Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

Jeff Herold

July 8, 2021

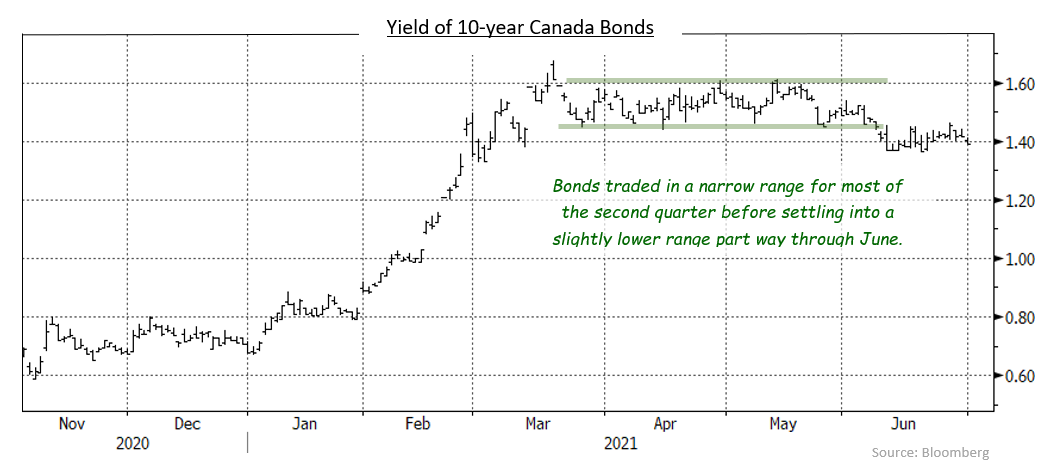

North American bond yields broke below the trading range that was established backed in March. Despite U.S. and Canadian inflationary measures reaching new recent highs, and both economies seeing continued reopening as vaccinations spread through their populations, investors seemed to be comfortable believing the views of North American central banks that inflationary pressures above 2% would be temporary. The FTSE Canada Universe Bond index returned 0.96% in the month of June.

Canadian economic data was mixed in June as employment, retail sales and manufacturing sales were all lower than expected due to the continued lockdown restrictions. In the most recent month, GDP declined -0.3% but second quarter GDP will likely rebound to grow +2.5%. Inflation continued to rise as the annual inflation rate in Canada increased 3.6% up from 3.4% in May and core inflation rose to 1.8% from 1.7%. Headline inflation is now at a 10-year high.

The Bank left its administered overnight rate unchanged at 0.25% at its June meeting. This was fully expected by the marketplace. The Bank stated that the economy remains on track with its projections and while it did express concern of slack in the economy, it is well believed by investors that the Bank will further taper their quantitative easing (QE) program again in July. The Bank of Canada dismissed increases in the inflation rate due to the rolling off of distorted low prices caused by the sudden onset of the Covid-19 pandemic a year ago. The Bank’s perspective was that this “base” effect, which has been raising headline inflation numbers, should begin to fade over the remainder of the year. The risk, however, is that supply line disruptions and powerful consumer demand could continue to pressure inflation upwards. That could force the central banks to reduce its substantial monetary stimulus sooner than expected.

U.S. economic data was mixed as well. Employment numbers came in lower than expected but higher than the previous month, which were dramatically lower than expected. Similar to Canada, U.S. annual inflation increased during the period with headline inflation up 5.0% from 4.2% in May and core inflation rose to 3.8% from 3.0%. Headline inflation in the U.S. also hit a 10-year high and core inflation was at a level not seen since 1992.

The U.S. Federal Reserve left its benchmark interest rate unchanged at 0.25% at its June meeting. This was anticipated by the market. However, the Fed’s projections of future rate increases became more hawkish, with more members of the committee forecasting that the first U.S. rate hike would take place in the second half of 2022. This caused 10-year bond yields to spike higher for a day, then subside to the low end of the trading range, generating some volatility in the bond market in the month.

In June, the FTSE Canada Universe Bond index saw sizeable monthly coupon payments and short-term bonds roll out of the index, which resulted in an increase in its duration. The increase in the index’s duration incented investors to buy bonds and the decline in bond yields during the period was greatest in longer-term maturities. Yields of 2-year Canada bonds, increased by 13 basis points in sympathy with US 2-year Treasuries, while 30-year bond yields declined 19 basis points. This resulted in the yield curve flattening 32 basis points. The flattening of the Canadian yield curve was similar to what occurred in the U.S. Treasury market, although in the US market, 2-year bond yields rose slightly less than Canada bonds.

In the Canadian bond market, federal bonds returned 0.53% in June as yields declined. Provincial bonds returned 1.48% in the month. The high quality and longer duration of provincial bonds were attractive to investors looking to extend durations with the index, which caused prices to rally and led to a 5 basis point narrowing of average yield spreads versus benchmark Canada bonds. Investment grade corporate bonds returned 0.78%. Short and mid-term yield spreads remained steady while longer-term corporate spreads narrowed as investors sought yield and term in longer corporate maturities. The strongest performing corporate sector on the month and quarter was infrastructure, which suggests that investors believe that a reopening of the economy is coming and corporate credits such as airports will likely benefit. Non-investment grade bonds returned 0.89%, as they followed stronger equity markets higher. Real Return Bonds earned 1.66% which was less than similar duration nominal bonds. Notwithstanding the rise in inflation, demand for RRB’s declined as investors were reassured by the Bank of Canada’s stance. Preferred shares contracted -0.22% in June as the market paused from the strong performance that they have experienced year-to-date.

The bond market has been trading in a range since March, but in June bond yields broke through the low end of that range and are now holding at lower yield levels. It is our belief price inflation will continue to build with economic and social normalization. In this environment the bond market is likely to push yields higher to compensate for the decay of income streams from inflationary pressures. In addition, the tapering of QE and ongoing issuance of government bonds should provide significant upward pressure on yields from reduced demand and increased supply. As a result, we are maintaining a defensive stance in portfolio durations with positioning that is shorter than underlying benchmarks.

We expect to see the Bank continue to reduce its QE bond purchasing program, with its next reduction likely coming in July. In addition, the Bank and the Fed are expected to raise interest rates beginning in the second half of 2022. Since the beginning of the spread of the Covid virus, the central banks’ extreme accommodative monetary policy that led to a steepening of the yield curve. Now that economies are poised to begin reopening, yield curves will begin to flatten as the central banks “take their foot off the gas” to normalize monetary policy. This normalization will push the short-mid part of the yield curve higher relative to longer-term yields.

Looking ahead to the third quarter we expect that, as vaccinations increase across the population, lockdowns will recede and the economy will continue to reopen. Considerable base and pent-up demand will likely spur robust growth over the remainder of 2021 and 2022. This strong demand growth will provide firm support for the corporate credit market. While the corporate credit backdrop looks attractive and we are comfortable positioning in the sector, we are mindful of the current expensive valuations of corporate bonds versus historical levels, and we are being very selective in adding to corporate holdings.

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.