Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

John Zechner

April 1, 2025

Following the U.S. election results last November, stocks surged over the next month to all-time highs with rallies in technology, financials, consumer, industrial and small cap sectors leading the way. In the midst of this ebullience, we said in our year end commentaries that “a year from now there are two phrases that we would be hearing much less of, if at all; ‘animal spirits’ and ‘U.S. exceptionalism!’ It took far less time than we expected for those terms to disappear from the business lexicon. The ‘animal spirits’ were referring to the expected increase in corporate takeover activity, bank lending, business capital spending and new public equity offerings as a result of reduced regulation, particularly in the financial sector. But the uncertainty around tariffs and the negative impact on consumer sentiment have put those spirits to rest. Corporate takeover activity has sunk back to the pandemic lows while IPOs (Initial Public Offerings) of stocks have been almost non-existent. In fact, the only major tech offering to make it through so far this year was CoreWeave, and even that one barely got over the ‘finish line.’ The plan was to sell over $4 billion of shares in the $47 to $55, but investor demand failed to materialize due to a difficult public market environment and questions surrounding the sustainability of the company’s business model. Nvidia, a major supplier and customer, stepped in at the last minute to buy shares at $40 to keep the scaled-back offering alive. We have seen similar reticence from corporations in terms of their capital spending, where companies have scaled back plans for this year amid the uncertainty associated with upcoming tariff announcements. ‘Animal spirits’ seem to have been replaced by ‘hibernation.’

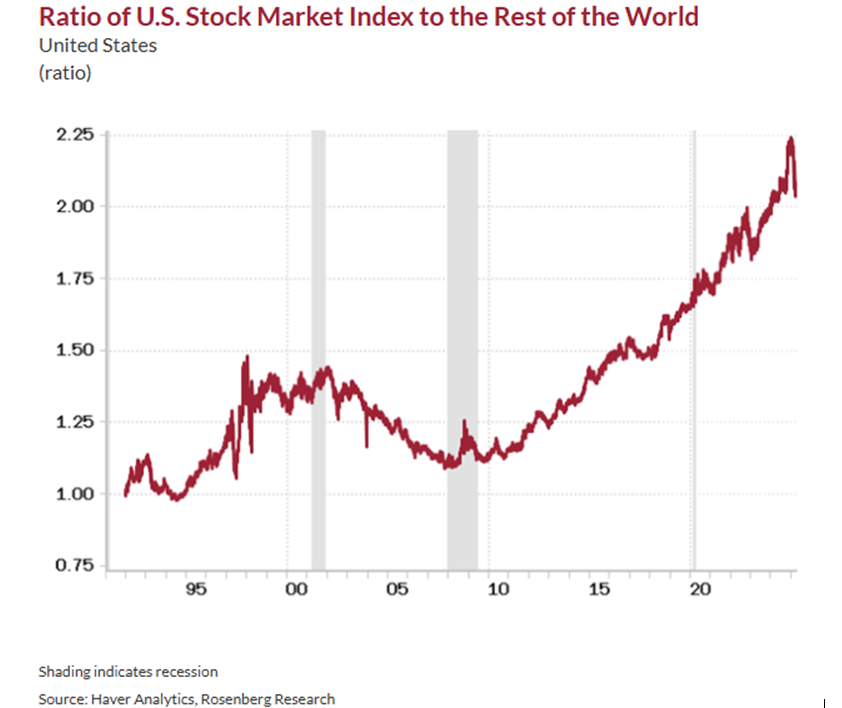

The other term we have heard repeatedly over the past few years has been ‘American exceptionalism,’ which was demonstrated most clearly in the past three years as the U.S. economy and stock market continued to surge while the rest of the global economy succumbed to the 2022 increase in interest rates. The U.S. economy continue to tick along, driven by consumer spending that showed no slowdown. U.S. stocks, powered by the ‘Magnificent Seven’ (Amazon, Apple, Microsoft, Alphabet, Nvidia, Meta and Tesla), outperformed all major global stock markets at the greatest rate since the tech boom of the 1990s while the weight of U.S. stocks in global stock indices rose to a record high of 64%, far in excess of the approximate 20% that U.S. GDP accounts for of global GDP. The chart below shows how strong the move to U.S. stocks has been ever since the Financial Crisis in 2008.

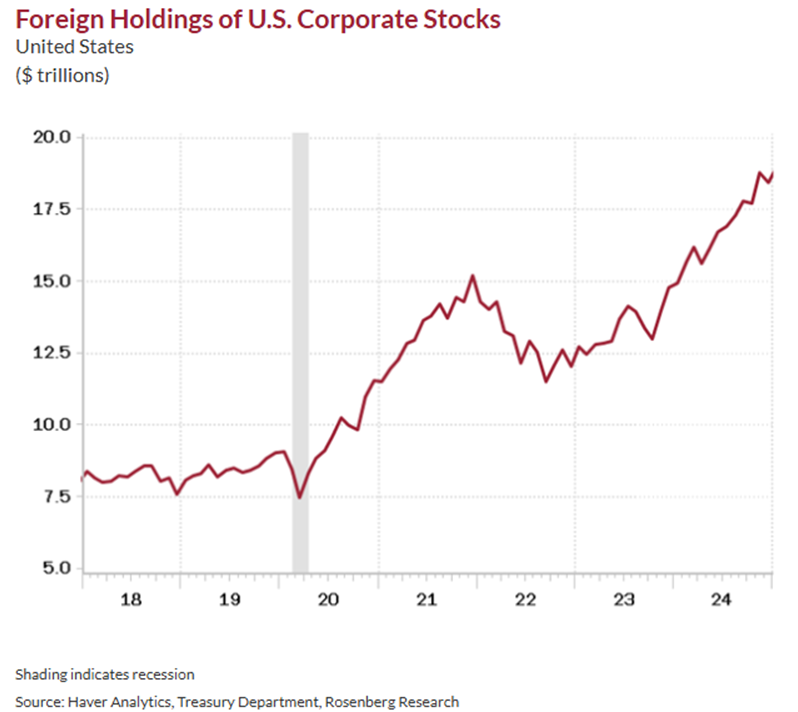

Whether it was due to inflated expectations, unease over policy uncertainty or simply the natural return to normal valuation differences due to excessive ownership of U.S. stocks, the period of outperformance came to an abrupt end in the first quarter as the 5% drop in the S&P500 and over 10% drops in both the tech heavy Nasdaq100 Index and small cap Russell2000‘ compared very poorly to the 7% gain in the Euro Zone STOXX50 Index, which was spearheaded by an 11% jump in Germany’s Dax Index. With major fiscal spending initiatives, particularly in defence spending, taking place in the NATO Bloc countries, the narrative may be shifting to ‘European exceptionalism.’ The stock leadership of the past two years also broke down in the U.S. as the ‘Magnificent Seven’ became the ‘magnificent laggards.’ As of last Friday, those seven stocks as a group were down 15.5% so far in 2025 versus the 5.1% decline for the S&P500 Index, of which they represent over 40%, meaning that the other 60% of the S&P500 is UP 1.8% so far this year. It really does look like a ‘mean reversion’ has been taking place both on global stock markets as well as within the U.S. stock market. The chart below shows how foreign holdings of U.S. stocks have surged in the past five years. This was also paired with a rising U.S. dollar, so foreign investors won on both the stocks and the currency. That over ownership could now continue to be an albatross for U.S. stocks, particularly if the erratic policies of the U.S. administration make investors want to domicile their holdings to their own markets at the same time as they reduce spending in the U.S., add countervailing duties and increase avoidance of U.S. goods and travel to that country.

Canadian stocks, like their European cousins, also bucked the negative trend of the first quarter despite the overhang of additional risks from U.S. tariffs. With one trading day left in the quarter, the TSX Index was up almost 1%, driven largely by sharp gains in the gold sector and some stabilization in the energy sector. Overall, though, the trend was weak, with six of the eleven sub-sectors in negative territory during the quarter. While tariffs are clearly a major risk and headwind for global stocks in general and particularly Canadian industrial stocks, we don’t believe the U.S. president will get what he wants in terms of companies shifting facilities and manufacturing from Canada and elsewhere in the globe back to the U.S. Major capital decisions like moving manufacturing facilities or assembly plants to different geographies take years to both plan and implement and are extremely costly, whereas there could be a completely new administration and policies in the White House in four years. We believe that companies will be reticent to commit to any long-term capital expenditures in that type of uncertain environment. Uncertainty around how and when Congress will enact tax legislation, on top of Trump’s ever-changing tariff announcements, is dragging down expectations for investment, surveys from across the country show. Many firms are putting their investment plans, a key driver of economic growth, on hold. That’s one reason why economists are dialing back growth forecasts for this year. Globalization and the building of the integrated North American supply chain has taken place over the past four decades and will not be unwound in anything beyond token moves to appease the current administration, particularly since globalization was one of the main tenets underlying the substantial expansion of economic growth over that same period. While U.S. manufacturing jobs were lost in the process, that country also picked up massive growth opportunities for their global brands in consumer products, pharmaceuticals, technology and capital goods. It goes way back to simple economic theory; the size of the total production ‘pie’ will see the most growth when each country engages in the activity where they have the biggest competitive advantage. The U.S. advantages have been in innovation, branding and marketing, not in manufacturing.

1 2

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.