Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

August 3, 2018

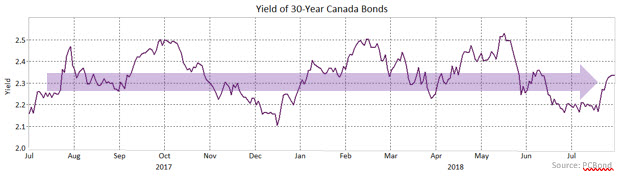

However, as can be seen in the chart below, the yield of 30-year bonds has not increased significantly during that period. As a consequence, the differential between 2 and 30-year yields has shrunk to only 25 basis points (i.e. the yield curve has flattened). While long term yields usually do not follow administered rates as closely as short term bond yields, the lack of any significant upward trend in long term yields in the last year has been a little surprising. Demand for traditional long duration assets by pension funds and life insurance companies combined with constrained supply of new long-duration bonds has left 30-year yields little changed. In the United States, a similar pattern has occurred. There, tax reform is encouraging corporations to contribute to underfunded pension plans before the corporate tax rate drops in mid-September. After September, there should be fewer pension contributions to be invested in bonds at the same time that the growing federal deficit necessitates increased bond supply.

We believe that the current demand/supply imbalance of long duration bonds will correct in the next few months and long term yields will rise. In anticipation of that occurring, we are keeping the duration of the portfolio shorter than that of the benchmark. As well, we have structured the portfolio to benefit from increasing term differentials (i.e. a steepening of the yield curve).

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.