Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

Jeff Herold

March 6, 2020

The coronavirus epidemic remained the dominant factor in global financial markets during February. While the epidemic appeared to be contained in China, with fewer new cases and deaths being reported on a daily basis there, the escalating number of countries with confirmed cases of the disease led to market panic developing late in the month. Equity markets were especially hard hit with several experiencing corrections (i.e. declines of 10% or more). Government bond yields plunged, particularly in the United States, as investors sought safe havens from the expected impact of a sharp reduction in global growth brought on by the disease’s spread. Canadian bond yields fell, but in more muted fashion than American ones, and yield spreads on provincial and corporate bonds moved wider in the risk averse environment. The FTSE Canada Universe Bond index returned 0.71% in February.

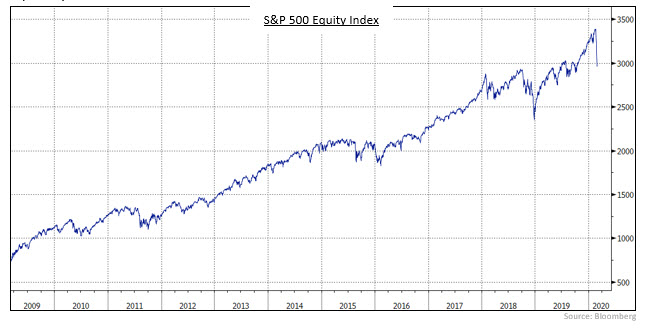

The plunge in equities caught the world’s attention, not only because it wiped out $3 trillion of wealth but also because it suggested a sharp deterioration in confidence that would depress future economic activity. However, to put the stock selloff in context, it only wiped out the gains enjoyed since last October. Relative to the upward move during the 11-year long bull market (as shown below), the correction does not look especially worrisome.

Economic data received in February had a smaller than normal impact on bonds because it reflected activity prior to the coronavirus outbreak. That said, negative economic news tended to reinforce the view that the Canadian economy was already underperforming its potential before the outbreak and the subsequent drop in commodity prices and slower global growth would make it more likely for the Bank of Canada to lower its interest rates going forward. On the positive side, unemployment dropped to 5.5% from 5.6% the previous month, housing starts were better than forecasts, exports rebounded from rail and pipeline disruptions last fall, and late in the month consumer confidence was reported to have hit a 7-month high. Among the negative news Canadian GDP in the fourth quarter last year slowed to annual pace of only 0.3%, although growth in December was surprisingly strong. As well, manufacturing and retail sales were reported to have been weaker than expected in December, primarily due to the auto sector. Inflation rose to 2.4% from 2.2% the previous month, but core inflation measures edged slightly lower.

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.