Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

John Zechner

June 28, 2018

One area where we do feel more bullish lately is the energy space. The TSX Energy Sector has rallied more than 20% from the March lows but is still almost 40% below the peak seen in 2014 when oil prices were above US$100 per barrel. The widening spread between Canadian Western Select and the benchmark global WTI oil price has been a headwind for Canadian stocks as have the numerous pipeline development problems that have dogged the Canadian distribution system and made daily negative headlines. The result is that we have seen a massive exodus of capital out of the Canadian energy sector by foreign investors and even the Canadian companies have started to shift their spending focus from the Western Canadian Basin to U.S. shale oil plays such as the Permian Basin in Texas. Canadian energy stocks have fallen to exceptionally low values in the process and are looking extremely attractive with oil prices rallying and the Canadian dollar falling. Most importantly though, the global oil market is back in balance. This was evidenced at the June OPEC meetings where the cutbacks announced over a year ago were rolled back to help satisfy the stronger global demand for oil as well as the supply losses at key OPEC producers such as Venezuela, Nigeria and Libya.

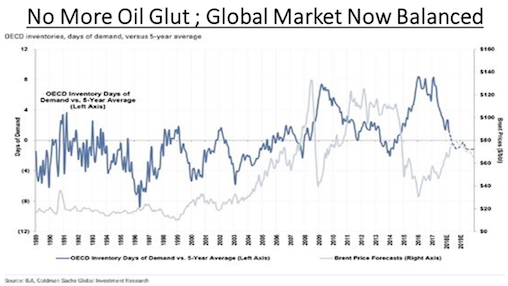

The chart below shows how the combination of reduced supplies and stronger demand have removed the glut of global oil that lead to the collapse in prices back in 2015. Rising U.S. shale oil production had grown the OECD inventories to record levels (dark blue line on chart), which lead to the collapse in oil prices (light blue line) to under US$30 per barrel in early 2016. Since that time we have seen shortfalls in production from some key OPEC producers more than offset the continued gains in U.S. production. This brought global supply/demand into balance. Then the agreement among both OPEC key non-OPEC producers such as Russia to cut back supply by over 1.8 million barrels per day last year helped to eliminate the surplus of oil. With the glut now removed and the market in balance we have seen oil prices continue to move higher in 2018. While we don’t expect to see prices recover to US$100 per barrel, we do expect them to stabilize in this US$65-75 range. On that basis we still see extremely good value in the energy sector in both the U.S. and Canada.

Back in the world of the market-leading FANG stocks, we saw Raymond James raise its target price on Netflix last month. But, given the extremely ‘stretched’ valuation for the stock, we were interested to see just how far ahead the analyst had to look to justify their new target for Netflix. From the report we read:

“We are raising our target price on NFLX from $365 to $465 and reiterate our Outperform rating. Per our survey work and analysis of data sets, we observe continued momentum internationally and increased relevance to U.S. households. Further, media consolidation and the shift to more direct-to-consumer models plays to Netflix’s strengths (e.g. personalization, year-round quality programming, service reliability) and may provide a driver for price increases over time. Our thesis remains unchanged: 1) Netflix is gaining share globally; 2) a deeper content library drives retention and pricing power; 3) there is material margin expansion potential; and 4) the company is positioned for long-term EPS growth and free cash flow generation. Our $465 target price is based on 27x our normalized 2024E EPS of $27.69, which we discount back to 2018. We view this as reasonable for a company sustaining 20% revenue/30% EPS growth over the medium term.”

So we have to look all the way out to 2024 and still put an extremely generous valuation of 27 times earnings on that to justify buying the stock today? Talk about discounting an optimistic future! What are the chances that new disruptive technologies, rising production costs, changing viewership preferences and other industry dynamics will not challenge that outlook? This is the type of analysis that defines market tops. It reminds me of the recommendations we saw for tech stocks in the late 1990s. We all know now how that ended. We prefer buying stocks with somewhat better valuations and more reasonable forecast periods. That may limit the upside but it also gives greater support to the current valuation of the stock. Maybe we’re just losing our nerve!

1 2

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.