Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

John Zechner

June 1, 2021

Stocks rallied and then stumbled a bit in May as investors shifted between buying into the exceptionally strong first quarter earnings reports and then selling on worries about rising inflation rates and the risk that the current economic recovery will lose speed after the re-opening is complete and stimulus support starts to run out. In Canada, the continued recovery in cyclical sectors such as banks, energy, industrials and basic materials powered the SP/TSX Index to a monthly gain of over 3%. U.S. gains were more muted, though, with the S&P500 gaining 0.6%, its fourth straight monthly gain, but the technology-heavy Nasdaq suffering a 1.5% decline, its first negative month in seven. The small-cap Russell 2000 index, which is more leveraged to the economic reopening, eked out a slight gain in May, posting its eighth straight positive month for the first time since 1995.

The good news about reduced Covid cases, increased levels of vaccination and a broader economic re-opening across North America and Europe supported the continued rotation from growth to value stocks and allowed global stocks to start to play ‘catch-up’ to the U.S. This is logical since other global markets do not have the high level of growth stocks in the U.S. indices. This difference in industry weights has helped Canadian stocks generate stronger net gains thus far in 2021, after over ten years of almost-uninterrupted underperformance. Where we go on economic recovery will also control the roadmap for stock market returns for the remainder of this year. Some major indicators such as the monthly U.S. employment report, came in well below expectations, gaining less than 300k versus expectations nearly triple that level! Investors worry that the risks of stagnating vaccination levels, rising inflationary pressures and overly optimistic views on recovery all continued to show up in economic releases throughout the month. The net result was that the Citibank Economic Surprise Index fell to its lowest level since the recovery began, making some investors wary that the ‘best news is already priced in’ to stocks.

Many of these worries were enunciated more clearly in a key report for the group that has been responsible for the strength of financial markets over most of the past decade, and the last year, in particular. “Rising asset prices in the stock market and elsewhere are posing increasing threats to the financial system”, warned the Federal Reserve in its semi-annual Financial Stability Report. The central bank said the Covid-19 pandemic remains one of the biggest near-term risks to the stability of the financial system. “Should risk appetite decline from elevated levels, a range of asset prices could be vulnerable to large and sudden declines, which can lead to broader stress to the financial system,” the central bank said in its semiannual Financial Stability Report. “Such scenarios could materialize if progress on containing the virus falls short of expectations or the recovery stalls, straining some households and firms. While the system overall has remained largely stable even through the Covid-19 pandemic, future dangers are rising, in particular should the aggressive run-on stocks tail off.” I guess we should all considers ourselves sufficiently warned!

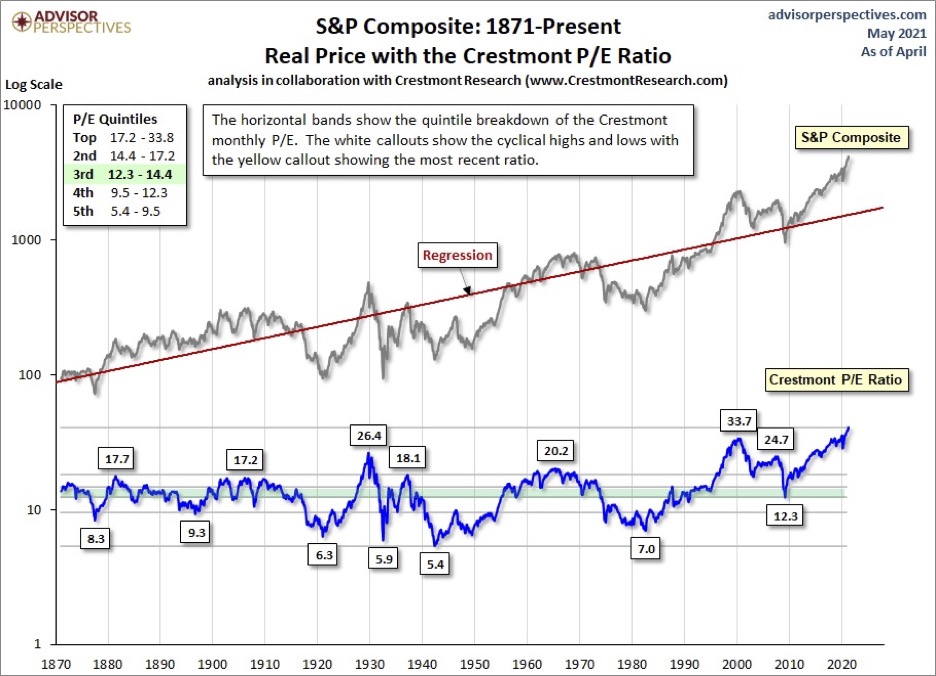

What about those storm clouds? It’s no secret that the biggest threats to current lofty market multiple are higher interest rates and bond yields. The inflation outlook and Federal Reserve policy, which are intertwined, will exert an even greater influence on the market in the second half of 2021. This risk is particularly acute given how extended stock market valuations currently are. How extended? At the end of April, the Crestmont P/E is 179% above its arithmetic mean and at the 100th percentile of this monthly metric that has been used for this analysis for almost 150 years!

While investors need to remain wary of the risks from high valuations or changing growth expectations, we still believe we are in the early stages of a new economic cycle and are hesitant to get too defensive in terms of overall stock market exposure. Our strategy continues to be to shift from ‘interest sensitive’ growth to the more cyclical and value-oriented areas of the market. These businesses are tied more closely to the growing economy, have cheaper valuations and are less sensitive to rising discount rates. This is clearly not a new strategy and has been going on since the first vaccine announcements last November. Since then, the Russell 1000 Value index has beaten its Growth equivalent by about 12 percentage points. But there’s potential for the trade to keep working. Valuations aside, many cyclical and value stocks coming off a nightmarish 2020 are in a position to show faster earnings growth in 2021. On the other hand, the relatively pandemic-insulated software and technology sectors now face tougher year-over-year comparisons. Moreover, when we look back at what we think is a similar shift in performance back in 2001 after the collapse of the tech bubble, value stocks moved into a multi-year period of outperformance that lasted until the collapse of the housing bubble and the resultant Financial Crisis in 2008.

The other big talking point over the past month is the higher inflation numbers and if that will finally push the Fed off this idea that some of this impact will be “transitory”. Adding to the fog of the debate and the uncertainty that has markets churning is that more than a generation has passed on Wall Street since investors had any experience at all with high, long-lasting inflation. When we look back into the 1970s and 1980s, the belief was always that inflation had to be controlled early with higher interest rates. Once it became built into expectations it took a period of much higher interest and/or an economic recession to rid the economy of these pressure. That has been exacerbated in the past year as the pandemic has distorted supply chains in different ways that has lead to key shortages in businesses such as lumber, steel and, most importantly, semi-conductors. These shortages are leading to higher production costs and closed facilities, with the auto industry the most visible casualty of these shortages. On top of that, a record number of businesses say they can’t find workers, inventories are down to cycle lows and a near-record number of companies say they plan to raise prices.

Maybe these inflationary pressures will be only ‘transient’, as predicted by central bankers, but as they become more embedded in wage gains and other product pricing, the more difficult it will be to keep interest rates at such low levels. That remains one of the biggest risk to stock prices, which have spent most of the past decade having their valuations levitated by continually falling interest rates. We’re already seeing some evidence of these rising price pressures. U.S. consumer sentiment weakened in May as inflation concerns picked up. The subdued reading reflects expectations of rising prices in the coming year. In the Michigan Survey, respondents said they expect inflation to average 4.6% in the next 12 months, the highest in a decade. The bottom line here is that, once inflation starts to take hold, the only way to get it under control is through higher interest rates. Maybe the weakness in interest sensitive sectors such as tech and other high growth stocks last month is telling us just that!

1 2

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.