Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

Jeff Herold

February 7, 2024

Bond prices declined and yields rose somewhat in January as investor optimism faded regarding central bank interest rate cuts occurring in the near future. Evidence of economic resilience, combined with increases in inflation and central banks reinforcing the need for sustainably lower inflation, caused yields to reverse a portion of their massive declines in November and December. The broad Bloomberg Canada Aggregate and FTSE Canada Universe indices returned -1.48% and -1.37%, respectively, in January.

In Canada, the economic data suggested the Bank of Canada would take longer to cut interest rates than the market had anticipated. The unemployment rate held steady at 5.8% despite job creation stalling, as the participation rate fell somewhat. Of concern to the Bank of Canada, though, wage pressures increased with average hourly wages rising by an eye-popping 5.7%. In addition, overall inflation accelerated with CPI rising to 3.4% from 3.1%, while core measures of inflation remained stubbornly above 3.5%.

The Bank of Canada announced on January 24th that it was leaving its overnight target interest rate unchanged at 5.00%. While Canadian economic growth had stalled, in the Bank’s opinion, the central bank wanted to see “further and sustained easing in core inflation”. The Bank’s projections expected inflation to remain around 3% in the first half of this year, then start gradually declining and finally return to the 2% target in 2025. Subsequent to the Bank’s announcement, StatsCan estimated Canadian real GDP topped expectations with a respectable 0.2% advance in November, and the flash estimate for December pointed to an even sturdier 0.3% rise. If the flash estimate is correct, growth in the fourth quarter would have been at an annual pace of 1.2%. While not robust, that pace is considerably better than the lack of growth experienced in the middle quarters of 2023 and substantially better than the Bank of Canada’s projections. Better than expected growth, of course, reduces the pressure on the Bank of Canada to lower interest rates.

The Bank made no changes to its Quantitative Tightening (QT) programme, which is gradually reducing the Bank’s holdings of Government of Canada bonds accumulated during the pandemic. The Bank did, however, provide more details on how it will be buying Canada Mortgage Bonds (CMBs) for the federal government. This quarter, the Bank will be purchasing half of the each of the expected new 5-year and 10-year CMB issues. In subsequent quarters, the Bank will purchase half of the quarterly total issued without necessarily buying 50% of each issue. Even though CMB total issuance will increase this year to $60 billion from $40 billion, the Bank’s purchases mean that new CMB supply available to the public will decline from $40 billion to $30 billion per annum, which resulted in CMB yield spreads versus benchmark Canada bonds tightening.

In the United States, the economic data also reduced the immediate need for monetary easing. U.S. GDP was estimated to have grown by 3.3% in the fourth quarter of last year which followed the very robust 4.9% pace of the third quarter. The labour market remained tight with the unemployment rate remaining at the very low level of 3.7%, while job vacancies rose to historically high levels. In addition, the increase in average hourly earnings edged up to 4.1%, a level inconsistent with the Fed’s 2% inflation target. The strong labour market resulted in buoyant consumer confidence, which translated into better than expected retail spending. Only the manufacturing sector showed signs of weakening but even there the indicators were somewhat ambiguous. Also in January, the regional banking crisis of last March resurfaced as New York Community Bancorp cut its dividend in the wake of large losses on two loans it had taken over after Signature Bank failed last year. The same day, Japan’s Aozora Bank announced it also had large losses related to U.S. commercial real estate loans. The news resulted in a brief flight to safety bid for U.S. Treasuries and a widening of U.S. bank spreads.

The Fed left its interest rates unchanged at its January 31st meeting and Fed Chairman Powell said that while rate cuts were possible this year, they were unlikely to start at the Fed’s next meeting on March 22nd. Chairman Powell did note they would be considering changes to the Fed’s QT programme at the March meeting, which could result in less supply pressure in the U.S. Treasury market. The bond market appeared to focus on the QT news rather than the delay to anticipated rate cuts as it rallied following the Fed announcements.

Internationally, the case for interest rate reductions is somewhat stronger. In Europe, GDP did not show any growth in the fourth quarter. However, the European Central Bank left its interest rates unchanged as it also waited for more progress on inflation. In the U.K., economic growth had stalled in the second half of last year, but as this is being written, the Bank of England has chosen to leave its interest rates unchanged.

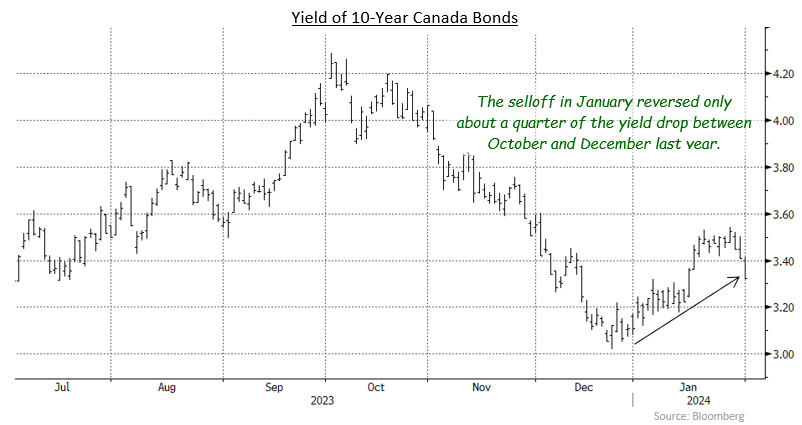

The Canadian yield curve experienced a rare parallel shift upward in January with yields of most maturities finishing 26 basis points higher than month earlier levels. The U.S. yield curve, in contrast, saw little change in shorter term yields while 30-year Treasury yields rose 20 basis points. As a result, the U.S. yield curve lost most of its inversion as the 30-year yield finished only 3 basis points below the 2-year Treasury yield. In contrast, the yield of 30-year Canada bonds finished 72 basis points below the yield of 2-year Canada bonds. The difference between the Canadian and U.S. curves reflects the concerns about financing the relatively large U.S. fiscal deficit and the focus of the Canadian government on issuing shorter term bonds.

Federal bonds returned -1.20% in January, as price declines were larger than the interest earned in the month. The provincial sector, which has a longer average duration, returned -2.05%. Provincial yield spreads were only marginally tighter in the month. Provincial governments were busy raising new financing, issuing almost $10 billion domestically and another $9 billion in non-Canadian dollar markets. Investment grade corporate bonds fared better than government bonds, returning -0.68%. Demand for corporate bonds was quite strong as their yield spreads narrowed an average 9 basis points in the month despite record new issues totalling $15.4 billion. (The previous record for January issuance was $12.9 billion in 2013.) Non-investment grade corporate bonds earned +0.88% in the month as investor optimism prompted buying of lower quality credits too. Real Return Bonds returned -2.95% due to their very long average durations. However, the rise in inflation helped RRBs perform markedly better than nominal issues with similarly long durations. Preferred shares, in contrast with bonds, enjoyed at strong start to the year, gaining 5.81% in January.

We are cautious about the bond market because we believe investors are too optimistic about inflation and because of the potential for fewer interest rate cuts by the Bank of Canada than many investors are anticipating.

Economic forecasting is quite difficult because the economy is so complex, but the nearly universal consensus that has developed around a slowing path for inflation reminds us of a 1960’s hit song that begins: “Wishin’ and hopin’ and thinkin’ and prayin’”. Just because people want inflation to decline, doesn’t mean it will happen. It is the very complexity of the economy that makes us less optimistic about inflation. Inflation has impacted virtually every segment of the economy, but each of those areas have different reaction functions. Some sectors, such as supply constrained goods in the pandemic, responded quickly while others, such as wage settlements, are still trying to catch up. And ongoing inflation leads to further inflation. Only a reduction in aggregate demand, as in a recession, has led to inflation being tamed in the past. If the consensus about inflation continuing to slow proves incorrect, the Bank of Canada and other central banks will need to keep interest rates higher for longer than the bond market currently anticipates.

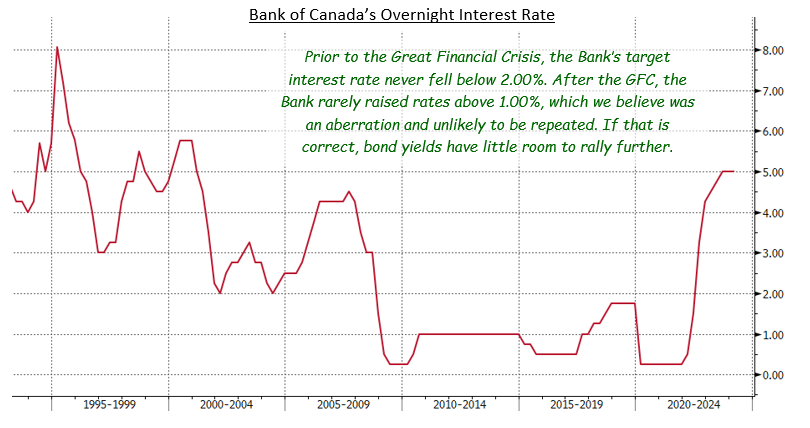

If and when the Bank of Canada begins lowering interest rates, a key consideration will be how low rates might go. For several years, the Bank has been estimating the “neutral” rate, which is neither stimulative nor restrictive, to be between 2.00% and 3.00%. More recently, though, the Bank has indicated that the neutral rate has probably increased. Given the recent bout with inflation, we believe the Bank will be reluctant to lower its target interest rate below 3.00%. We suspect that level differs from investors who started their careers in the last fifteen years, a period when the Bank of Canada kept its interest rate well below 2.00%. We believe that period was an aberration, rather than the new normal, and the Bank will be reluctant to return interest rates to such low levels, given the negative consequences that included a housing bubble. As can be observed in the following chart, prior to the Great Financial Crisis, the Bank’s overnight target rates never went below 2.00% and yet the Canadian economy performed reasonably well. Our view is that the Canadian economy can sustain significantly higher interest rates than prevailed in the 2009 to 2022 period. And if money market yields do not fall below 3.00%, we do not see a lot of value in long term bonds currently yielding less than 3.50%.

The ongoing tightening of corporate yield spreads keeps us cautious about the corporate sector. As we noted last month, investors appear “unduly optimistic given the tepid pace of economic growth and the potential for the Bank of Canada to keep monetary policy restrictive for several more months. We are particularly cautious regarding real estate issuers given their elevated leverage and the need to adjust cap rates to reflect current interest rates and bond yields. In addition, there is a concentration in equity market gains, particularly in the U.S. S&P500 where seven massive tech stocks are dominating the price performance of the other 493 index constituents. Any correction in equities will likely cause corporate yield spreads to widen noticeably.”

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.