Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

Jeff Herold

February 15, 2018

The federal sector returned -0.77% in January as higher yields pushed bond prices lower. The provincial sector declined -1.26% in the month. The longer average duration of provincial bonds, plus a small widening in their yield spreads, resulted in the sector’s weak performance. In contrast, the corporate sector declined only -0.24% in the period. Of note, BBB-rated issues had markedly better returns than higher rated issues. New issue supply for much of the month was insufficient to meet demand, which caused yield spreads to narrow by 7 basis points on average. There were $10.5 billion of new investment grade corporate issues in January, but only $6.15 billion were fixed rate bonds, with the balance in floating rate issues. Of the fixed rate new issues, $2.35 billion came to market on January 31st. Non-investment grade bonds returned +1.01% in January, with only one new issue of $200 million. Real Return Bonds earned -0.42% on average as they outperformed nominal bonds on a duration-neutral basis. Robust economic growth, combined with a lack of excess capacity, made investors nervous about increased inflationary risks. Preferred shares earned +1.58% in January.

We have taken defensive steps in clients’ bond portfolios because we believe yields are likely to move higher. The synchronized global economic expansion is using up spare capacity and causing most central banks to reduce the amount of monetary stimulus that they are providing. It appears likely that the Fed will raise its administered interest rates at its next meeting, which is scheduled for March 20 and 21. The Bank of Canada will probably follow suit at its April 18 meeting. Given the possible impact on the exchange rate, we believe that the Bank will avoid raising rates before or faster than the Fed this year.

The bond market is unlikely to wait for the central banks to raise their respective rates. Instead, investors will probably anticipate the Spring rate increases as well as additional increases later this year. There is also potential for an acceleration in the pace of inflation that would only increase the expected pace and magnitude of the rate increases. Accordingly, we have reduced portfolio durations further.<!–nextpage–>

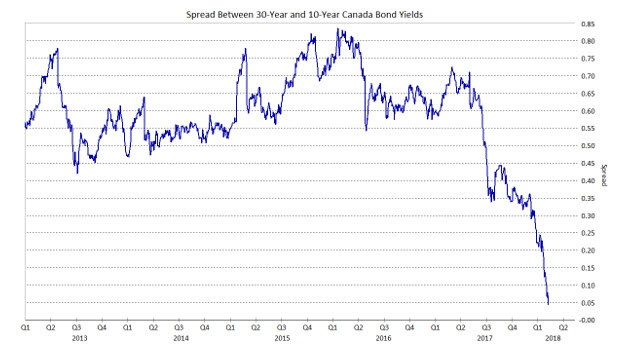

While rate increases by central banks have often led to flattening of the yield curves in the past, we have been a little surprised by how much the difference between 10 and 30-year bond yields has shrunk recently. In January alone, the spread between the two maturities shrank by 15 basis points to finish at only 5 basis points (0.05%). The outperformance of 30-year

issues on a yield basis was, in our opinion, unjustified and we think that it will reverse in coming weeks. Accordingly, we are reducing the long term holdings in favour of additional mid term issues.

The corporate allocation remains higher than the benchmark index in order to improve the overall portfolio yield and return. However, corporate yield spreads have narrowed in most cases to levels that are historically unattractive from a risk/reward perspective. As a result, we plan to gradually reduce the corporate holdings in the coming months. While that may reduce returns modestly in the near term, we believe it will prove to be the correct decision in the long term, as it has in the past. We are also maintaining the Real Return Bond allocation because RRB’s remain cheap versus nominal bonds and because inflationary risks have increased.

We have been asked a few times lately whether the recent flattening of the yield curve is a harbinger of a recession. We do not believe so, because the flattening has not been caused by aggressive tightening by central banks. Rather, long term yields have been remarkably sticky for technical reasons that may soon dissipate, allowing yields to rise and the curve to re-steepen somewhat. As well, if rising bond yields lead to a long-awaited correction in equity markets, the rise in bond yields may slow but probably not stop. Unless a serious bear market develops for stocks, we would not anticipate central banks to react.

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.