Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

Jeff Herold

January 13, 2020

Globally, in addition to the tentative U.S./China trade deal, there was somewhat less economic gloom during December. In Australia, unemployment was lower than expected and, in New Zealand, third quarter growth of its GDP was stronger than forecasts. In Sweden, the Riksbank raised its key rate to zero after five years in negative territory, making it the first central bank to exit its negative rate strategy. Rates remain negative in the Eurozone, Japan, Switzerland, Denmark, and Hungary, but there is hope that more central banks will follow Sweden’s lead. In that vein, the new head of the European Central Bank, Christine Lagarde, has indicated that she is less enthusiastic about negative interest rates than her predecessor Mario Draghi. Instead, she has started advocating for increased fiscal stimulus, particularly from Germany. Negative yields in Europe and Japan over the last several years have pushed yields in other bond markets, including Canada’s, much lower than otherwise would have occurred as investors sought positive yields. An end to negative yields would presumably lead to less demand for Canadian bonds and higher yields would result.

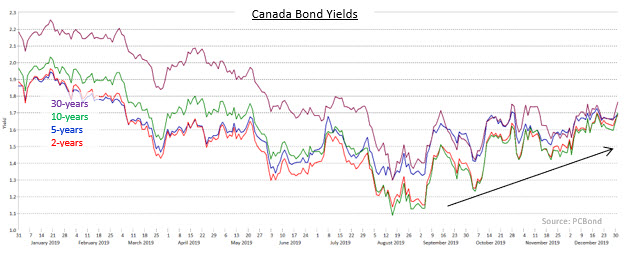

The Canadian yield curve steepened in December because the 21 basis point increase in 30-year Canada bond yields was greater than the 11 basis point rise in 2-year yields. Mid term bonds, which had been anticipating future interest rate reductions by the Bank of Canada, experienced higher yields in the more optimistic environment of December. Yields of 5 and 10-year Canada bonds rose 19 and 24 basis points, respectively. The increase in yields during the month extended the rising trend since the lows hit in August and brought each of them closer to the Bank of Canada’s overnight target of 1.75%. The U.S. bond market also experienced a steepening of its yield curve, although the changes in yields were smaller than in Canada. The yield of 2-year Treasuries declined 5 basis points, while 30-year Treasury yields rose 18 basis points.

Federal bonds returned -1.06% in December as coupon income failed to offset the lower prices brought on by higher yields. Provincial bonds returned -1.80%, as their longer average durations resulted in larger price declines as yields rose. The more positive economic sentiment of December led to robust demand for provincial issues that resulted in their yields narrowing to Canada benchmarks by 3 basis points. Investment grade corporate sector returned -0.54%, thereby outperforming government issues, as corporate yield spreads narrowed another 8 basis points in spite of $10.9 billion of new issues. Seasonally high coupon payments combined with relief regarding trade tensions to produce strong demand for corporate issues. High yield bonds gained +0.30% in December, helped by an absence of new issues. Real Return Bonds returned -1.53%, which was significantly better than nominal bonds on a duration-adjusted basis. Preferred shares enjoyed markedly higher returns than both bonds and equities, earning +2.48% in the month.

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.