Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

Jeff Herold

February 15, 2018

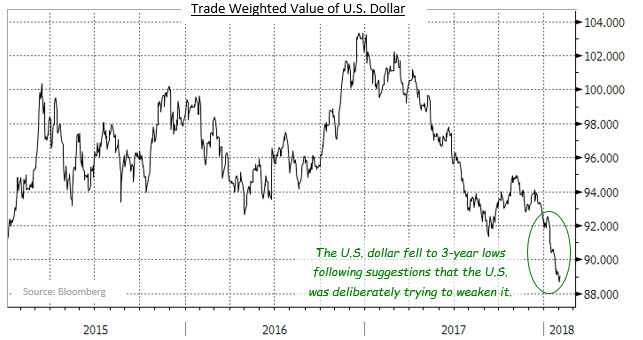

Eurozone economic data was also positive in January. GDP growth in the last quarter of 2017 was at an annual pace of +2.7% and unemployment held steady at 8.7%, which was the lowest rate in 9 years. While the European Central Bank did not change its policy, many observers expect that the ECB will terminate its quantitative easing programme in September. The end of QE will likely cause European government bond yields to gradually rise thereby lessening the downward pressure on other bond yields, including those of Canadian bonds. The improved European growth rate in the last year has also led to weakness in the U.S. dollar. Through 2016, the U.S. dollar had risen in value against most other global currencies, due to the far better performance of the U.S. economy. However, as European growth improved though 2017, it became apparent that a synchronized global recovery was underway, and the U.S. dollar gave back some of its earlier gains. This past month, the U.S. dollar decline accelerated following remarks by the U.S. Treasury Secretary, Steven Mnuchin, that the United States was pursuing a weak dollar strategy. A weaker dollar would make U.S. exporters more competitive and thus stimulate the U.S. economy. However, with the U.s economy already at full capacity, the need for further stimulus is questionable. Faster

economic growth has the potential to raise inflation, because there is no extra capacity to satisfy additional demand. As well, the weaker dollar will increase import prices, which would also increase U.S. inflation. Should U.S. inflation accelerate for its current pace of roughly 2.0%, the Fed would likely act to slow growth by raising rates more quickly.

Yields of all maturities in the Canadian bond market moved higher in January, with the largest increases occurring in mid term bonds. The yields of 2 and 30-year Canada Bonds, for example, rose 12 and 10 basis points, respectively, while 5 and 10-year yields jumped 22 and 25 basis points. The greater increase in mid term yields appeared to reflect investors’ revised expectations for further rate increases by the Bank of Canada. Longer term yields failed to keep pace with mid term yields apparently due to a technical shortage of long term bonds; investment dealers had become short the sector in December, and new issue supply in January was less than expected making it difficult to cover the short positions. As well, with the Bank of Canada in the midst of a monetary tightening cycle, investors anticipated that the yield curve would flatten, increasing the demand for long term bonds versus shorter term issues. The “bowing out” of the Canadian yield curve during January also resembled the shift in the U.S. yield curve in the month. The U.S. shift, though, was roughly 10 basis points larger at each term.

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.