Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

Jeff Herold

April 15, 2020

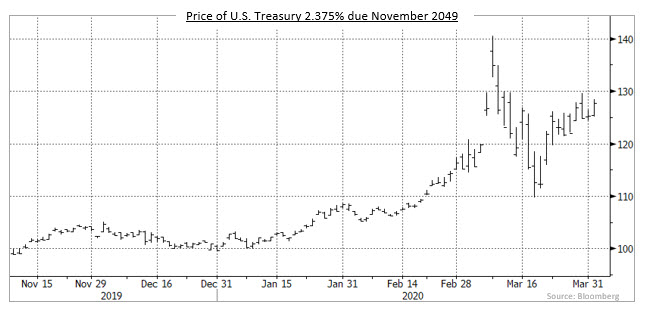

Bond markets were not immune from extraordinary volatility in March. Intra-day swings in prices of government bonds hit unprecedented levels in the month as liquidity deteriorated even in the biggest markets. An example of the volatility is shown in the chart below, which graphs the price of a U.S. Treasury bond maturing in November 2049. The vertical lines show the price range that the bond traded in each day (the longer the line, the greater the price range). Prior to March, prices rarely moved more than one percent in a day. In the chaotic trading during March, bond prices often changed by 8% to 10% in a single day.

The Canadian yield curve steepened significantly in March as the Bank of Canada’s three rate cuts prompted a sharp drop in shorter term bond yields. The yield of 2-year Canada bonds fell 72 basis points in the month, while 5 and 10-year yields declined 47 and 42 basis points, respectively. Surprisingly, though, the yield of 30-year Canada bonds finished the month 1 basis point higher. The lack of movement in long term yields was due to the combination of illiquidity and concerns regarding looming provincial supply. The changes in Canadian yields during March were fairly close to the moves in U.S. bond yields, with the exception of long term bonds. In the United States, 30-year Treasury yields fell 32 basis points in the month.

Federal bonds earned +1.63% in March as lower yields, particularly for shorter term issues, resulted in price gains. The provincial sector returned -2.83% in the month as the risk premium, or yield spread, increased by an average of 41 basis points. The increase in provincial yield spreads reflected the expected deterioration in provincial fiscal situations as tax revenues fall and social support spending is being dramatically increased to offset the economic slowdown and surge in unemployment. In the latter half of March, provinces struggled to attract interest in new public bond issues and started doing private ones. Of note, both Alberta and Manitoba issued 100-year bonds on a private basis. Investment grade corporate bonds fared worse than provincial issues, returning -5.41%, as their yield spreads widened an average 133 basis points in the period. There was wide variation in the spread performance of individual issuers, with some lower quality ones seeing much greater widening. Remarkably, there were $10.95 billion of new issues in the month, with five deals of $1 billion or more. New issue pricing concessions were significant, but some new issues later in the month quickly tightened their spreads by the amount of the concession. High yield bonds returned -10.43% in March, underperforming higher quality issues as the economy fell into recession. Ratings downgrades sharply increased the size of the previously tiny Canadian high yield sector, with Ford Credit Canada alone adding $8.3 billion to the sector following its rating reduction. Real Return Bonds returned -4.93%, as the double plunges in oil prices and economic demand were likely to constrain future inflation. Preferred shares fared poorly in the risk-off environment of March, declining -20.14%. The decline appeared to reflect investors’ concerns about creditworthiness more than the decline in bond yields.

Over the last five weeks, the global economy has crashed into a serious recession. In Canada, this will probably be much more severe than the 2008-09 financial crisis and at least as bad as the 1982 downturn. Unemployment has likely already doubled, given the early applications for unemployment benefits, and entire swathes of the economy have shut down, at least temporarily. Anticipating how long the recession lasts and how the market will react is especially difficult given the uncertainty of the COVID-19 pandemic.

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.