Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

Jeff Herold

April 15, 2020

In contrast with as little as a month ago, most countries including Canada have embraced social distancing and self-isolation as the most likely way to slow the spread of the disease and avoid overburdening the available medical resources. To date, this strategy has not yet been proven successful in most countries, however, it seems likely to continue for at least two or three months. Assuming the social distancing strategy is effective, it will need to remain in place in some form in order to avoid an acceleration in the disease’s spread. As a result, we believe the shutdowns of many businesses will be extended to longer than the three to four months currently assumed in by the federal and provincial governments in their policy responses to the recession.

Bond issuance by the federal government has already ramped up to start covering the costs of the various new support programmes. The Bank of Canada’s new QE will offset much of that new supply. With most terms of Canada bonds yielding close to the Bank’s overnight target of 0.25%, we do not anticipate yields moving significantly lower, so we are keeping portfolio durations close to benchmark levels.

Provincial government issuance also needs to increase substantially but may require wider yield spreads in order to entice investors. To date, the Bank of Canada has only stepped in to improve liquidity in the provincial treasury bill market, but it may decide to purchase provincial bonds as well. Until that happens, we are content to remain underweighted to the provincial sector.

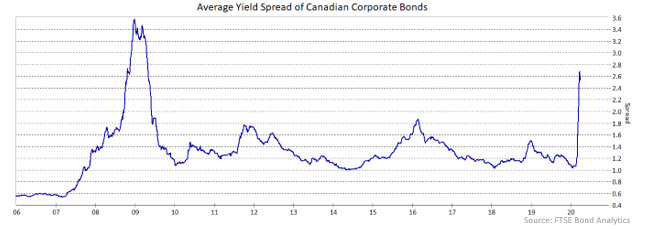

Corporate yield spreads widened very sharply in March, although a brief improvement in investor sentiment caused them to narrow somewhat in the last few days of the month. Rather than adding to corporate holdings at what appear to be historically attractive spread levels, we prefer to remain cautious regarding the sector. Canada, and the world, has just begun a serious recession and the implications for corporate borrowers continues to evolve rapidly. Until we have a better understanding of how effective the social distancing response is and how long the measures will be in place, it is very difficult to estimate their impact on corporate creditworthiness. We believe that once issuers begin reporting losses due to the crisis, yield spreads may widen further. For the time being, we are looking for opportunities to further upgrade credit quality and potentially reduce the corporate sector allocation.

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.