Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

Jeff Herold

January 13, 2020

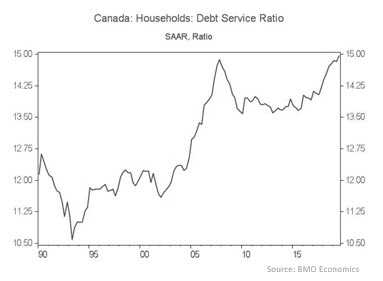

Canadian economic growth slowed in the second half of 2019 but some of the causes, such as strikes at CN Rail and GM, were temporary. Positive factors for continuing Canadian growth include robust population growth, a healthy housing market, increased investment spending with the greater trade certainty, and improved energy sector confidence as the Trans Mountain Pipeline expansion finally proceeds. In addition, we anticipate increased fiscal stimulus as the minority federal government raises spending in its March budget. Our biggest concern about the Canadian economy is the level of household debt, which has already

resulted in rising insolvencies even as interest rates have stayed low. Household debt service ratios recently hit record highs and could move even higher with any increase in interest rates. Having encouraged consumers to take on more debt when it lowered interest rates in 2015, the Bank of Canada is wary of repeating its mistake in 2020. That said, the Bank will be very cautious about raising rates given the difficulties some households are already experiencing with debt costs.

The yield curve is quite flat, with little difference between short and long term Canada bond yields. Mid term yields, though, remain slightly lower than short and long term levels and appear to be discounting the potential for interest rate reductions by the Bank of Canada. We believe that, barring an economic surprise, the Bank is unlikely to change rates for the next few quarters, so mid term issues look overvalued and we plan to reduce those terms in the portfolios. Overall, as economic growth remains satisfactory, the pessimism apparent in such low absolute long term yields should dissipate allowing the yields to rise. Accordingly, we are structuring the portfolio to benefit from a steepening of the yield curve.

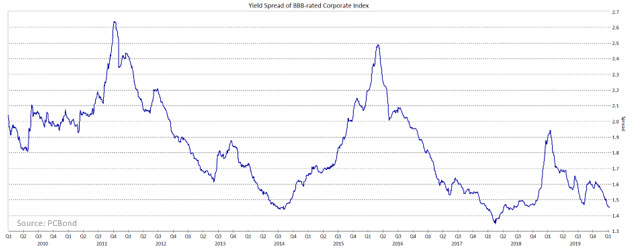

We do not anticipate a recession in the next year, so we are comfortable with an overweight allocation to corporate bonds. However, we recognize the potential for a slowdown has increased, so we are carefully reviewing the creditworthiness of every holding and looking for opportunities to lower overall risk. Corporate yield spreads have recovered from the sharp widening that occurred in the fourth quarter of 2018 and are now near the tightest levels of the ten years since the financial crisis. The weakest investment grade corporate bonds, those rated in the BBB category, look particularly expensive.

Consequently, we anticipate reducing further the already underweight allocation to BBB-rated issues in the coming weeks.

Please accept our best wishes for a healthy and happy 2020.

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.