Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

John Zechner

June 28, 2017

Stocks continued their upward move during the 2nd quarter as investors focused on strong first quarter earnings reports and improved global economic growth, ignoring the political noise in the U.S., growing geo-political risks internationally, rising interest rates in the U.S. and slower economic growth. Other risks that failed to stop the upward move included the facts that stock valuations remain near the highs eclipsed only prior to the ‘technology bubble’, number of stocks participating in the gains continues to narrow and that key commodity markets such as oil, gas, copper, met coal, iron ore and the U.S. dollar have all been falling so far this year. Index fund flows have been the big driver of stocks all year as ETFs (Exchange Traded Funds) have been the primary source of demand. These flows can be seen in the late day market moves as these funds tend to drive ‘last hour buying,’ a trend that dominated most trading days so far this year. We would point out, however, that the last few weeks of June have seen a bit of a reversal in these flows with some of the ‘last hour buying’ turning into ‘last hour selling’. While this is a very recent development, it might indicate that this large pool of stock buying has dried up. The second half of 2017 should be interesting, and probably a lot more volatile than the first half.

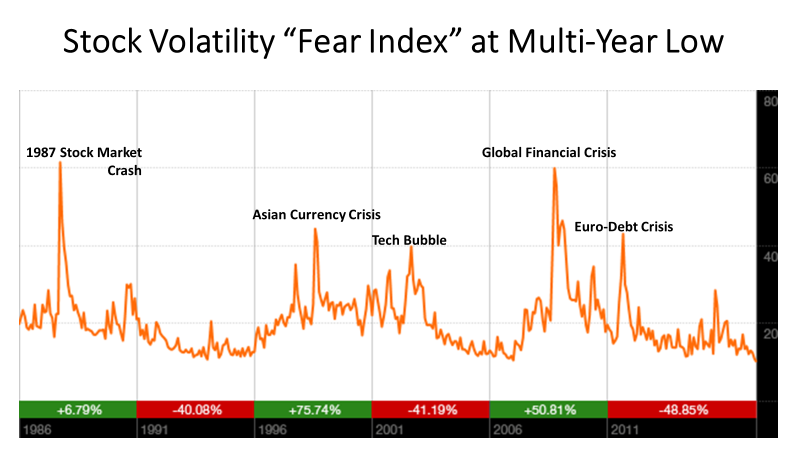

As we pointed out last month, investors seem oblivious to fear about any negative developments that could hurt stock prices, which is reflected in the ‘VIX’ or ‘fear index’, shown in the chart below. This measure of stock volatility continued to drift to record lows in the first half of 2017. While low volatility, in and of itself, is not shown to be a causation of market tops, history has shown that stocks market peaks have historically always occurred during periods of low volatility while market bottoms have always been associated with upward spikes in volatility. This suggests to us that there is very little chance that we are not in the late stage of this bull market.

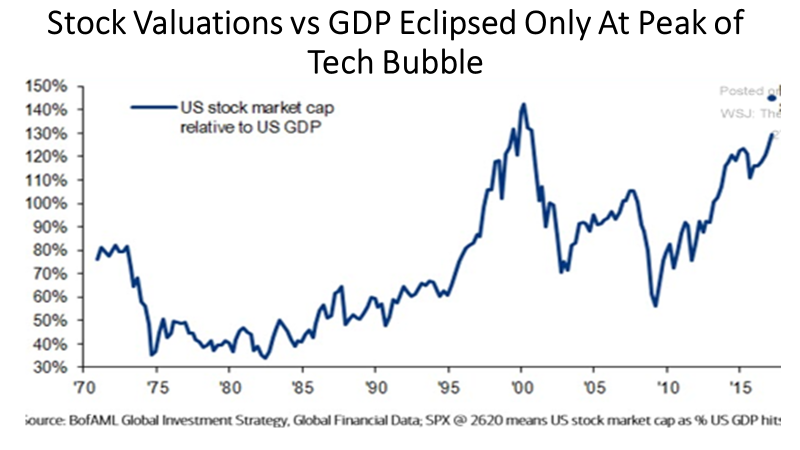

While investors seem entirely unconcerned about both the market and ‘non-market’ risks, they also do not seem worried at all about the record valuation of the stock market. The continually dropping level of interest rates over the past eight years seemed to be the logical reasoning for the rising valuation for the stock market. How many times have we heard the TINA (There Is No Alternative) argument for buying stocks? That argument seems to be reversing this year as the U.S. Federal Reserve has now increased interest rates four times in the past 18 months and now plans to begin reducing its massive US$4.5 trillion balance sheet by selling bonds, rather than its ongoing buying of government bonds during the prior periods of quantitative easing (QE). Moreover, the European Central Bank is starting to make similar noises about ending their QE program as growth picks up in the Euro Zone. The bottom line is that many of the tailwinds of the past few years are starting to turn into headwinds. Yet, as shown in the chart below, the world’s largest stock market is trading at a valuation (relative to GDP) about 40% above the long-term average and a level seen only during the peak of the technology bubble in the year 2000.

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.