Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

John Zechner

April 1, 2025

We had three major concerns about stocks coming into this year: valuation, investor sentiment and portfolio positioning. Two of the three remain an issue but sentiment has quickly reversed with all the negativity of the past month and is quite bearish now. If nothing else, this increases the chances for at least a short-term bounce. Any rally will run into selling though since ‘positioning’ is still too high with individuals still having over 70% of their financial assets in stocks (a record), mutual fund cash levels at lows and ‘quant funds’ still net bullish. That means that any rallies will most likely be met with ongoing selling (much like what we see recently with rallies in the morning running into selling into the afternoon and close). The selloff in stocks was quite pronounced as the S&P500 Index underwent one of the sharper 10% gut checks in memory over three weeks into March 13, before pivoting higher with two days of broad, encouraging buying, followed by another pop on hopes of a more moderate tariff campaign. Since then, it’s been a lot of messy churning in a headline-sensitive, irresolute tape. No more than 40% of the total pullback was ever recovered, before last week’s late sell-off on stiff auto tariffs and disappointing consumer-spending and inflation readings. The extremity of the negative attitudes right now has Wall Street acutely sensitive to any evidence that such “soft” survey results are bleeding into the measured “hard” data tracking real activity. Translation: U.S. consumers have been ‘talking the talk’ in terms of getting more worried about the future but now we expect to see them ‘walking the walk’ as they translate those fears into reduced spending by both individuals and companies.

The ‘wealth effect’ also continues to work in reverse as stocks fall. The leaders of companies that serve everyone from penny-pinching grocery shoppers to first-class travellers are seeing cracks in demand, a shift after resilient consumers propped up the U.S. economy for years despite prolonged inflation. On top of high interest rates and persistent inflation, CEOs are now grappling with how to handle new hurdles like on-again, off-again tariffs, mass government layoffs and worsening consumer sentiment. Across earnings calls and investor presentations in recent weeks, retailers and other consumer-facing businesses warned that first-quarter sales were coming in softer than expected and the rest of the year might be tougher than Wall Street thought. Many of the executives blamed unseasonably cool weather and a “dynamic” macroeconomic environment, but the early days of President Donald Trump’s second term have brought new challenges — perhaps none greater than trying to plan a global business at a time when his administration shifts its trade policies by the hour. Economists largely expect Trump’s new tariffs on goods from China, Canada and Mexico will raise prices for consumers and dampen spending at a time when inflation remains higher than the Federal Reserve’s target. In February, consumer confidence — which can help to signal how much shoppers are willing to shell out — saw the biggest drop since 2021. A separate consumer sentiment measure for March also came in worse than expected. Earnings reports from huge retailers such as Walmart, Home Depot, Dick’s Sporting Goods, Kohls, Nike, Lowes as well as Fedex and the major airlines such as Delta, United and American Airlines all echoed this subdued outlook, which in some cases had been positive outlooks at the beginning of 2025. Companies, too, are showing signs of concern by limiting travel, slowing hiring, and taking other steps to rein in spending and those concerns have already started showing up in earnings guidance.

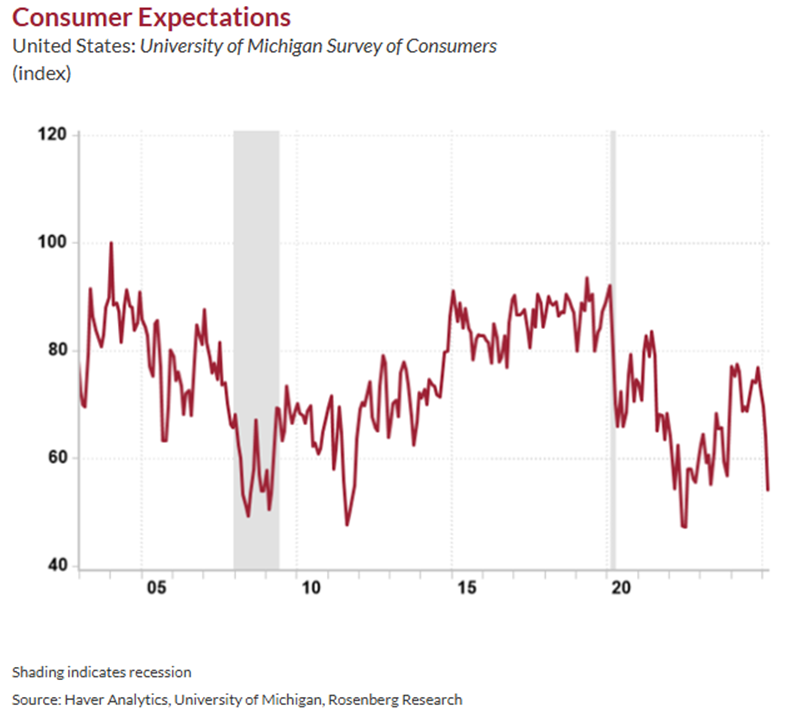

Bullish sentiment for stocks cratered in historic fashion this past month as President Trump’s haphazard rollout of tariffs rattled markets and raised concerns about economic growth, according to the most widely followed investor survey on Wall Street. Bank of America’s Global Fund Manager Survey for this month saw its biggest pullback in overall investor sentiment since March 2020, back when stocks plummeted as the U.S. grappled with the Covid-19 pandemic. This month’s steep decline is the seventh largest over the past 24 years and brought the overall sentiment measure to a seven-month low. The sentiment index comprises three components: equity allocation, cash holdings and economic growth expectations. However, despite the ‘crash’ in sentiment, positioning in the survey is “nowhere near” levels that reflect an “extreme bear” environment or one in which investors should “close-your-eyes-and-buy.” Investors still carry stock weights well in excess of historic norms, which could mean more selling on any rally. The index of consumer expectations in March sank -10 points to its lowest level since July 2022 and the third lowest level in thirteen years. This suggests a future of very subdued growth in consumer expenditures. This is bearish for Consumer Discretionary stocks but bullish for the Treasury market. The deterioration in consumer sentiment was even worse than anticipated in March as worries over inflation intensified, according to a University of Michigan survey. The final version of the university’s closely watched Survey of Consumers showed a reading of 57.0 for the month, down 11.9% from February and 28.2% from a year ago.

In addition to worries about the current situation, the survey’s index of consumer expectations tumbled to 52.6, down 17.8% from a month ago and 32% for the same period in 2024. Inflation fears drove much of the downturn as inflation expectations for the year ahead jumped to 4.9% this month from 4.3% in February, marking the highest reading since November 2022. Long-run inflation expectations surged to 3.9% from 3.5% in the prior month. This is the largest monthly increase since 1993. That is a bigger problem since stickier inflation at elevated levels would encumber the Federal Reserve’s ability to cut interest rates to revive growth. Tariff policy has hit consumer sentiment hard and threatens to keep shoppers at home.

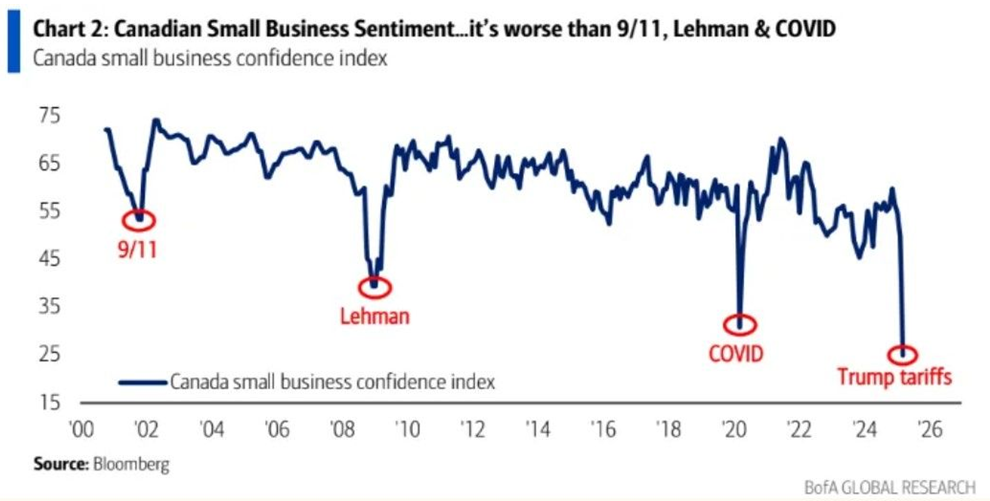

Oh Canada! Economically we have been hit harder than most during the initial round of tariff announcement and that is adding to the downward economic pressures that we had already been feeling prior to the U.S. election results last year. More evidences of this deterioration came to light last month with the outlook sinking to multi-year lows as small business sentiment in Canada came out from the CFIB for March. Sentiment for the coming year crashed to its lowest level on record, with the index plunging to 25.0 from 49.8 in a decline that has never been seen except for March 2020. The level is worse than it was during the pandemic, the Global Financial Crisis, and 9/11. Between tariff threats, political uncertainty, and overall economic activity, there’s a lot weighing on the minds of small business owners. Even though we saw a slight uptick in Canadian inflation in March (due mostly to the end of the two month ‘HST holiday’) we expect the dire economic outlook and tariff uncertainty will motivate the Bank of Canada to resume its policy of reducing short term interest rates in Canada, which are now at 2.75%.

Gold versus Bitcoin in the ‘store of value’ world. Some commentary suggests that both meet that need but for different reasons. In a more light-hearted way, we might say “Bitcoin in a store of value for optimists while gold is a store of value for pessimists!” While the reality of that comparison is certainly subject to debate, the evidence is quite compelling as Bitcoin has rallied the past few years along with other ‘risk assets’ such as high growth stocks. In fact, the correlation between Bitcoin and other ‘risk on’ assets has been quite high, on both the upside and the downside. That deviation has been seen so far this year as the stock market’s trepidancy over the Trump tariffs lead gold to move to new all-time highs above US$3,100, while the Bitcoin rally that had gotten new momentum after Trump was elected, took some major steps backward. The biggest position argument in favour of cryptocurrencies such as Bitcoin has been where the investment demand will come from. That sustained the sharp rise to record highs in 2024 as Bitcoin ETFs were approved for sale by U.S. regulators. But that changed this year as U.S. Bitcoin exchange-traded funds recorded their longest run of weekly net outflows since listing in January last year as US President Donald Trump’s tariffs drove a wider retreat from riskier assets. Investors pulled over $5.5 billion in total from the group of 12 ETFs so far in March. The record outflows started shortly after Trump returned to the White House, underscoring how even crypto investors have focused more on the trade war he ignited than on his crypto-friendly policies like creating a digital-asset stockpile.

Gold, on the other hand, has seen continued buying as global central banks are diversifying their reserves out of dollars and into gold. This is a massive and ongoing tailwind for the yellow metal. In the past three years alone, central banks have bought more than 1,000 metric tons of gold each year, according to the World Gold Council. But it’s not just the central banks. Gold holdings in U.S. ETFs have risen +4.3% so far this year to 1,650 tons and by +3.6% to 1,334 tons in Europe. The central banks should be viewed as more stable, longer-term holders of bullion than the investment world’s buyers of crypto ETFs. Gold also has the benefit of ongoing jewellery demand in addition to investment demand. That might not be enough to continue pushing prices higher, but it is a notable difference from Bitcoin, where investment demand appears to be the only story. We have yet to see widespread adoption or cryptocurrencies for transactions, something that would seem to be essential to any long-term sustainability of the interest in this asset class. Meantime, gold stocks are looking cheaper relative to the price of gold bullion than they have at any point in the past 40 years, even after the nearly 20% gain in prices in the first quarter. We expect to see corporate activity pick up in the gold sector since it is much less expensive for existing players in the industry to expand by acquiring competitors versus exploration and development of existing resources. Rising material, labour and environmental costs, in addition to heightened global geopolitical risks have combined to make almost any new project exceed initial cost and timeline estimates. For gold producers, it is much cheaper to ‘buy’ than ‘build.’

Investment strategy changes in volatile times. Not much has changed in our view in the first quarter of this year. Tariff and other geo-political and economic risks, combined with valuations still near record levels, make it difficult to advocate for an overweight position in stocks. However, given the sharp recent drop in investor sentiment, we are beginning to see the downside risks as more mitigated and the potential for at least a ‘recovery bounce’ increasing. Technology stocks have been the hardest hit sector, yet the growth opportunities for that group remain in place suggesting that we might see a bounce in that sector first. But our strongest conviction remains with the bond market. We don’t see any way that tariffs will not lead to an economic slowdown, even if those same tariffs slow down the reduction in inflation rates. Interest rates should go lower in both the U.S. and Canada, and we continue to hold overweight positions in longer-term government bonds as a hedge against both potential stock market weakness and/or an economic recession. While still slightly underweight stocks in general, we continue to favour those sectors with high dividend yields, economically resilient earnings growth and moderate valuations. Telecom, utility, health care and pipeline stocks continue to meet those criteria most closely. The outlook for cyclical stocks continues to be cloudy in our view and we remain underweight the consumer, financial, industrial and basic material sectors until we see some more stabilization on the tariff front or some improvement in the underlying economic outlook. No need to ‘run for the hills’ right now as there remain plenty of opportunities for gains in financial markets in areas such as long-term bonds and gold stocks, much like what we saw in the first quarter. But this is also not a ‘risk on’ environment where investors should be adding exposure.

1 2

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.