Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

John Zechner

August 2, 2017

While the jury is still out on this call, the trend might just be broken this year as the weakness in the U.S. dollar and the significant fall in 10-year bond yields may be telling us that something is ‘not right’ with U.S. growth. Money has been flowing from the U.S. to Europe as growth over there is viewed to be at an earlier stage of the expansion cycle. But if the U.S. economy is in the late stages of their ‘post-2008’ expansion, then the rest of the global economy is probable not far behind. Wage costs and inflation are rising, employment levels are near full, inventories are building and companies are not spending; this is more indicative of an economy in the later stage of the cycle. Stocks generally hit their cycle peaks about 6 months before the peak in growth. We believe we are pretty much at that juncture right now!

Equity bears (such as ourselves) hunting for excesses in the stock market might be better off worrying about bond prices, says former Federal Reserve Chairman Alan Greenspan in a recent interview. “That’s where the real bubble is, and when it pops, it’ll be bad for everyone. By any measure, real long-term interest rates are much too low and therefore unsustainable. When they move higher they are likely to move reasonably fast. We are experiencing a bubble in bond prices. This is not discounted in the marketplace.” While the consensus of Wall Street forecasters is still for low rates to persist, Greenspan is warning they will break higher quickly as the era of global central-bank monetary accommodation ends. “The real problem is that when the bond-market bubble collapses, long-term interest rates will rise. We are moving into a different phase of the economy — to a stagflation not seen since the 1970s. That is not good for asset prices. Stocks, in particular, will suffer along with bonds as surging real interest rates will challenge one of the few remaining valuation cases.”

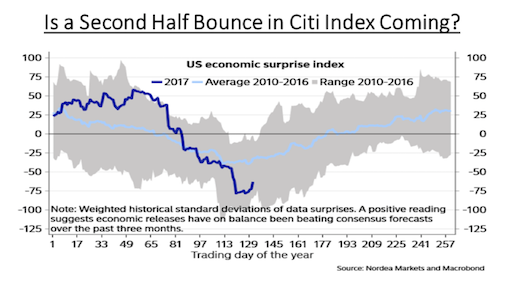

One surprising area of weakness this year has been the value of the trade-weighted U.S. dollar (DXY), which fell 2.9% in July and is down 9.3% so far this year. This comes despite the fact that the U.S. Federal Reserve has raised short-term interest rates three times in the past eight months and the American economy was supposed to be booming under the Trump agenda of lower taxes, less business regulation and increased infrastructure spending. As the policy expectations have clearly fallen well short of the promises, the U.S. dollar has basically given its entire ‘post election’ gains and then some, while bond yields have also traced back over half of their increase seen after the election last November. The weaker U.S. dollar has lead to a recent bounce in commodity prices, which has basically been in a bear market since 2011. Is it time to look at the commodity market? The chart below shows the ratio of the CRB Commodity Index to the S&P500 Stock Index. A rising line indicates a time when commodities do better than stocks while a falling line shows bull markets in stocks. What we can clearly see is that commodities are trading at their lowest level relative to stocks since the Dot-Com Bubble in 2000.

If you’re like us and tend to be one of those who believes in ‘mean reversion’, then it looks like it’s probably a good time to be switching money from stocks to commodities. We have been doing that to a larger degree in our (JZA) Hedge Fund, where we are short the ETF for the S&P500 and long various commodity indices such as oil and gold. The recent moves in the U.S. dollar appear to support this move. Commodity stocks have also seen somewhat of a bounce recently, at least in the base metals, agricultural and coal sectors. From a contrarian point of view the Canadian energy sector is looking extremely ‘oversold’, although the rising Canadian dollar is an additional headwind for that group. Beneficiaries of the rising Canadian dollar would include the travel companies, as demonstrated by recent strong results from both Air Canada and West Jet. However the big Canadian utilities and banks have all made substantial U.S. investments in the past few years and those earnings would be negatively impacted by the stronger Loonie.

Global debt hit a record level this year, mainly driven by emerging markets, raising questions of whether there will be another financial crisis in the near future. Data from the Institute of International Finance showed that global debt reached $217 trillion in the first quarter of this year, or a record 327% of gross domestic product. The debt burden is not distributed evenly. “Some countries/sectors have seen deleveraging while others have built up very high debt levels. For the latter, rising debt may create headwinds for long-term growth and eventually pose risks for financial stability,” the IIF said in its Global Debt Monitor report. High debt levels mean that the debt crisis has not been solved, neither in the U.S. nor the Eurozone. Increasing debt levels in Asia and other emerging market economies also show that a structural change has not yet taken place. All of this, however, does not mean that we are at the verge of another financial crisis. Central banks and low interest rates should continue to limit these risks for the time being. But good times don’t last forever and we continue to see the financial markets as being in a period of high risk.

1 2

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.