Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

Jeff Herold

July 9, 2019

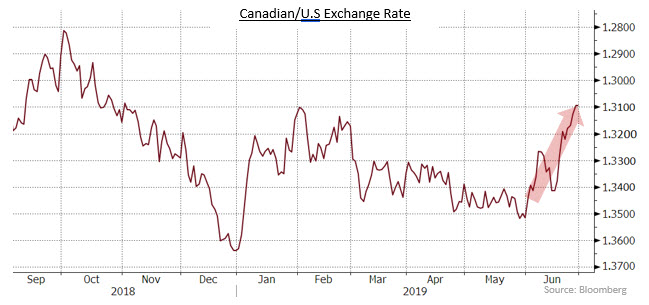

The prospect of imminent rate cuts by the Fed caused the U.S. dollar to lose value against almost all global currencies in June. The Canadian dollar was one of the largest beneficiaries, because the Bank of Canada was not expected to lower its rates either as soon or as much as the Fed. The loonie gained 3.2% versus the greenback, with the Canadian unit rising to its highest level of 2019.

Federal bonds returned 0.34% in June as lower long term yields resulted in higher bond prices. The provincial sector benefitted from its longer average duration and tighter yield spreads, earning 1.35%. Provincial yield spreads tightened by 3 basis points on average in the month. Investment grade corporate bonds earned 1.06% in the month. New issue supply was fairly robust with $14.3 billion of fixed rate, investment grade issues coming to market. In addition, there were $1.9 billion of new floating rate issues. The supply of new corporates bonds was, however, insufficient to meet investor demand and yield spreads narrowed 7 basis points on average, with the greatest tightening occurring in long term issues. Clearly, investors were confident that central banks, including the Bank of Canada, would ease monetary policy sufficiently to reduce the possibility of a serious economic slowdown. High yield bonds gained 0.70% in the period, slightly outperforming investment grade issues on a duration-equivalent basis. Real Return Bonds earned 1.38% in the month, essentially keeping pace with long term, nominal Canada bonds that have similar durations. Preferred shares gained 0.80% in the month, helped by slightly higher 5-year Canada bond yields and reduced expectations of Bank of Canada monetary easing.<!–nextpage–>

The Bank of Canada is scheduled to hold its next rate setting announcement on July 10th. We don’t expect the Bank will change its administered rates because the Canadian economy is performing better than the Bank’s expectations. The Bank had predicted the economy would bounce back from the tepid pace of last year’s fourth quarter and the first quarter of this year, but the Bank’s most recent forecast of 1.3% growth in the second quarter pales in comparison with the 2.5% consensus of private forecasters. Should the Fed decide to lower its interest rates at the end of July, the Bank will not necessarily follow suit because it had not raised rates as much as its American counterpart, and because the Canadian economy has been growing faster than expected.

Barring a surprise breakthrough in the China/U.S. trade dispute, the key event for bond investors during July will probably be the July 30-31 meeting of the Fed, at which it is widely expected to reduce its interest rates. Precedents for the Fed cutting rates to extend economic expansions include 1995 and 1998 when both times it lowered rates by a total of 75 basis points to encourage faster economic growth. Of note, in 1998, the Fed’s first rate reduction was 50 basis points, which has led to speculation that a similar move might occur this year. However, since the Fed’s June meeting a number of its officials have played down the possibility of 50 basis point reduction. Indeed, even a 25 basis point reduction is not a certainty, for three reasons. First, the Fed is still evaluating whether the U.S. economy is, in fact, slowing. There will be nearly four weeks of additional data before the meeting, including another report on unemployment and job creation that will confirm whether May’s weakness was a one-off event or the start of a slowing trend. In addition, the data will need to be analyzed to determine whether the economy is only slowing to its long term potential growth rate of roughly 1.9% or to something worse. Second, the Fed may not want to validate the U.S. administration’s trade policies. Much of the more pessimistic outlook for global and U.S. growth is the result of the tit-for-tat tariff wars that the Trump administration has initiated. If the Fed cuts rates to offset the slower resultant growth, that may encourage even more aggressive trade moves by the administration that will require further monetary easing. Third, the Fed may also not want to be seen validating the bond market’s anticipation of lower rates. While bond yields have fallen sharply in recent quarters, that is not a sufficient reason for the Fed to lower short term rates. The central bank values its independence and does not want to appear forced to follow the direction of the markets.

We are cautiously defensive regarding bonds. The current level of yields is discounting substantial worsening of the economy and resultant monetary easing by the Bank of Canada, neither of which is the most likely outcome, in our opinion. We believe the Canadian economy will continue to grow at a satisfactory pace and the Bank of Canada will stand pat on rates through the summer. In the fall, a federal election campaign will reduce the likelihood of the Bank making any move. The lack of rate cuts will put upward pressure on Canadian bond yields. Accordingly, we are maintaining portfolio durations somewhat below benchmark levels. Should there be positive developments on the trade front, we will look to shorten durations further. The yield curve is inverted from Treasury Bills to 10-year bonds, making mid term issues the most expensive on the yield curve. Accordingly, we are shifting the portfolio away from the mid term sector and into a combination of short and long term issues. Our sector allocation strategy is maintaining a moderate overweight of the corporate sector, but we are looking to further improve overall credit quality given the current stage of the economic cycle.

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.