Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

John Zechner

June 28, 2017

We don’t claim that anything in this Index should move financial markets and the index’s creators do not argue that it means recession necessarily follows peaks in the Index Value. They only say there is a measurable economic effect from uncertainty. The trouble for the U.S. president (and probably the financial markets) is not that the index spiked since his election, it’s that uncertainty has remained elevated since then and shows little sign of abating. Probably worth an investor’s time to track the President’s comments on Twitter, just so you can stay on top of the comments on a timely basis!

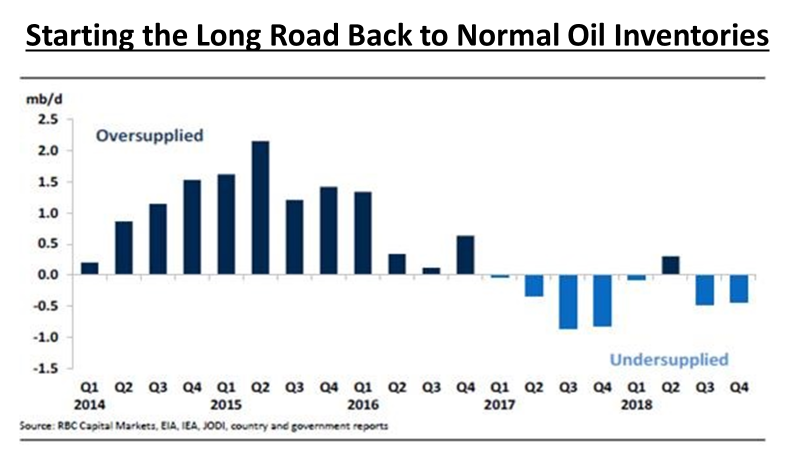

One of the biggest disappointments in the first half of the year has been the performance of the energy sector as oil prices have fallen over 15%, despite good adherence to the production cuts enacted by major oil producers last November. While the negative story on oil over the prior two years had been the record build-up in global inventories of energy products, it appears that oil inventories peaked both on a notional basis and relative to seasonal normal levels during the middle of 2016. The path to running down those stocks, though, has been bumpy ride. While OPEC has voiced the intention of running inventories back toward seasonal normal levels, outright oil inventories are some 280 million barrels in excess of the five-year average. While this represents a level that is already 20% lower than last year’s peak, the current balances suggest that inventories will not be fully rebalanced until late mid-2018.

The problem for the oil market has come from both supply and demand sides. While global demand growth has come in below expectations, the U.S. shale oil producers have offset a good portion of the OPEC reductions by increasing domestic production. The shale oil group has increased spending and appears to be able to generate profits to prices as low as US$40 per barrel. That could then provide the floor for oil prices. Given that the energy stocks have begun to reflect this ‘worst-case’ scenario for oil prices, we are starting to see some better value in the group and have been adding to positions in the past month. The best time to buy is when no one else seems interested and sentiment is bearish. Can’t think of another market sector that meets that criteria better than oil right now!

Elsewhere in our portfolios we remain underweight in stocks overall but overweight in U.S. technology stocks for their consistent long-term growth and reasonable valuations. We have reduced positions in both the financial and basic materials sectors due to our less buoyant outlook on economic growth. We remain with a slight overweight in preferred shares due to their high gross yields and positive fund flows. Given this overall defensive investment stance, it should be no surprise that we also have a larger than normal weight of cash in all of our managed portfolios.

John Zechner

Chairman and Founder

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.