Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

John Zechner

April 7, 2017

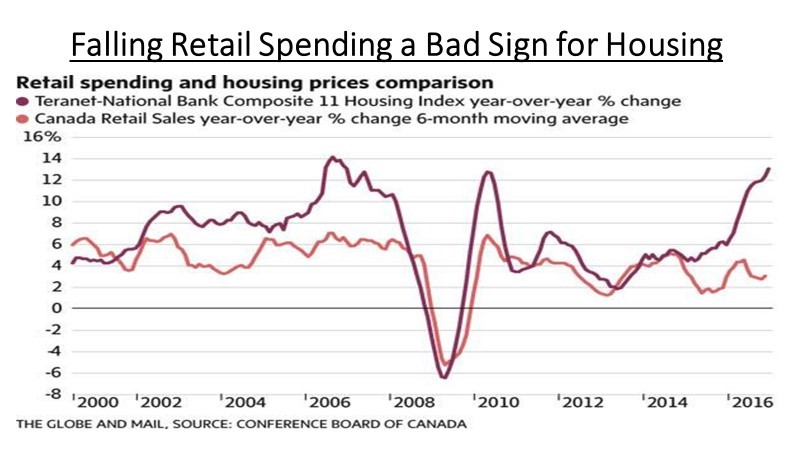

Canada’s real estate market continues to ride a euphoric wave of high prices and foreign buying, but at some point, all good things must come to an end. While we are not projecting any imminent demise in our housing market we are starting to notice some ‘cracks in the armour.’ While we all recognize that Canadian real estate does not look expensive compared to Hong Kong or some of the other centres where much of the foreign buying is coming from, the recent BC Provincial tax on foreign buyers has shown how susceptible this market has become to the sudden removal of that buying. A more worrying sign for us is the recent breakdown between retail spending growth and housing price increases in Canada, as shown in the chart below. They generally tend to move in tandem as rising house prices means consumers feel wealthier and they tend to spend some of that additional wealth which, in turn, keeps economic growth moving ahead. Also, rising home prices are generally indicative of a growing market which means that new buyers need to buy home accessories etc. But this relationship has fallen over the past year as home prices have continue to rise but retail spending growth has slowed down.

While a large part of that spending may be specifically related to the problems in Alberta in 2016, the housing market does seem to be at somewhat ‘historically unsupported’ levels. Moreover, affording a home in Toronto is the toughest it has been in more than 25 years, Royal Bank of Canada warns. Not only that, the “squeeze” is spreading in Southern Ontario, with evidence suggesting the Toronto area is now a “high-risk” zone that calls for government intervention. The housing affordability measure – the proportion of median pre-tax income needed to juggle mortgage payments, property taxes and utility bills – puts Toronto at its most stressed since 1990. Any breakdown in the Toronto, Vancouver or overall Canadian real estate market would have immediate ripple effects on the overall economy since that sector has been responsible for much of the economic growth over the past three years. This would also create downside risk for the stock market, particularly the banking sector.

The bottom line is that nothing has really changed in our investment strategy and views despite some further strength in global stocks in the first quarter. While growth has picked up in Europe, the U.S. actually looks to be missing some of their targets lately and will probably end up showing growth of only about 1% in the first quarter. Canada has generated some better numbers lately as trade has picked up, but we remain tied to the bigger moves in the global economy. Investors, meanwhile, seem oblivious to economic, geo-political and policy risks and continue to look for further growth. But stocks have not experienced a bear market since 2011, much longer than the normal period. Valuations are stretched and profit expectations seem ‘overly optimistic’, in our view. On top of that, investors can no longer count on the ‘largesse’ of central banks to support stock valuations as rates are clearly headed higher in the U.S., the Europeans are looking at tapering back their bond market purchases and the Bank of China is tightening policy. So the ‘zero interest rate policy’ party is also coming to an end. All we are left with is record government debt levels and mediocre growth! We continue to hold higher than average cash levels and added to positions in gold stocks in the portfolio. Bring on the second quarter; we’re not waiting for the ‘Sell in May and go away’ indicator. We believe the time for caution is now!

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.