Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

John Zechner

June 1, 2021

There remain lots of reasons to be a bit cautious about the short-term outlook for stocks, notwithstanding the fact that we believe we are still early in this new economic cycle, the re-opening of the economy is ongoing and the central banks remain stalwart supporters of financial markets. But the second and third years of any recovery do tend to run into more headwinds than the first year when expectations are washed out and many investors have been chased out of the stock market. As shown in the chart below, the current recovery is following pretty much the same roadmap as the major recoveries from recession in 1982 and 2009. In both those prior cases, stocks struggled a bit before moving into the next phase of expansion. This can be achieved through a sharp, short-term downturn or simply by seeing stocks remain in a trading range while valuations ‘catch up’ to the underlying stock prices. Despite the shorter-term risks, we see upside over the balance of this cycle so prefer to focus on individual stocks and sectors where we feel that profit performance will be stronger or where valuations give more support. Financials, industrials and energy continue to look like the best choices in terms of meeting those conditions right now.

Can the auto industry remain profitable and grow through the transition from internal combustion engines (ICE) to electric vehicles (EV) and can the oil industry do the same during its planned migration from fossil fuels to renewable energy? If there is one lesson we have learned from investing in technology companies over the past 30 years it’s that transitioning from a slower growth ‘legacy’ business to a higher growth ‘emerging’ business generally runs into more bumps along the way than expected. Take Blackberry as an example. Once known for being the world’s largest smartphone manufacturer, it saw its ultimate demise in that business and has successfully migrated to become exclusively a software provider with a stated goal of end-to-end secure communication for enterprises. However, in the process, it was watched its annual revenue run rate drop from almost $20 billion in 2010 to about $1 billion in the past year and its stock price drop by over 90%, despite remaining profitable and cash positive throughout the transition. The math is simple. Even if the new businesses grow at a 100% rate, it’s never enough to offset the decline in the much larger legacy business, particularly in the early years of the transition.

The auto industry now faces such a challenge. GM and Ford and almost all other ICE auto manufacturers have announced plans this year to migrate all or most of their production to EVs by 2030, undergoing billions in new capital spending over the ensuing period. The risk is that the cash generated from the legacy businesses is not enough to offset the spending required to reach profitability in EVs. Our strategy in this sector has been to focus more on the auto parts companies, such as Magna, Linamar, Martinrea and ABC Technologies in Canada. Their advantage is that only about 10-20% of their sales to auto manufacturers is from ‘drive train’ products (i.e. those that are specific to ICE auto production). The rest of their sales are in areas like communications systems, seating, exteriors and other products that are similar in EVs to those in ICEs. Valuations in those sectors remain extremely low, thus mitigating the risks to a greater degree. It also makes more sense, on a risk-reward basis, than playing the pure EV companies such as Tesla at such excessive valuation levels. Particularly if the existing ICE manufacturers are able to successfully promote their existing brands (i.e. an EV F-150 pickup and Mustang from Ford or an EV Cadillac and Hummer from GM) and also use their auto production expertise to take dominant share in the EV market.

The energy industry faces a similar risk. Big Oil is in transition as the ‘wind has changed’ in the past month. Activist investors added at least two of their own nominees to ExxonMobil’s board after warning the supermajor faced an “existential risk” from its fossil fuel focus. The same day, shareholders approved a measure for Chevron to set strict emissions targets from products that it sells, while a Dutch court ordered Royal Dutch Shell to cut carbon emissions much faster than it planned. Last week, the International Energy Agency said oil companies must stop all exploration projects from this year if global warming is to be curbed. The petroleum-based economy is beginning to unravel. The world is moving to reduce its dependence on hydrocarbons amid growing anxiety about environmental damage. Yes, fossil fuels will remain a major driver of cash flows for the global energy industry for many years, even decades. But many companies will supplement their oil and gas businesses with substantial investments in renewable energy, carbon capture, and other technologies that help to speed the transition away from oil. The road ahead will be bumpy, with plenty of risks. Yet the transformation could also bring enormous opportunities for the companies involved, and their investors. BP believes global oil demand could fall by 10% in the current decade. The company plans to cut its own oil and gas production by 40% by 2030, and to invest $5 billion in wind, solar, and biopower, using the cash flow from its legacy businesses to fuel its low-carbon endeavors. The sharp recovery in oil prices in the past year is giving these majors a chance to use the excess cash flows to build positions in renewable fuels. In terms of our strategy for this sector, we continue to be attracted by the record low valuations and substantial net free cash flow. In Canada we like core oil players such as Suncor and Cenovus as well as the pipeline companies such as Pembina, Enbridge and TC Energy. Natural gas-oriented majors such as Tourmaline and Arc Resources also look good as their balance sheets are in great shape and their growth profiles remain strong. We are also starting to add in some renewal energy names such as Algonquin Utilities and Northland Power, especially now that their valuations have dropped sharply over the past few months.

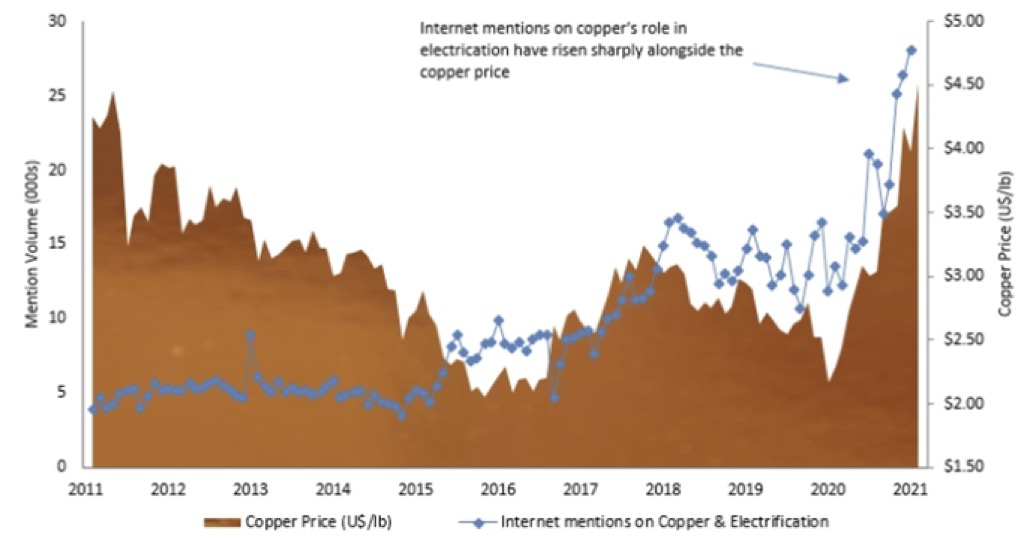

While the recoveries in oil and lumber over the past year have attracted much attention, a true standout has been the copper market. Supplies have been curtailed by some production outages as well as a decade of under-investment in new projects. Demand, on the other hand, is being supplanted by far more than typical capital spending recoveries in the U.S. and China as copper sees greater growth from its use in electrical vehicle production as well as the rollout of 5G communications networks. Rising demand and restricted supply is always a great combination for higher prices. Teck Resources is seeing its major Quebrada Blanca project some on at just the right time while First Quantum Minerals, another Canadian major, is now seeing dividends being paid from its developing Cobre Panama copper project in Panama, which had been seen as somewhat high risk at the time but is now looking like a very timely purchase.

Finally, while we already know that Amazon Inc has decimated the competition in ‘bricks and mortars’ retailing as well as becoming one of the largest players in the high growth ‘cloud services’ industry (through AWS), it has also quietly moved up to become the second largest player in the exploding ‘streaming’ business. According to a report from Consumer Technology Association, projections put the total spending on streaming programming at $112 billion in 2021, an increase of 11% over last year and a 31% increase over 2019. While this growth may subside in the short term as the re-opening occurs and consumers move away from some online activities, there can be no doubt about the longer-term trend away from traditional network programming to streaming as the most profitable source of industry growth.

Amazon continues to position themselves as a core player in this rapidly emerging industry. The rumoured $8.5bn acquisition of MGM Studios, which would be Amazon’s largest since it bought Whole Foods for $13 billion, will help drive Prime subscriptions which, in turn, should help Amazon even more. While other players are spending money they do not have, Amazon is building itself an even stickier subscription platform, a recurring revenue bundle, that is unrivaled by any peers. Imagine going to the mall, and for a monthly fee you get all the entertainment the mall has to offer while at the same time discounts at every store, and on top that, someone carries your bags around! In a nutshell, that was Amazon is doing to traditional retail as they continue to solidify their growth profile and dominance. While the valuation has always seemed excessive (maybe even crazy), clearly they have delivered on their growth promises and are becoming more profitable all the time. Don’t own for the long term at your own risk!

1 2

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.