean fewer than expected rate cuts in that country this year.

We continue to be sceptical about how much monetary easing is built into Canada’s negatively sloped yield curve. For several years, the Bank has been estimating the “neutral” rate, which is neither stimulative nor restrictive, to be between 2.00% and 3.00%. More recently, though, the Bank has indicated that the neutral rate has probably increased. Our view is that the Canadian economy can sustain significantly higher interest rates than prevailed in the 2009 to 2022 period. And if money market yields do not fall below 3.00%, we do not see a lot of value in long term bonds currently yielding roughly 3.50%.

Both equity markets and the corporate bond market are reflecting more optimism about economic growth than we believe is warranted. Stock market indices have recently hit all-time records, while corporate yield spreads have narrowed to below average levels suggesting a low level of credit risk. A significant factor behind the optimism is expectations of rate cuts by the Bank of Canada and the Fed. Given our view that inflation is not yet vanquished and that rate cuts will not occur as soon as expected, we are cautious that equity markets may correct and corporate bond spreads may widen. Accordingly, we are somewhat defensive regarding the allocation to the corporate sector.

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.