Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

Jeff Herold

March 6, 2020

On the positive side, China has started to reboot its economy by gradually lifting the quarantines, encouraging businesses to re-open, and providing fiscal stimulus. In less than three months, the country that was the epicentre of the crisis appears to be recovering from the epidemic, although the rebound will likely take two or three months. If the epidemic truly has been contained in China, that provides reasons for the rest of the world to be optimistic that the impact will be relatively short-lived.

Global central banks have already started increasing monetary stimulus. In addition to the Fed, the central banks in Australia and Malaysia have lowered their rates, and the Bank of Canada is expected to reduce its rates on March 4th. Fiscal measures to offset the coronavirus related slowdown have also been promised by the G-7 group of major economies. We believe these moves will ameliorate, but not fully prevent the slowing of growth in the first half of the year. Should the epidemic be sufficiently contained, as we hope, we look for growth to rebound in the second half of the year.

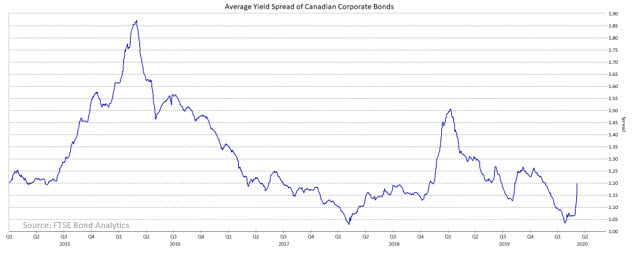

As can be seen in the chart below, the widening of corporate yield spreads during February did not make them cheap, just less expensive. Relative to the last five years, spreads remain fairly tight. If economic growth remains sub-par, we would expect spreads to move wider still. As a result, we are comfortable with the recent

reduction in the corporate allocation and, in particular, the lessening of BBB-rated issues. We are also maintaining our yield curve positioning in anticipation that central bank rate cuts will lead to a steepening of the curve with shorter term yields falling faster than long term ones.

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.