Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

John Zechner

May 5, 2017

Global stocks staged a recovery in the final week of April, lead by the European indices which were buoyed by the first round of results from the French elections in which Emmanuel Macron, a more moderate candidate, appeared to have an insurmountable lead for the final election on May 7th. This removed one near-term major fear in the market, which was a further fracturing of the European Economic Union and the potential end of the Euro. The ensuing rally left markets with slight gains for the month, as most had been under pressure in the first part of April as investors worried about geo-political risks which, in addition to the Euro-risk, the confrontation between the U.S. and North Korea as well as ongoing and escalating issues in Syria. On top of that, U.S. economic numbers were clearly weaker than expected in the first quarter. While the optimists blamed this on the seasonal weakness we have seen in the first quarter over the last five years, the reality is that growth in the U.S. was only 0.7% in the first three months of 2017. More importantly, the economic numbers do not appear to have picked up any momentum in April.

Another source of strength for the stock market in April was the positive results from first quarter earnings reports. Expectations were for year-over-year growth of 10%. With over 60% of companies having already reported, the results are running ahead of that expectation with a gain of about 13%. One interesting note from the U.S. companies earnings season reports is that the less a U.S. company is exposed to America, the better its results. S&P500 companies that generate more than half their revenue overseas are posting first-quarter earnings growth of 19.9% on average, double that of companies that conduct most of their business domestically, according to FactSet. That helps explain the gap between the strong quarterly earnings results and sluggish economic data like the GDP report showing U.S. growth of just 0.7% in the first quarter, its slowest pace in three years.

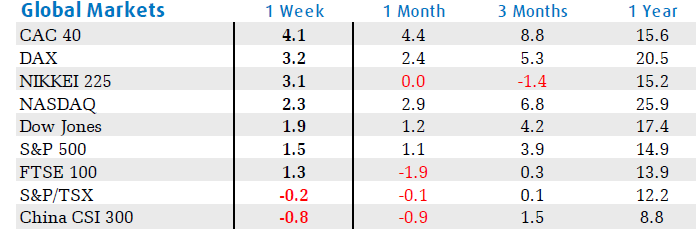

But the money flows into stocks continue to dominate market moves and this pushed most indices to monthly gains in April, as shown in the table below. France and Germany lead the winners, up 4.4% and 2.4% respectively. Growing Brexit worries pushed London stocks lower while weaker commodity prices were also drags for the Canadian and Chinese markets. U.S. stocks had mixed results but once again the technology stocks were the bigger winners as strong earnings reports from Alphabet (Google), Amazon and Microsoft helped push the Nasdaq Index up another 2.9% to a record high.

![]()

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.