Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

John Zechner

April 7, 2017

Another reason we are cautious on stocks is that so few investors are not. Typically, the best gains are seen by making investment decisions when sentiment indicators are at extreme levels. Forget the dot-com boom with its “irrational exuberance” and the real estate bubble that was supposed to be invincible: Current stock market sentiment eclipses all of that. In fact, bullishness has never been this high going all the way back to 1987. Bullishness is at 63.1% of market professionals responding to the latest Investors Intelligence survey. That’s the highest level since the year of the infamous “Black Monday” Oct. 19, 1987, crash that sent the U.S. market down nearly 23% in one day. All the optimism comes with the market setting a succession of new highs. A recent sentiment survey from the Yale School of Management shows the collective fear of missing out on stock market gains could be a big reason investors keep buying. Asked if the stock market will be up a year from now, investors registered a big jump in confidence to the highest level in at least 15 years. Yet when asked about valuations, were far less assured and believed the market was overvalued. ‘Stocks are expensive but let’s keep buying so we don’t miss out on gains.’ Sounds like the definition of a bubble!

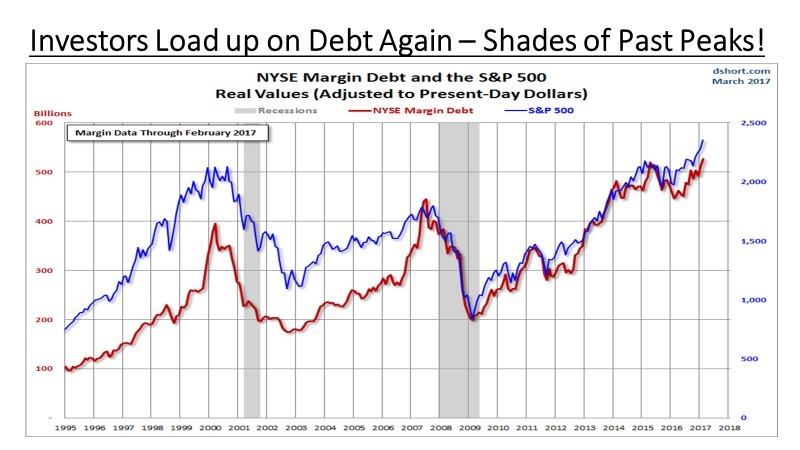

Another example of how enamoured investors are with stocks can be seen in the data on Margin Debt (investors borrowing to buy stocks) as measured by the New York Stock Exchange and shown in the chart below. The red line shows the dollar level of margin debt. Investors continue to bet big on the Wall Street bull, at a time when stocks are hovering near records but have been unable to break through to fresh peaks. The latest data show margin debt, or cash borrowed to buy shares, hit a record $528.2 billion in February, up from its prior high of $513.3 billion in January. Borrowing money to buy stocks is a sign that investors remain optimistic the market will continue to rise. Like any form of leverage, there’s always additional risk after taking out a loan to fund the purchase.

Falling stock prices and a resulting drop in one’s brokerage account balance could force investors to have to put up more collateral to meet the lender’s requirement. In the past, this has made market downturns even worse as the investors have to sell stocks that are falling in value to raise the cash. Looking back, we see that Margin Debt peaked at over US$400 billion in 2008, just as the S&P500 (blue line) was also hitting peak levels. Prior to that, debt rose to almost US$400 billion in 2000, again coinciding with that peak in the stock market.

The only problem with these concerns is that valuation or sentiment alone are seldom something that derails a bull market. Usually some unforeseen catalyst occurs first, which then exposes just how out of whack things were. Timing then becomes the bigger issue. But we tend to look at markets more in terms of a ‘risk/reward’ profile than a market timing issue. Looking back at the technology bubble in the late 1990’s, one could easily argue that stocks became over-valued in 1998, a full two years before the market hit its ultimate peak. But, when in fell, it dropped far below those 1998 levels so getting defensive at that point was not necessarily a losing strategy. We see a similar situation today. While we can’t forecast when the stock market will see it’s peak, we don’t see the upside from continuing to own an overweight position in stocks as great as the potential downside from a correction in prices to historical valuation levels. Moreover, downside risk could be amplified due to the excessive margin debt of investors or a con-current slowdown in economic growth and corporate profits. Our investment strategy therefore continues to be to reduce stock positions into strength, add deep value positions with less downside and invest in some ‘safe-haven’ areas such as gold.

‘Canadianizing’ the oil patch again. Events over the past month will ensure the Canadian oil sands industry survives for decades to come, albeit as a shadow of its former self. In March alone, two of the largest Canadian players spent more than $30 billion in cash and stock scooping up oil sands assets once held by international supermajors. Canadian Natural Resources is spending $12.7 billion to all-but-buy out positions from Royal Dutch Shell and Marathon Oil. Then Cenovus announced its largest-ever acquisition as the company is buying out its Texas-based joint-venture partner – ConocoPhillips – for a whopping $17.7 billion. Cenovus CEO Brian Ferguson called it a “transformational acquisition” for the Calgary-based company. “In a low oil price environment, economies of scale are important. This deal about doubles the scale of the company and this will give us a greater competitive edge.”

Earlier this year, Norway’s Statoil sold its Canadian oil sands assets for $832 million. A year ago, Suncor Energy took majority control of Syncrude with a $937-million purchase of American Murphy Oil’s 5% stake in the mine. Whether the Canadians are making the right call by basically ‘doubling-down’ on their oil sand positions or the international investors are exiting at the right time won’t be known for years. If oil prices don’t break below the US$50-60 range, then these deals will be positive for the Canadian buyers. But if prices break below those levels, the Canadian buyers will have difficulty managing the significant debt loads taken on to buy back these assets. The oil sands are high cost projects to build, but don’t require as much to operate so it makes more sense for the Canadian companies to buy in the balance of existing operations as opposed to starting expensive new projects. For the foreign sellers, they mostly need to repair their balance sheets from these acquisitions that were made at much higher prices and the re-invest some funds into the shale oil operations in some low-cost regions such as the Permian Basin in Texas. In the end, it might be good deals for both sides! But, for now, it’s a big bet by the Canadians on the direction of oil prices.

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.