Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

August 3, 2018

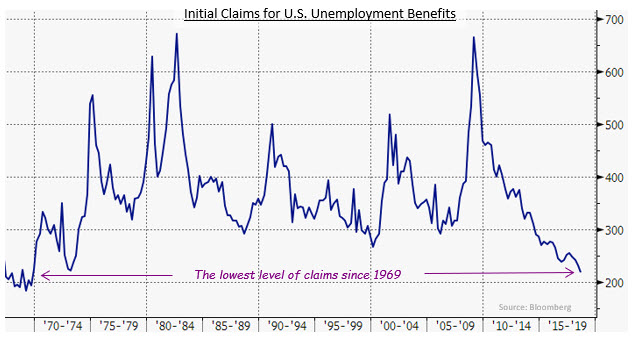

U.S. economic releases in July continued to show the economy operating at full speed. Growth in U.S. GDP during the second quarter was estimated at a robust 4.1% pace. Factory orders and light vehicle sales were stronger than expected and consumer credit was higher due to a surge in credit card spending. The estimated savings rate was revised substantially higher for 2016 and 2017, averaging 6.7% versus the previously reported 4.2%, suggesting greater potential for consumers to spend. However, most of the upward revision reflected small business owners making more money rather than employees earning higher wages. Similar to the Canadian data, the U.S. unemployment rate rose to 4.0% from 3.8% because of higher participation. The labour market in the U.S. remained very tight; initial claims for state unemployment benefits fell to the lowest level in 49 years, notwithstanding the 60% growth in the U.S. population since 1969.

The Canadian yield curve shifted upward in July in a nearly perfect parallel fashion, with 2-year bond yields rising by 12 basis points and 30-year yields by 13 basis points. The changes in Canadian yields were quite similar to the ones that occurred in the U.S. bond market during the month. The federal sector returned -0.63% in the period, as higher yields meant lower bond prices. Provincial bonds returned -1.04% on average; a 2-basis point narrowing of yield spreads was not enough to offset the longer average duration of the sector. Investment grade corporate bonds earned -0.49%. Corporate yield spreads tightened by 2 basis points, as new issue supply of $5.1 billion was insufficient to satisfy demand in the normally quiet summer month. Non-investment grade corporate bonds earned +0.27%, as they benefitted from higher coupon income and lower durations. Real Return Bonds returned -1.86% and only slightly outperformed nominal bonds on a duration-adjusted basis. Preferred shares fared better than bonds gaining +1.13% in July.

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.