Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

Jeff Herold

May 13, 2024

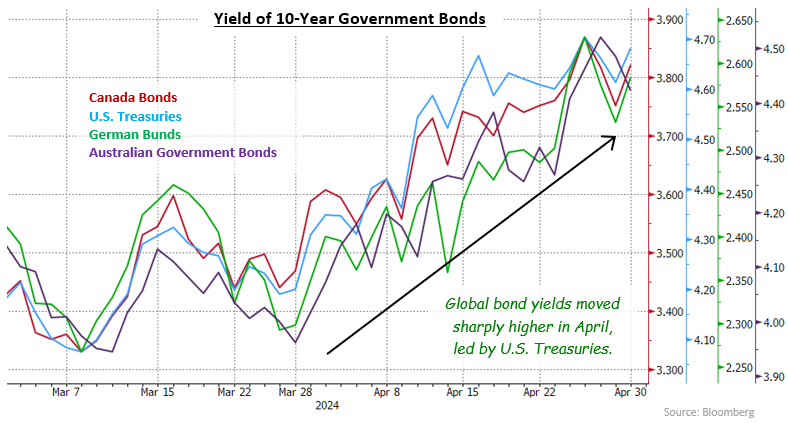

For the third month in four to start 2024, Canadian bond prices declined and yields moved higher in April. The shift to higher yields was part of a global trend led by U.S. Treasuries as investors substantially revised their expectations of when the Federal Reserve would begin lowering interest rates. Stronger than expected U.S. economic data and stubbornly high inflation in that country caused forecasts to shift from three interest rate cuts starting in July to perhaps one in December, or not at all this year. With money market yields expected to stay higher for longer, bond investors demanded higher yields too. Stock markets declined in reaction to the higher for longer rate expectations, but corporate bond investors were more optimistic as corporate yield spreads tightened again. The Bloomberg Canada Aggregate and FTSE Canada Universe indices returned -2.10% and -2.00%, respectively, in April.

In contrast with the U.S., Canadian economic data remained supportive of potential interest rate cuts as soon as June or July. The unemployment rate jumped to 6.1% from 5.8% as the number of jobs unexpectedly shrank while the labour force continued to grow rapidly due to surging immigration. Growth in GDP appeared to be decelerating from January’s robust pace, with slower than expected growth in February and StatsCan estimating no growth in March. Retail sales were also weaker than expected, suggesting high interest rates were discouraging consumption. Inflation was little changed as CPI rose to 2.9% from 2.8%, but core measures eased to slightly below 3.0%. The Bank of Canada left its interest rates unchanged at its April 10th meeting and indicated that it wanted more evidence that inflation was under control. The Bank also indicated that rate cuts are likely to be gradual when they finally begin.

In the United States, the economy continued to be resilient, and inflation failed to improve for the third consecutive month, which led investors to conclude that the Federal Reserve might keep interest rates unchanged for the balance of the year. Of particular importance during April, CPI accelerated to 3.5% from 3.2%. Reinforcing concerns about inflation, the Employment Cost Index gained 1.2% in the first quarter, up from 0.9% in the final quarter of last year. Indications of economic strength included the unemployment rate declining to 3.8% on robust job creation, and better than expected retail sales and manufacturing production. First quarter GDP growth was weaker than expected but excluding the volatile categories of net exports and inventories, the U.S. economy continued expanding at an above trend pace.

The prospect of the Fed keeping its interest rates high for an extended period distinguished it from other global banks that are thought to be considering rate reductions in the next few months. As a consequence, the U.S. dollar strengthened markedly versus other major currencies in April. The Canadian dollar was not immune to the speculation about the timing of Fed rate cuts, declining 1.7% versus the U.S. currency. That weakness pointed to potential trouble for the Bank of Canada should it decide to lower rates ahead of the Fed because a weaker exchange rate would result in higher inflation.

As this is being written, the U.S. Federal Reserve has kept its Fed Funds target range at 5.25% to 5.50% for the sixth consecutive meeting. Fed Chair Jerome Powell said progress on reducing inflation had stalled recently, but additional rate increases were unlikely. The only significant change announced was that the Fed would slow the pace at which it reduced its holdings of U.S. Treasuries. Starting in June, the Fed’s holdings will decline by $25 billion per month instead of the current $60 billion pace.

The potential for interest rates staying higher for longer, combined with the steep inversion of the Canadian yield curve, led longer term yields to have the larger increases in April. Yields of 2-year Canada bonds rose 28 basis points, while bonds maturing in 5 to 30 years saw yield increases of 34 to 37 basis points. As a result, longer term yields finished closer to shorter term ones and the Canadian yield curve became slightly less inverted. As noted above, U.S. Treasuries led the way to higher yields in April, with larger increases than in Canada. Yields of 2-year Treasuries rose 36 basis points, while 30-year yields climbed 44 basis points. Mid term yields experienced even larger gains with 5-year and 10-year Treasury yields jumping 51 and 48 basis points higher, respectively.

The federal sector returned -1.68% in April, as the higher yields resulted in declining bond prices. The provincial sector returned -2.91% as its longer average duration resulted in larger price declines with higher yields. In addition, provincial yield spreads widened one basis point in the month. The investment grade corporate sector returned -1.24% in April. The corporate sector’s duration was 1.4 years shorter than the overall Universe, which meant less impact from the rise in yields. In addition, corporate yield spreads narrowed 3 basis points during the month as investor demand for extra yield remained strong. During April, $8.7 billion of new corporate issues came to market, well ahead of the $5.8 billion in April 2023. So far in 2024, there have been $47.3 billion of new issues, which compares with $30 billion raised in the same period last year. Non-investment grade corporates returned +0.29% in the month as their high coupons offset their price declines. Real Return Bonds returned -3.49% as their very long average durations magnified the impact of the rise in yields. However, RRBs fared substantially better than the nominal Long Term Government Bond index return of -4.77%, suggesting ongoing demand for inflation protection. Preferred shares gained 1.22% as redemptions prompted reinvestment flows and investors anticipated additional redemptions this year.

The surprisingly sharp drop in inflation in the last two months makes the next CPI report on May 21st a particularly important one as it will be the last measure of inflation before the Bank of Canada’s June 5th rate announcement. While we anticipate that inflation will rise back above 3.0% as a result of energy and shelter costs, another lower than expected CPI report may encourage the Bank of Canada to begin easing monetary policy. Should that occur, we would anticipate a rally in bonds, particularly for shorter maturities, leading to a normalizing of the yield curve.

In light of the uncertainty surrounding the next inflation release, we are keeping portfolio durations close to benchmark levels. We are also cautious about extending duration because we believe the Bank of Canada will not lower interest rates as much as the market currently expects. For several years, the Bank has been estimating the “neutral” interest rate, which is neither stimulative nor restrictive, to be between 2.00% and 3.00%. More recently, though, the Bank has indicated that the neutral rate has probably increased. Our view is that the Canadian economy can sustain significantly higher interest rates than prevailed in the 2009 to 2022 period. And if money market yields do not fall below 3.00%, we do not see a lot of value in long term bonds currently yielding roughly 3.60%. We do expect, however, that the yield curve inversion will unwind, potentially in the next few months. Accordingly, we have overweighted the mid term sector to benefit when that curve shift occurs.

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.