Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

John Zechner

May 5, 2017

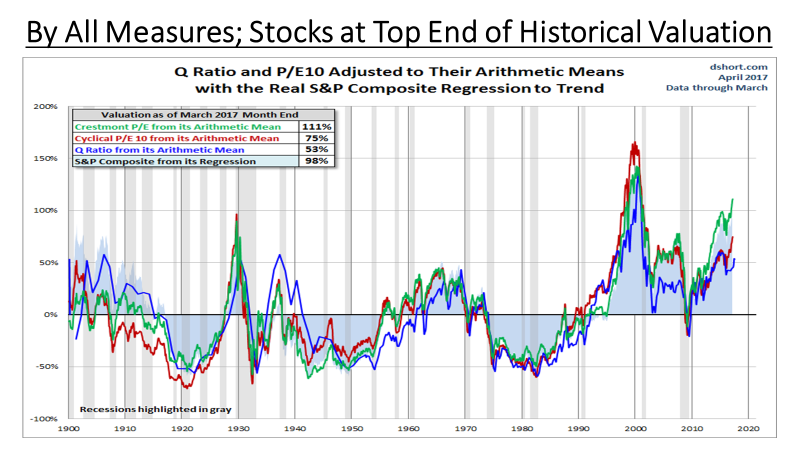

As long as we’re piling on worries about the economy and financial markets, we would be loathe to ignore the overall current valuation of the stock market. While markets could be expected to have higher valuations early in the economic cycle when growth and earnings are in their early recovery stages and interest rates are falling. That’s not the case today as we are 8 years into a recovery and interest rates have most likely seen their lows for the cycle. Yet, as shown in the chart below, a plethora of standard valuation measure for stocks basically all show the market at its highest historical level, outside of the technology bubble in the late 1990s. The Crestmont PE (Price-to-Earnings ratio) is 111% above its historical average level, the Cyclical PE is 75% above, the Q-Ratio is 53% above and the S&P Composite Index is 98% above its trend level. While we are not predicting any imminent collapse in stock prices, particularly since money flows into stock ETFs are currently so strong, the risk-reward ratio of owning stocks is clearly not in investors’ favour at current levels.

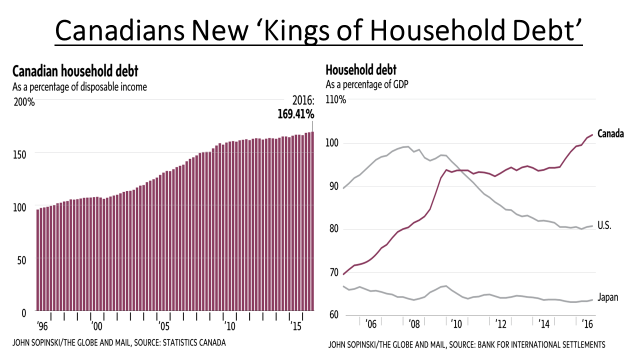

Back in Canada we have to deal with our own issues, including potential trade disputes with the Trump administration, high-lighted by new initiatives from our southern neighbour on both dairy and softwood lumber. President Trump has also threatened to ‘rip up’ NAFTA if a new deal that is more favourable for Canada can’t be negotiated. However the bigger issue in Canada has been the rising level of household debt that has coincided with the strength of the housing market. As shown left panel below, Canadian household debt has soared in the past 20 years from 100% of household income to an all-time high of almost 170%. Low interest rates have made the servicing of these debts less onerous but, with rates probably having seen their lows for the cycle, those costs could clearly rise. To put this number in perspective, the right panel shows this debt as a percentage of GDP compared to that in both the U.S. and Japan.

Back in Canada we have to deal with our own issues, including potential trade disputes with the Trump administration, high-lighted by new initiatives from our southern neighbour on both dairy and softwood lumber. President Trump has also threatened to ‘rip up’ NAFTA if a new deal that is more favourable for Canada can’t be negotiated. However the bigger issue in Canada has been the rising level of household debt that has coincided with the strength of the housing market. As shown left panel below, Canadian household debt has soared in the past 20 years from 100% of household income to an all-time high of almost 170%. Low interest rates have made the servicing of these debts less onerous but, with rates probably having seen their lows for the cycle, those costs could clearly rise. To put this number in perspective, the right panel shows this debt as a percentage of GDP compared to that in both the U.S. and Japan.

The Japanese have always been net savers and this has allowed the country to keep their borrowing needs within their borders. The U.S., on the other hand, did go on a ‘debt binge’ similar to what we have in Canada during their housing boom from 2003-2008. The unwinding of that debt bubble (and how it was financed) was one factor that lead to the Financial Crisis in 2008 that ended up threatening the entire global financial system! The recovery from those excessive debts required years of record low interest rates and kept the U.S. economy as a relative under-performer for most of the past 8 years. While this is not exactly a blueprint for what could happen in Canada, the risks of these excessive debt levels will come into play over the next few years. The recent weakness in the Canadian dollar is most likely one of the early casualties of this loss of global confidence in our financial and economic outlook.

The fallout from aggressive lending practices and investor confidence in those lending institutions showed up in April in the performance of beleaguered Home Capital Group (HCG), which fell almost 70% in April as it announced an emergency funding package designed to backstop the mortgage lender’s bleeding deposit base. They also disclosed that the onerous terms of the financing will cause the company to miss its financial targets for the year. The Toronto-based company, which is Canada’s largest alternative mortgage lender with $18-billion in home loans outstanding, drew down half of a $2-billion line of credit secured in an attempt to stabilize the bank. Depositors have been fleeing Home Capital and the company lost more than $1.5-billion in savings deposits since late March. The run on the bank comes in the wake of allegations from provincial securities regulators that senior executives at the lender had misled investors in 2015, after discovering fraudulent documentation on loans originated by some of its staff. Whether this is the ‘canary in the coal mine’ for the downturn in the housing sector in Canada is yet to be determined but we don’t believe that the contagion will end here.

In fact, subsequent to the breaking of the HCG news, one of Canada’s largest private real estate investment firms sought creditor protection, owing hundreds of millions of dollars to thousands of individual investors and blaming a downturn in the Alberta economy and shifting appetite among U.S. property developers for its financial woes. Calgary-based Walton Group of Companies is a major land banking and real estate development company, which owns more than 105,000 acres of property in Alberta, Ontario and several U.S. states. It advertises that it has $5.2-billion worth of assets under management in Canada and the United States spread out across what court documents describe as an “extremely complex structure of more than 600 corporations, limited partnerships and other entities.

The bottom line, in our view, is that there are a growing number of risks in the economy and, more particularly, financial markets that have been artificially supported by an extended period of abnormally low interest rates. As prudent money managers, we have to be aware of these risks and invest our client assets accordingly.

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.